Yes — you can use FSA for vaginal estrogen. Prescription vaginal estrogen generally qualifies for reimbursement from a standard health FSA, when the expense is incurred during your coverage period and isn't reimbursed elsewhere. A limited-purpose or dependent-care FSA usually won't cover it. And card acceptance is a separate question from eligibility — you may still need an itemized receipt and a manual claim.

There's a rule printed on the back of most manufacturer savings cards that almost nobody reads — and it names your FSA directly. Mayne Pharma's Imvexxy copay card states that a patient may not seek reimbursement for the value received from the card from any third-party payer, including a flexible spending account or health savings account. Pfizer's menopause savings card requires you to deduct the card's value from any reimbursement request. Get that backwards and you file a claim you weren't entitled to file.

This page is for you if…

- ✓ You have a vaginal estrogen prescription (or are about to get one)

- ✓ You have money in a health FSA

- ✓ Your card was declined and you want to know why

- ✓ You're using a manufacturer copay card and want to know what you can still claim

This page is not for you if…

- → Still deciding whether vaginal estrogen is right — start with our guide to vaginal estrogen

- → Only have a dependent care FSA — that's for childcare, not prescriptions

- → Just want the lowest price with no FSA — see cheapest vaginal estrogen without insurance

The 15-second answer, by account type

| Your account | Does it cover prescription vaginal estrogen? |

|---|---|

| General-purpose health FSA (the common one) | Generally yes — with a prescription, incurred during coverage, not reimbursed elsewhere |

| Limited-purpose FSA (LPFSA) | Usually no — covers dental, vision, preventive care; some plans allow broader expenses after the deductible |

| Dependent care FSA (DCFSA) | No — this reimburses childcare and dependent care services, not prescriptions |

| HSA | Generally yes — same prescribed-medicine rule, different account |

| HRA | Plan-specific — reimbursement only to the extent your employer's plan allows |

Source: IRS Publication 502 and Publication 969. Your plan document controls.

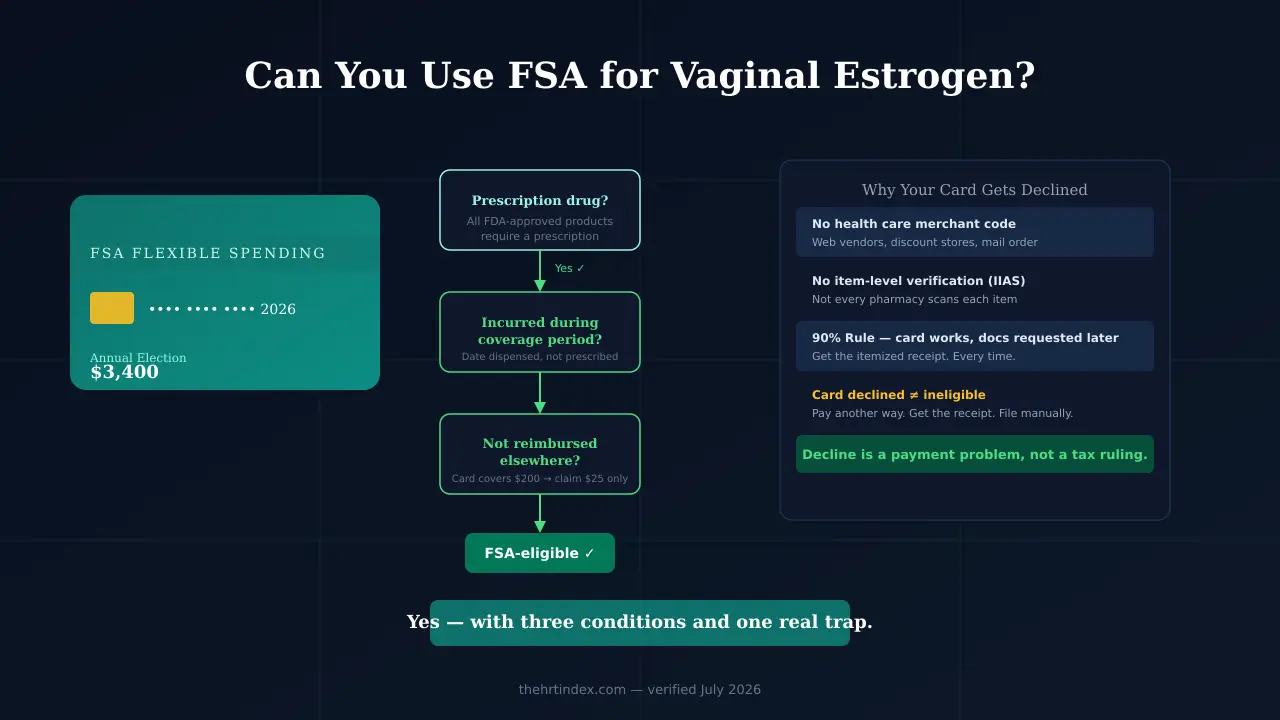

Can you use FSA for vaginal estrogen?

Yes. A standard health FSA can reimburse prescription vaginal estrogen because the IRS treats prescribed medicine as a qualified medical expense under Section 213(d) of the tax code. You don't need a separate Letter of Medical Necessity for it. The two account exceptions are a limited-purpose FSA, which is narrowed to dental, vision and preventive care, and a dependent care FSA, which isn't a medical account at all.

Here's what almost every page on this topic misses. "Can I use my FSA for this" isn't one question. It's three separate decisions, made by three different parties, and answering one doesn't settle the other two:

- 1Is the expense qualified? The IRS decides this, through your plan's rules. Prescribed medicine qualifies.

- 2Will the card authorize? The payment network decides this, at the register, using merchant codes and inventory systems.

- 3Is the transaction substantiated? Your plan administrator decides this — sometimes automatically, sometimes with a letter asking for a receipt weeks later.

The most useful sentence on this page:

A declined FSA card is a payment problem, not an eligibility ruling. If the expense qualifies under your plan, your plan still owes you the reimbursement — you just have to claim it manually instead of at the register.

Why a limited-purpose FSA usually won't work

An LPFSA is what you get when you have an HSA-eligible high-deductible health plan and your employer still wants to offer you an FSA. You generally can't have a full health FSA and contribute to an HSA in the same year — so the LPFSA is narrowed enough that it doesn't disqualify you. Narrowed to: dental, vision, preventive care, and other expenses your plan expressly permits. Vaginal estrogen isn't any of those.

The exception worth checking: some plans include a post-deductible rule that opens the LPFSA to broader medical expenses once you've satisfied your deductible. Look at your summary plan description before you rely on it — not a blog, not us.

The four things to check

It was prescribed.

Every FDA-approved vaginal estrogen product on this page requires a prescription in the U.S.

It was incurred during your active coverage period.

More on this next — it's the condition people miss most.

Your plan includes the expense.

Plans can be narrower than the IRS baseline.

Nobody else already reimbursed it.

Not your insurer, not an HRA, not a manufacturer program. You can only claim what you actually paid.

Which date decides whether it's eligible?

The date the expense was incurred — not the date you paid, and not the date the prescription was written. For a prescription, that generally means the date the medication was dispensed. If your plan year ended before you filled it, the expense usually belongs to the next plan year, even if the doctor wrote it in December.

The December trap

Say your plan year ends December 31. Your clinician writes the prescription on December 28. You fill it on January 3. That's a next-year expense. Your prior-year balance can't touch it — even though the prescription is dated December. Flip it: you filled it December 29 but forgot to submit. That may still be claimable under your plan's run-out window.

Three dates to write down from your plan documents

- →Coverage period end — the last day you can incur an eligible expense

- →Grace period end, if your plan has one — up to 2½ months of extra time to incur expenses

- →Run-out deadline — the last day to submit a claim for an expense you already incurred

They're different dates. They do different jobs. Plans set their own.

Which vaginal estrogen products are FSA-eligible?

All of the FDA-approved ones, when prescribed. Eligibility comes from the prescription, not the brand — so a generic cream and a brand-name ring follow the identical FSA rule. What actually differs between them is which manufacturer savings programs exist, who's locked out of them, and what documentation you'll need.

The Vaginal Estrogen FSA Claim Matrix — verified July 16, 2026

| Product | FDA-approved? | Route | Health FSA | LPFSA | LMN needed? | Keep these docs |

|---|---|---|---|---|---|---|

| Generic estradiol vaginal cream | Yes | Local | Generally eligible | Usually no | No | Itemized receipt or bag tag; EOB if insurance billed |

| Vagifem / Yuvafem / generic estradiol inserts | Yes | Local | Generally eligible | Usually no | No | Same |

| Imvexxy (estradiol softgel insert) | Yes | Local | Generally eligible | Usually no | No | Same — plus see the copay-card rule below |

| Estring (estradiol vaginal system, 7.5 mcg/day) | Yes | Local | Generally eligible | Usually no | No | Same |

| Femring (estradiol acetate vaginal ring) | Yes | Systemic | Generally eligible | Usually no | No | Same |

| Premarin Vaginal Cream (conjugated estrogens) | Yes | Local | Generally eligible | Usually no | No | Same |

| Compounded vaginal estrogen | No | Local | Plan review — see below | Usually no | Plan-specific | Prescription, itemized receipt, pharmacy details |

"Generally eligible" applies the IRS prescribed-medicine rule to an identified prescription product. Not a guarantee your plan will reimburse or any card reader will authorize. Sources: IRS Publication 502 and 969; current FDA-approved product labeling; Pfizer MHT savings program terms; Mayne Pharma Imvexxy copay card terms.

Estring and Femring are both rings. They are not the same decision.

Estring delivers 7.5 mcg of estradiol per day and is indicated for moderate to severe symptoms of vulvar and vaginal atrophy due to menopause. Femring delivers a systemic dose and is indicated for vasomotor symptoms — hot flashes — as well as vulvar and vaginal atrophy. Same FSA rule. Completely different clinical conversation. If a page ever hands you these two as interchangeable because they're both rings, close it.

Non-estrogen prescriptions that follow the same rule

Two prescription products are frequently discussed alongside vaginal estrogen and often mistaken for it. They aren't estrogens, but they follow the same prescribed-medicine FSA logic:

- →Intrarosa (prasterone) — a vaginal insert containing a synthetic form of DHEA, indicated for moderate to severe dyspareunia (painful sex) due to menopause. Generally eligible when prescribed.

- →Osphena (ospemifene) — an oral SERM, not a vaginal product at all. Generally eligible when prescribed.

Both have manufacturer savings programs with the same commercial-insurance-only restrictions described below.

Why did my FSA card get declined at the pharmacy?

Because the card has to clear a second test that has nothing to do with whether the medicine qualifies. FSA card use is limited to merchants with a health care merchant category code, or merchants running an approved item-level verification system. Where neither exists, the transaction is required to be declined — even for a fully eligible prescription.

The four ways a swipe can clear

IRS guidance on FSA debit cards (Revenue Ruling 2003-43) describes how card transactions can be handled:

Copay match

The charge matches a known copay amount under your insurance plan.

Recurring expense match

Same amount, same merchant, already substantiated once.

Real-time verification (IIAS)

The merchant checks each item against an approved list at the register — the SIGIS Eligible Product List.

Conditional authorization

The charge goes through, and the administrator asks for documentation afterward. Card working ≠ claim clearing.

The merchant code problem

Under IRS Notice 2007-2, FSA card use is limited to merchants with health care merchant category codes — codes like 5912 for drug stores and pharmacies. Merchants without one need an approved item-level substantiation arrangement for the card to be used at all. SIGIS names the categories that don't get a health care code: supermarkets, grocery stores, discount stores, wholesale clubs, mail order vendors, and web-based vendors.

That last one matters for anyone buying online. A web-based vendor without a qualifying health care code generally needs an approved substantiation arrangement for FSA-card use. Some online providers process through a medical practice or a pharmacy and clear fine. Others don't. You can't tell from the website. Test it, or ask the provider directly.

The 90% Rule trapdoor

Some pharmacies skip item-level scanning by registering under the 90% Rule: if at least 90% of a store's sales are prescriptions and eligible health products, plan administrators are permitted — not required — to approve the card. But SIGIS states it plainly: transactions at 90% Rule merchants are not auto-substantiated. The card works. Then documentation gets requested later. If you can't produce it, the plan may suspend card use or recover the payment.

What the IRS said in 2023

An April 2023 IRS Chief Counsel memorandum (expressly nonprecedential, but a clear window into agency analysis) reiterated that health FSA reimbursements must be fully substantiated by an independent third party. It rejected self-certification, sampling, favored-provider exceptions, and de minimis thresholds. There is no "it's only $20 so they'll let it slide."

Sources: IRS Revenue Ruling 2003-43; IRS Notice 2007-2; IRS Chief Counsel Advice 202317020 (released April 28, 2023); SIGIS program and cardholder documentation, sig-is.org.

The 6-step declined-card fix

- 1

Ask for an itemized receipt.

Not the card slip. The itemized one, or the bag tag stapled to the bag. It should show patient name, pharmacy, drug, date filled, and amount paid.

- 2

Pay another way.

Any card. The payment instrument doesn't affect eligibility.

- 3

Wait for the EOB if insurance is still processing.

You need your final patient responsibility before you claim anything.

- 4

Submit a manual claim for what you actually paid.

Use your administrator's form. Keep the confirmation number.

- 5

Answer any documentation request before the stated deadline.

Don't let a request expire unanswered.

- 6

If denied, get the reason in writing and appeal that specific issue.

A generic appeal usually fails. The fix depends on the denial code.

Can you use a manufacturer savings card and an FSA together?

Yes, in one direction only. The savings card reduces what you owe at the pharmacy. Your FSA then covers what you actually paid after it. What you cannot do is claim the value the card covered — Mayne Pharma's Imvexxy program prohibits seeking reimbursement for the card's value from an FSA or HSA in writing, and Pfizer's menopause program requires you to deduct the card's value from any reimbursement request.

The damaging admission

Your FSA is the weakest money-saving tool on this page. An FSA does not reduce the pharmacy's price. It changes the tax treatment of the eligible amount you pay. The manufacturer's card reduces the actual price. That's a bigger lever — but it's a lever with conditions, and one of those conditions is a written rule about your FSA.

Who's locked out of the savings cards

Pfizer's MHT savings card (Estring, Premarin Vaginal Cream, Duavee, Premarin tablets, Prempro)

Eligible commercially insured patients may pay as little as $25 per prescription.

- ✗ You must have private insurance — not valid for cash-paying patients

- ✗ Not eligible if enrolled in Medicare, Medicaid, TRICARE, VA, state drug assistance programs

- ✗ Not valid when your private plan already reimburses the entire cost

- ! Per-fill max: $360 Estring, $250 Premarin Vaginal Cream; $1,440 annual cap across the entire portfolio

Mayne Pharma's Imvexxy copay card

- ✗ You must have commercial insurance that covers a valid Imvexxy prescription at the time it's filled

- ✗ Must meet applicable deductible and prior authorization requirements

- ✗ Not valid: TRICARE, Medicare, Medicaid, Medicare Advantage, Part D, Medigap, VHA, DOD, IHS

- ✗ Not valid for cash-paying patients

- ⚠ Not valid for a Medicare-eligible individual enrolled in an employer-sponsored health plan — even if she has commercial insurance and isn't using Medicare. This catches exactly the women most likely to be reading this page.

The caps, and the arithmetic that matters

Estring is replaced every 90 days — four fills a year. At the $360 per-fill maximum, four fills is exactly $1,440 — the entire Pfizer annual cap, precisely exhausted by one year of Estring alone, with nothing left for other drugs in the portfolio. And the cap resets December 31, while your FSA plan year may run on a different calendar entirely. The month you exhaust one rarely lines up with the month the other refills.

The rule that gets claims denied

You may only claim what you actually paid. If the card covered $200 of a $225 copay and you paid $25, your FSA claim is $25. Not $225. Mayne Pharma's Imvexxy card states this in its own terms. Pfizer's terms require you to deduct the card's value from any reimbursement request submitted to your private plan.

Card first → FSA second → claim your real out-of-pocket only.

One thing we noticed: when Pfizer's card is used at a non-participating pharmacy, its rebate process requires you to mail a copy of the original pharmacy receipt — and states that a cash register receipt is not valid. That is the same document standard your FSA administrator uses. Both systems reject the same piece of paper. Get the itemized receipt once and it works for both.

If you're on Medicare, Medicaid, TRICARE, or the VA

The savings cards are closed to you. Federal anti-kickback restrictions and the programs' own written terms exclude prescriptions paid in whole or part by federal or state health care programs. Your FSA works either way — it pays whichever price you land on. But weigh your plan-adjudicated price against a permitted cash-discount price, and ask what an off-insurance fill does to your deductible before you choose.

Swiping an FSA card does not make you a cash-paying patient.

What makes a fill a cash transaction is choosing not to submit the prescription to insurance. The adjudication path determines that — not the plastic you hand over for the balance. You can run a prescription through insurance, apply a copay card, and pay the remaining copay with your FSA card. That's three systems in one transaction, and it's the normal case.

What if you don't have a prescription yet?

You can't spend FSA money on vaginal estrogen without a prescription — every FDA-approved product on this page is prescription-only. A fee for a genuine telehealth medical visit generally qualifies as an FSA expense. A subscription, membership, retainer, or access fee is a much weaker claim — ask for an itemized invoice that separates them.

Midi Health

States you can use your HSA or FSA to pay for Midi copays and services. In-network with most PPO plans. Self-pay: $250 initial / $150 continued care.

Not enrolled with state health care programs. Cannot treat Medicaid/Medi-Cal patients. Medicare beneficiaries accepted as self-pay but cannot submit any related claims.

Check Midi Insurance Coverage →Sesame

States you can pay for its services using HSA, FSA, HRA or other health account funds, and that its support team will provide an itemized bill on request. Does not bill insurance by design — your prescription still goes to your own pharmacy where your insurance and savings card apply normally.

See Sesame Menopause Pricing →Note: If you have a commercial PPO and want the Pfizer or Mayne Pharma savings-card path to stay open, you need an insurance claim. Midi's in-network billing does exactly that. Sesame does not bill insurance by design, which means the manufacturer programs that require a commercial claim won't apply.

Not sure which fits your situation, or not sure you even need vaginal estrogen?

Find My HRT Path →Can you use FSA for lubricants, moisturizers, and dilators?

Not automatically. Related products don't inherit the prescription answer. Eligibility for a moisturizer, lubricant, insert, dilator, or pelvic-floor device depends on the exact product's classification and your plan's documentation rules — and the dividing line isn't hormone vs. non-hormone, or prescription vs. over-the-counter.

The line administrators tend to draw is what the product is sold to do. A product marketed to treat a condition is easier to substantiate than a product marketed to make an activity more comfortable — even when they sit on the same shelf and need no prescription.

| Product | Common FSA treatment |

|---|---|

| Vaginal moisturizers | Commonly listed as eligible by FSA administrators and retailers. Check your specific product against your plan's current list. |

| Personal lubricants | Widely treated as needing a Letter of Medical Necessity — a short note from your clinician tying it to a diagnosed condition. |

| Vaginal dilators | Commonly listed as eligible. Many plans still request an LMN in practice. |

| Hyaluronic acid vaginal inserts (e.g., Revaree Plus) | Varies. FDA's 510(k) database lists Revaree Plus Vaginal Suppositories (K213220) as a Class II personal lubricant — don't assume device clearance alone settles an FSA claim. |

| Supplements | Generally need a prescription or LMN tied to a specific condition. |

| Pelvic floor trainers | Plan-specific. |

None of these are eligible under an LPFSA or DCFSA. Sources: FSA administrator and retailer eligibility listings; SIGIS Eligible Product List criteria; FDA 510(k) database, K213220.

The practical rule: for anything that isn't the prescription itself, check the exact product against your plan before you swipe. Eligibility lists are maintained by administrators and stores — they change.

Can you use FSA for compounded vaginal estrogen?

It generally requires plan review. A compounded drug is mixed to order by a pharmacy for an individual patient. It is not FDA-approved, and FDA does not review compounded drugs for safety, effectiveness, or quality before they're marketed. A plan reimbursing your compounded cream is a plan administrator approving an expense — not FDA approving the drug.

FSA eligibility is a tax and benefits question. FDA approval is a regulatory determination. They are unrelated. A prescribed compounded medication may qualify, subject to your plan's eligible-expense and documentation rules. Three things tend to be harder:

- 1.Product coding and billing vary — compounded prescriptions can be harder to auto-substantiate at the register.

- 2.Your administrator may request more — an itemized pharmacy receipt, prescription details, or an explanation of the formulation.

- 3.Insurance coverage and pharmacy discounts vary. Confirm the pharmacy's billing path and your plan's documentation requirements before you rely on reimbursement.

Be skeptical of blanket eligibility claims. We found compounding pharmacies stating flatly that all of their formulations are FSA/HSA-eligible regardless of ingredients. That's a pharmacy making a claim about a decision it doesn't get to make. Eligibility depends on whether the expense treats a medical condition under IRS rules, as administered by your plan — the pharmacy selling you the cream has no vote.

Compounded is a different decision, not a cheaper version of the same one. Full picture: FDA-approved vs. compounded HRT.

How much FSA money do you have — and when?

Once coverage is active, your full annual election is available during the coverage period — even before all your payroll deductions have happened. That's the uniform coverage rule, and it's the reason an expensive prescription is affordable in month one instead of month nine.

Your 2026 numbers

| Item | 2026 |

|---|---|

| Health FSA contribution limit | $3,400 (up from $3,300) |

| Maximum carryover from 2025 plan year into 2026, if employer adopted carryover | $660 |

| Maximum carryover from 2026 plan year into 2027, if employer adopted carryover | $680 |

| Grace period, if your plan uses one | Up to 2½ months after plan year end |

| Can a plan have both carryover and a grace period? | No — one or the other, or neither |

Source: IRS Revenue Procedure 2025-32 and IRS Publication 969. Your employer may allow a lower carryover, or none.

Watch the carryover numbers carefully.

Many pages state "the 2026 carryover is $680" and let you assume you can carry $680 out of 2026 today. You can't. What could carry into 2026 was $660 — carryover is capped at 20% of the prior year's limit, and 2025's was $3,300. The $680 applies to money moving from 2026 into 2027. Twenty dollars. Small thing. But if a page can't get that right, what else did it get wrong?

If you leave your job

Coverage commonly ends with employment. The plan's coverage-end date, run-out period, and any continuation rights determine which expenses can still be reimbursed. Check those dates before you incur or submit anything new — don't assume the balance travels with you.

The deadline is real, and it isn't marketing.

Most health FSAs are use-it-or-lose-it. If you have a balance and a prescription you've been putting off, the calendar is a genuine constraint. Find your run-out deadline — the last day to submit a claim for an expense you already incurred. It's plan-specific and often later than people assume.

What receipts do you actually need?

For a pharmacy prescription: the itemized receipt or the bag tag — the label stapled to the bag. It should show the patient name, pharmacy, drug, date filled, and amount paid. A credit card slip is not sufficient. If insurance was involved, keep the EOB, which establishes what you actually owed. There's no minimum threshold — every claim needs third-party documentation, no matter how small.

| Document | Useful? | Why |

|---|---|---|

| Itemized pharmacy receipt / bag tag | Yes | Shows patient, drug, date, amount paid |

| Explanation of Benefits (EOB) | Yes, for the copay | Third-party proof of what you owed |

| Itemized telehealth invoice | Yes | Must name patient, provider, date, service, amount |

| Itemized digital receipt | Potentially | Only if it carries every field your administrator requires |

| Credit card slip | No | Shows a dollar amount and a store. Proves nothing about what you bought. |

| Bank statement line | No | Same problem |

| Payment-only screenshot | No | Not a third-party record of the service |

| A website's 'FSA eligible' badge | No | Marketing, not substantiation |

Your administrator may request a different combination of records. Their list wins.

The three charges to keep separate

If you're getting care online, your invoice may bundle things. Ask for itemization:

- ✓The medical visit — generally eligible

- ✓The medication — generally eligible

- ⚠Membership, access, retainer, or convenience fees — much weaker claim. A fee that reserves access to a clinician isn't the same as a medical service.

Filing manually: a cover-note template

"Requesting reimbursement for a prescribed medication expense incurred on [DATE]. The attached itemized pharmacy receipt shows the patient, pharmacy, prescription, date filled, and amount paid. My out-of-pocket responsibility was $[AMOUNT]. No other plan or program has reimbursed the amount I'm claiming."

If insurance was billed, add: "The attached EOB confirms a patient responsibility of $[AMOUNT]." If insurance wasn't involved, leave that line out.

This note doesn't replace your administrator's claim form or required documentation. Save the confirmation number.

What if your claim is denied?

Get the written denial reason first, then appeal that specific issue before the stated deadline. A generic appeal usually fails, because denials come from a handful of very different causes — and the fix for each one is different.

| The reason | What it means | The fix |

|---|---|---|

| Wrong account | You claimed from an LPFSA or DCFSA | Check whether the plan has a post-deductible rule; otherwise it's the wrong account |

| Outside the coverage period | The expense was incurred in a different plan year | Check whether the correct plan year is still within its run-out window |

| Duplicate reimbursement | Insurance or a savings program already covered that amount | Resubmit for your actual out-of-pocket only |

| Missing substantiation | They want a document you didn't send | Send the itemized receipt or EOB — not the card slip |

| Expense not covered by the plan | Your plan is narrower than the IRS baseline | Ask for the specific plan provision in writing |

Your denial checklist: the denial code or reason, the plan provision cited, the exact document they want, the appeal deadline, and your submission confirmation. Get all five before you write a word of appeal.

Will your employer see what you bought?

Your manager ordinarily does not receive itemized FSA claim details. Claims are handled by a third-party administrator or by designated plan-administration staff, and your plan's privacy notice explains who may access protected health information. Many prescription swipes also clear automatically through copay or item-level matching, so no separate claim document is generated at all.

A health FSA may be a HIPAA-covered group health plan. The Privacy Rule governs how a health plan shares protected health information with an employer. In practice, claims typically route to a third-party benefits administrator processing thousands a day — not to your manager, not to your team. Your plan's privacy notice is the document that tells you who can access what. Read it if this matters to you.

FSA vs. HSA vs. insurance — what does what?

When you use insurance, the plan and the pharmacy claim determine the adjudicated price and your patient responsibility. An FSA or HSA then pays or reimburses an eligible portion of that responsibility. They're not alternatives — they're sequential, and neither can reimburse a dollar the other already covered.

| Feature | Health FSA | HSA |

|---|---|---|

| Ownership | Employer-established arrangement; not portable | Yours — portable, permanent |

| 2026 limit | $3,400 | $4,400 self-only / $8,750 family (+$1,000 if 55+) |

| Full amount available upfront? | Yes — the whole election, during coverage | No — only what you've deposited |

| Use it or lose it? | Generally yes; employer may adopt carryover up to the maximum, a grace period, or neither | No — it rolls forever |

| Requires a specific health plan? | No | Yes — a qualifying HDHP to contribute |

| Covers prescription vaginal estrogen? | Generally yes | Generally yes |

| Does a card decline mean ineligible? | No | No |

Sources: IRS Revenue Procedure 2025-32 (FSA); IRS Revenue Procedure 2025-19 (HSA/HDHP); IRS Publication 969.

One thing people get wrong about HSAs: contribute through payroll and you skip FICA payroll tax, same as an FSA. Deposit directly from your bank account and you don't — you get the income tax deduction, but not the payroll tax break. Over years, that adds up.

Working the HSA side? Our separate guide covers using an HSA for HRT, including the same vaginal estrogen analysis for HSA accounts.

What we actually verified

What we verified

- → IRS Publication 502, 969, and Section 213(d) on prescribed medicine as a qualified medical expense

- → Account-type distinctions — general-purpose, limited-purpose, dependent care, HSA, HRA

- → 2026 limits — Revenue Procedure 2025-32 ($3,400; $660 into 2026; $680 into 2027) and Revenue Procedure 2025-19

- → Card and substantiation mechanics — Revenue Ruling 2003-43; Notice 2007-2; Chief Counsel Advice 202317020

- → Pfizer MHT savings card terms and Mayne Pharma Imvexxy copay card terms, read on manufacturer pages

- → Product regulatory status and route — current FDA-approved labeling; Estring as local low-dose, Femring as systemic

- → Compounded drug status — FDA's compounding Q&A

- → Revaree Plus — FDA 510(k) database record K213220

- → Provider payment statements — read directly on joinmidi.com and sesamecare.com on July 16, 2026

What we did NOT test

- ✗ We did not run a live claim through any FSA administrator

- ✗ We did not swipe a card at any pharmacy or provider checkout

- ✗ We have not read your plan document — and it beats every general rule here

- ✗ We do not publish live pharmacy prices — they move by ZIP, pharmacy, quantity and day

- ✗ We cannot promise reimbursement — nobody honest can; your administrator decides

Found something wrong? Tell us — we publish corrections with dates.

Last verified: July 16, 2026. This follows The HRT Index Verification Standard: read every published price, separate FDA-approved from compounded, verify state availability and insurance, and re-check on a fixed schedule. We evaluate providers on five things, in this order: clinical legitimacy, care quality, medication fit, price transparency, access.

Frequently asked questions

Is estradiol vaginal cream FSA-eligible?

Generally yes, with a prescription, from a standard health FSA — when it's incurred during your coverage period and isn't reimbursed elsewhere. Because it's generic, there's typically no manufacturer savings card, so a pharmacy discount program and your FSA are the usual combination.

Can I use my FSA for Vagifem, Yuvafem, or Imvexxy?

Generally yes, all three, with a prescription. Note that Imvexxy's copay card carries a written prohibition on seeking reimbursement for the card's value from an FSA or HSA — you can still use your FSA for what you actually pay after the card.

Is Estring FSA-eligible?

Generally yes. If you have commercial insurance, Pfizer's savings card may reduce your cost to as little as $25 per fill, with savings capped at $360 per fill and $1,440 per calendar year across Pfizer's menopause portfolio. Your FSA then covers what you actually pay.

Is Femring FSA-eligible?

Generally yes. But don't treat Femring and Estring as the same product because both are rings. Estring is a low-dose local vaginal system. Femring is systemic and is also indicated for hot flashes. Different clinical decision entirely.

Is compounded vaginal estrogen FSA-eligible?

It generally requires plan review. Compounded drugs are not FDA-approved, and FDA doesn't review them for safety, effectiveness, or quality before marketing. Your plan may still reimburse it — that's a benefits decision, not an FDA one. Expect more documentation and no manufacturer savings card.

Does FSA eligibility mean a drug is FDA-approved?

No — they're unrelated. FSA eligibility is a tax and benefits question decided by the IRS and your plan. FDA approval is a regulatory determination based on the agency's review of safety, effectiveness, labeling and manufacturing quality. A plan reimbursing a compounded cream tells you nothing about FDA's view of it.

There's a boxed warning on my box. Does that affect my FSA?

No. Labeling status has no bearing on FSA eligibility. FDA labeling changes are approved product by product, so a warning on a current label reflects that product's current approved labeling. Talk to your prescriber about what your product's label means for you — but it doesn't touch the reimbursement question.

Do I need a Letter of Medical Necessity for vaginal estrogen?

A separate LMN normally isn't required for a prescription drug. But the prescription alone isn't your full claim record — keep the itemized pharmacy receipt or bag tag, and the EOB if insurance was billed. LMNs are typically required for dual-purpose items like lubricants.

Why was my FSA card declined for an eligible prescription?

Usually a merchant or substantiation problem, not an eligibility ruling. FSA card use is limited to merchants with health care merchant codes or an approved item-level verification system. Pay another way, get the itemized receipt, and file manually.

Can I pay with a regular credit card and reimburse myself?

Yes. The payment instrument doesn't determine eligibility. Pay however you like, keep the itemized receipt, file the claim.

Can I use insurance and my FSA together?

Yes, and usually you should. Insurance adjudicates first, then your FSA covers your patient share. Just never claim more than you actually paid — if a copay card covered part of it, claim only your portion.

Can my FSA pay for my spouse's prescription?

Generally yes. A health FSA can reimburse qualified expenses for you, your spouse, and qualifying dependents, provided they meet the applicable rules. Your plan administers the claim.

Does an FSA cover the telehealth visit, not just the medicine?

A fee for a genuine telehealth medical service generally qualifies. A membership, retainer or access fee is a much weaker claim. Ask for an itemized invoice separating them.

Can I use an FSA for lubricant?

Administrators commonly treat lubricants as needing a Letter of Medical Necessity, because they're dual-purpose. Vaginal moisturizers marketed to treat dryness are more often listed as eligible without one. Check your exact product against your plan's current list.

Which date matters — when it was prescribed or when I filled it?

When the expense was incurred, which for a prescription generally means when it was dispensed. A December prescription filled in January is usually a January expense — even if the prescription was written in December.

What if my plan year already ended?

Check your run-out deadline — the last day to submit claims for expenses you already incurred. It's plan-specific and often later than people expect.

Can I use a limited-purpose FSA?

Usually not before any post-deductible phase. LPFSAs cover dental, vision, preventive care, and whatever else your plan expressly permits — which is what keeps you HSA-eligible. Check your summary plan description for a post-deductible rule that opens broader medical expenses.

Still deciding what kind of care you need?

If you have the prescription and a standard health FSA, you have what you need. If you're still working out whether you need local vaginal estrogen or systemic HRT, whether online care is the right starting point, or which provider works with your insurance and your state — that's a different question, and it deserves a real answer.

Take Our Free Matching Quiz — Find My HRT Path →A few questions. A personalized action plan. Including a flag if your situation should start with an in-person clinician instead.

Sources

Tax and benefits

- IRS — Publication 502, Medical and Dental Expenses

- IRS — Publication 969, Health Savings Accounts and Other Tax-Favored Health Plans

- IRS — Revenue Procedure 2025-32 (2026 health FSA limit and carryover)

- IRS — Revenue Procedure 2025-19 (2026 HSA and HDHP limits)

- IRS — Revenue Ruling 2003-43 (FSA debit cards and substantiation)

- IRS — Notice 2007-2 (merchant category codes and the 90% Rule)

- IRS — Chief Counsel Advice 202317020, released April 28, 2023 (nonprecedential)

- SIGIS — program documentation, cardholder and merchant FAQs, Eligible Product List criteria, sig-is.org

- U.S. Department of Health and Human Services — HIPAA and employer access to health information

Medical and regulatory

- FDA — "Compounding and the FDA: Questions and Answers"

- FDA — current approved labeling for products named on this page

- FDA — 510(k) database, K213220 (Revaree Plus Vaginal Suppositories)

- HHS Office of Inspector General — Special Advisory Bulletin on copayment coupons

Manufacturer programs (retrieved July 16, 2026)

- Pfizer — Menopause Hormone Therapies savings card, full terms and conditions

- Mayne Pharma — Imvexxy copay card, program terms, conditions and eligibility criteria

Providers (retrieved July 16, 2026)

- Midi Health — Pricing & Insurance, joinmidi.com

- Sesame — HSA/FSA/HRA payment information, sesamecare.com