Progesterone prior authorization for menopause is rarely about you. It’s about which product got written, and which plan you happen to have.

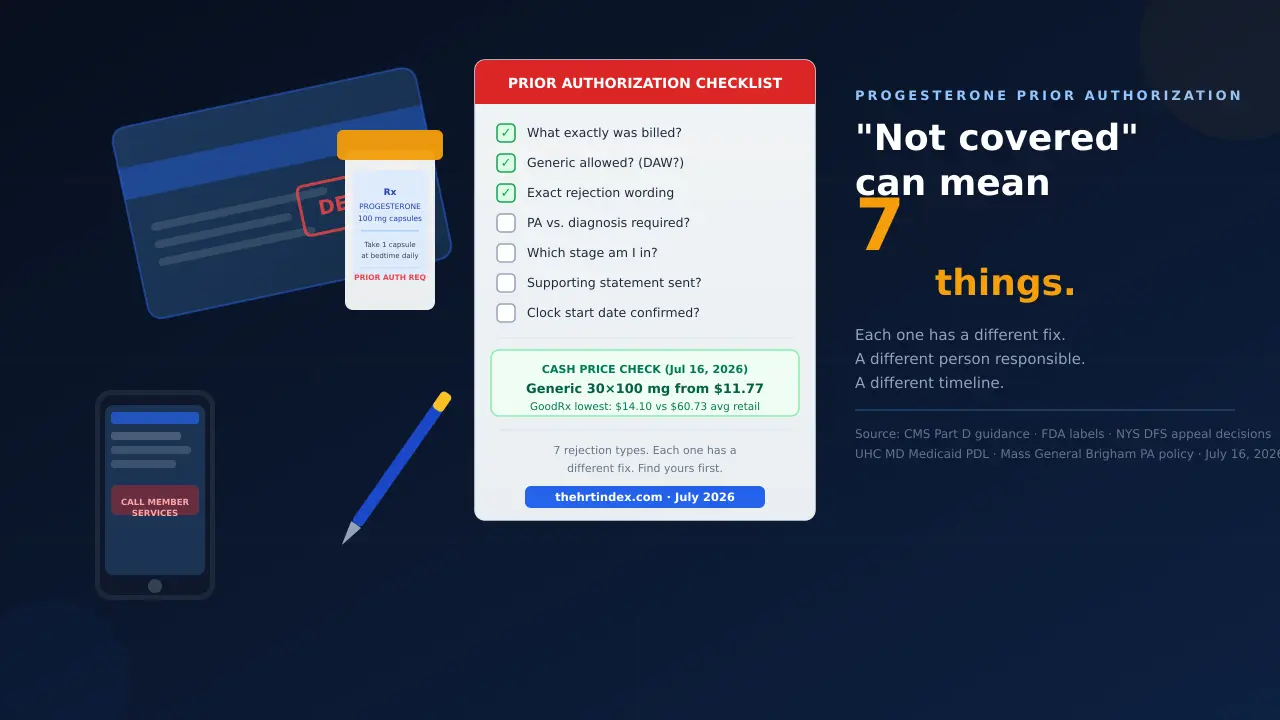

Here’s the bottom line.“Not covered” can mean seven different things. Each one has a different fix, a different person responsible, and a wildly different timeline. Some take a phone call. Some take an appeal. Telling them apart takes about sixty seconds at the pharmacy counter — and almost nobody does it, which is why women lose weeks to the wrong process.

If your plan rejected brand Prometriumand your prescription allows substitution, FDA-approved generic progesterone is often the shortest route. On July 16, 2026, Drugs.com listed 30 × 100 mg generic capsules from $11.77, and GoodRx displayed a lowest price of $14.10 against an average retail price of $60.73.

Two questions before you do anything:

What exactly did you bill? and Does my prescription allow a generic?The second one matters more than you’d think — if your prescriber marked it “dispense as written,” the pharmacy legally cannot swap it, no matter what it costs.

The answer changes if: the plan rejected the generic(that’s a different rule entirely); you have a peanut allergy(Prometrium contains peanut oil — this is a safety issue before it’s an insurance one); you’re on Medicare Part D (its own clock, its own appeal ladder); or you were prescribed Bijuva (a combination capsule with product-specific criteria).

And one more thing. New York publishes its insurance appeal decisions — the full reasoning, not just the outcome. We read the menopause ones. There’s a pattern in them that will change how you talk to your doctor’s office this week.

Is this page for you?

Yes, if:

- Your pharmacy said “prior authorization required,” “not on formulary,” “step therapy,” “diagnosis required,” or “refill too soon.”

- You put the bag down because of the price.

- A refill that worked for months suddenly stopped working.

- Your doctor’s office says they’re “waiting on insurance.”

No, if:

- You’re deciding whether to start HRT → HRT basics guide.

- Your question is about compoundedprogesterone specifically → Is Compounded HRT Safe?

- You have signs of a severe allergic reaction or another emergency symptom — call 911 or go to emergency care. For unexpected bleeding or a non-emergency medication concern, contact your clinician promptly. Insurance paperwork waits. This doesn’t.

The 7 rejection types, decoded

Everything else on this page depends on this table. “Not covered” is not a diagnosis of your problem. These seven things are.

| What the pharmacy said | What it can mean | Who acts | Your first move | Likely cost |

|---|---|---|---|---|

| “Prior authorization required” — brand Prometrium | Generic preference, brand exclusion, non-preferred tier, or a product-specific rule | You + prescriber | Ask whether your prescription allows a generic | Generic copay, or ~$12–14 cash |

| “Prior authorization required” — generic progesterone | A PA, quantity limit, diagnosis edit, or duplicate-therapy rule | Prescriber | Get the exact rejection wording | Your plan’s generic copay if approved |

| “Diagnosis required” | The claim system didn’t find a matching diagnosis on file | Pharmacy or prescriber | Ask whether the pharmacy can transmit the diagnosis | Your plan’s copay if it clears |

| “Not on formulary” | Not listed as covered on the current drug list | Prescriber | Ask whether the plan allows an exception, or treats it as excluded | Copay if approved |

| “Step therapy required” | The plan wants a preferred drug tried first | Prescriber | Ask exactly which drug, what dose, how long | Copay if approved |

| “Refill too soon” | Claim history doesn’t match a dose or schedule change | Pharmacy | Ask them to confirm the new prescription and day supply | Your plan’s copay |

| “Not covered — compounded” | Compounded products may be excluded from the benefit | You + prescriber | Ask whether it’s an exclusion or a formulary decision | Cash, or switch to an FDA-approved product |

Find your row. Read the section that matches it. You don’t need the whole page.

The right online HRT provider isn’t the same for every woman — it depends on your symptoms, your age, your medication route preference, your risk history, and your insurance situation. Use The HRT Index’s Find My HRT Path tool to match your situation to the right provider — and to flag when online care isn’t the right starting point — before your first consult.

How does progesterone prior authorization for menopause work?

Prior authorization means a health plan requires approval before it will cover a prescription under its product-specific and plan-specific rules. A member, pharmacy, prescriber, or authorized representative may be able to start the process, but when the plan asks for clinical support, that generally has to come from the prescriber. It is a payment rule, not a review of whether your diagnosis is real.

Here’s the part that trips everyone up: plans set these rules per plan, not per company.

A single insurer might administer a commercial PPO, a Medicaid managed care plan, a Medicare Part D plan, and dozens of employer-specific plans. Each has its own drug list, its own effective date, and its own restrictions on the same medication. So when a website tells you “Cigna requires prior authorization for progesterone,” ask: which Cigna plan? On what date? For which product and strength?

We’ll be straight with you, and it’s the most useful thing on this page: no honest source can tell you your plan’s rule from your insurance company’s name. Not us, not anyone. What we can do is show you how to find it, and what each answer means.

Prior authorization isn’t the only rule — and it’s not always the one you have

Look at a real drug list. The UnitedHealthcare Community Plan of Maryland Preferred Drug List, effective July 1, 2026 — a Medicaid managed careformulary, not a commercial one — sorts drugs into Tier 1 (generic) and Tier 2 (brand), then applies seven separate restriction markers on top:

| Marker | What it means |

|---|---|

| PA | Prior authorization required |

| DX2RX | Diagnosis required |

| QL | Quantity limit |

| ST | Step therapy |

| AL | Age limit |

| GE | Gender limit |

| SP | Specialty medication |

Source: UnitedHealthcare Community Plan of Maryland PDL, effective 07/01/2026. Checked July 16, 2026. This is one Medicaid plan — do not assume a commercial plan under the same brand uses the same rules.

On that specific list, generic oral progesterone sits at Tier 1 with DX2RX and QL. Not PA. A woman on that plan who is told “it needs a prior auth” is being pointed at the wrong process entirely.

So don’t accept the phrase “it needs a prior auth” as your answer. Ask the pharmacy to read the rejection and tell you whether the claim shows PA, diagnosis required, quantity limit, refill timing, non-formulary status, or something else. It’s on their screen. It takes seconds, and it decides everything that happens next.

How to find your actual drug list

You need four things, and they’re all findable in about ten minutes:

- Your exact plan name.It’s on your card — and it’s usually longer and more specific than “Aetna” or “Blue Cross.”

- Your pharmacy benefit manager (PBM).Sometimes it’s a different company from the one on the front of your card. Check the back.

- The formulary or “preferred drug list” for your plan, at your current plan year. Log into your member portal, or search your exact plan name plus “formulary.”

- The effective date on that document. A drug list from last plan year can be flatly wrong today.

Then find progesterone and read the markers next to it.

One wrinkle worth knowing: self-funded employer plans

If you get insurance through a large employer, there’s a decent chance your plan is self-funded— meaning your employer pays the claims and the insurance company on your card is only administering them.

Why it matters: your appeal rights, external review options, and the rules that govern them can be different from a plan the insurer actually funds. If your denial letter mentions ERISA, or your HR benefits team is the one answering coverage questions, ask directly: “Is this plan self-funded, and what external review rights do I have?”

Which product is actually on your prescription?

Generic oral progesterone, brand Prometrium, Bijuva, and compounded progesterone are four different things to an insurance plan. They can sit on different tiers, carry different restrictions, and require different paperwork. Before anyone submits anything, confirm exactly which product the pharmacy billed.

This is the single most useful question you can ask your pharmacist. Not “is it covered?” — “what exactly did you bill?”

| The label says | What it is | Don’t assume |

|---|---|---|

| progesterone 100 mg or 200 mg capsule | Generic micronized progesterone— micronized means the drug is ground into very fine particles so your body absorbs it better | That it follows the same rule as brand Prometrium |

| PROMETRIUM | Brand-name micronized progesterone | That brand is covered just because generic is |

| BIJUVA | An FDA-approved capsule combining estradiol and progesterone in one pill | That it’s treated as two separate prescriptions |

| compounded progesterone | A product prepared by a compounding pharmacy or outsourcing facility. Not FDA-approved. | That it’s covered, or interchangeable with FDA-approved progesterone |

| vaginal progesterone | A different route entirely | That oral coverage rules apply |

Can the pharmacy even substitute a generic? Check this first

Before you plan around “just switch to the generic,” find out whether that’s legally available to you.

Ask the pharmacy: “Does my prescription allow generic substitution, or is it marked dispense as written?”

If your prescriber wrote DAW(“dispense as written”) or brand medically necessary, the pharmacy cannot substitute — full stop, regardless of price. You’d need your prescriber to authorize a change or issue a new prescription.

Brand Prometrium

The current U.S. label indicates Prometrium for prevention of endometrial hyperplasia in nonhysterectomized postmenopausal women who are receiving conjugated estrogens tablets, and for secondary amenorrhea.

Note how specific that is. Plenty of women take micronized progesterone alongside a different estrogen product than conjugated estrogens tablets — that’s a clinical decision between them and their prescriber, and it’s common. But it isn’t what the label says, and that distinction sometimes shows up in coverage criteria.

The UnitedHealthcare Community Plan PDL states that it requires mandatory generic substitution on the vast majority of products when a generic equivalent is available, and that brand-name drugs may be covered in certain situations by requesting a prior authorization. That ’s not us characterizing plan behavior. That’s a plan describing itself.

Bijuva — its own criteria

Bijuva is the FDA-approved combination of estradiol and progesterone in a single capsule, for moderate to severe hot flashes and night sweats in a woman with a uterus.

Plans don’t treat one-capsule convenience as a covered reason. Here’s a real example — and it’s one plan’s policy, not a universal rule.

Mass General Brigham Health Plan’s commercial/exchange Bijuva policy, effective September 1, 2025 (rechecked July 16, 2026), is marked as a prior authorization policy. It grants authorization only when all of these are true:

- Member is 18 years of age or older

- Member has a diagnosis of moderate to severe vasomotor symptoms due to menopause

- Member has had an inadequate response, intolerance, or a contraindication to an estrogen and progesterone formulation taken concurrently as separate agents

Approvals run 12 months. Read criterion 3 again. Under thispolicy, the plan wants documentation that estrogen and progesterone taken separately didn’t work for you. Your plan may word it differently. Get your plan’s actual criteria before anyone writes anything.

Compounded progesterone

Compounded drugs are prepared by a compounding pharmacy or outsourcing facility. They are not FDA-approved, and the FDA does not review them for safety, effectiveness, or manufacturing quality before they’re marketed.

What we’ll tell you is the coverage mechanics: some plans exclude compounded products from the pharmacy benefit, and others cover them only under narrow rules. So the question to ask is precise: “Is this a benefit exclusion, a non-formulary decision, or a documentation problem?” Those three answers lead to three different places, and only one of them is a paperwork fix.

→ Is Compounded HRT Safe? What Actually Differs

What changed in February 2026

On February 12, 2026, the FDA approved labeling changes for six menopausal hormone therapy products — including Prometrium. The changes removed specified boxed-warning statements about cardiovascular disease, breast cancer, and probable dementia.

It did not remove every warning.The current labels still carry contraindications and other warning material. Specific boxed-warning statements came out. That’s what happened, and it’s not the same as “the risks are gone.”

And it hasn’t moved insurance.None of the payer policies we reviewed for this page stated that its criteria changed because of the February 2026 labeling action. If someone tells you the new label is leverage on your prior authorization, they’re guessing.

What did the pharmacy actually reject?

A pharmacy rejection is a claim code, not a verdict on your treatment. Prior authorization, diagnosis required, quantity limit, refill-too-soon, non-formulary status, and benefit exclusion are different problems with different owners and different fixes. Getting the exact rejection is the step that makes every later step work.

Call the pharmacy. Ask this, word for word:

That’s it. The pharmacist can see it. It takes seconds, and it’s the difference between fixing the right problem and waiting on the wrong one.

“Diagnosis required” is not prior authorization

Most pages miss this entirely, and it’s common enough to matter.

The UnitedHealthcare Community Plan of Maryland PDL spells out the mechanism. The plan requires that the diagnosis for prescriptions in certain classes match the FDA-approved use, or a use supported by current published evidence. The diagnosis is verified at the point of sale by the pharmacy claims system. If a matching diagnosis isn’t found in the medical claim file or on the pharmacy claim, the prescription rejects right there at the counter.

But read the next line in that same document, because it matters: if the diagnosis provided still doesn’t match the approved use, a prior authorization may then be requested.

So there are two versions of this. Sometimes it’s a missing data field and the pharmacy can transmit it. Sometimes the diagnosis genuinely doesn’t meet the plan’s rule, and you’re headed for a real review. Ask which one you have before anyone starts new paperwork.

“Quantity limit”

The billed amount or day supply exceeds the plan’s rule. Common trigger: your dose changed and the claim didn’t. Check strength, capsule count, day supply, and whether something recently changed. The pharmacy can verify the billed quantity and day supply — but a plan override or prescriber action may still be needed.

“Refill too soon”

Your claim history doesn’t reflect something that changed — a new schedule, a dose change, a lost bottle, travel. Start with the pharmacy: ask them to confirm they processed the new prescription, quantity, and day supply. A corrected claim often resolves it. Sometimes you’ll still need a plan override or a prescriber note.

“Not on formulary”

The product isn’t listed as covered on your plan’s current drug list. This usually needs an exception, and your prescriber has to support it.

“Step therapy”

The plan wants you to try a preferred drug first. This is a payment rule, not a treatment instruction. Nobody at an insurance company is telling you to change your medication — and you shouldn’t change it based on a claim rejection. Ask exactly which alternative, at what dose, for how long, and what counts as having completed the step. Then take that to your prescriber.

“Excluded”

A real benefit exclusion. Ask a precise question: “Is this product excluded from my benefit, simply absent from the formulary, or excluded because it doesn’t meet the definition of a covered drug?” Those categories can carry different review rights.

Where are you in the process? (This saves people weeks)

A lot of women try to appeal before there’s anything to appeal. There are four stages, and they’re not interchangeable:

The claim was billed wrong or is missing data. Pharmacy territory. No appeal exists yet.

The plan needs clinical support before it decides. Prescriber territory. Still no appeal.

You're asking the plan to cover something it doesn't normally cover, or to waive a requirement. Prescriber support required.

A decision has been made and you're contesting it. This only exists after an actual denial.

If you don’t have a written denial, you’re probably not at stage 4. Ask the plan: “What stage is my request in, and has a determination been made?”

Don’t decide on your own to stop, double, split, or substitute your medication. Call your prescriber and tell them the fill was blocked — today, not next week. If you’re having signs of a severe allergic reaction or another emergency symptom, don’t wait on any of this. Get emergency care.

What does generic progesterone cost, and when does paying cash make sense?

FDA-approved generic micronized progesterone is widely available at low cash prices. On July 16, 2026, Drugs.com listed 30 × 100 mg capsules from $11.77, and GoodRx displayed a lowest price of $14.10 against an average retail price of $60.73. Actual price depends on strength, quantity, pharmacy, ZIP code, stock, and savings program.

Price snapshot — checked July 16, 2026

| Product | Displayed price | Source |

|---|---|---|

| Generic progesterone, 30 × 100 mg | from $11.77 | Drugs.com price guide |

| Generic progesterone, 30 × 200 mg | $17.54–$24.50 | Drugs.com price guide |

| Generic progesterone, most common version | $14.10 lowest, vs $60.73 average retail | GoodRx |

These are savings-program and price-guide figures, not guaranteed local prices. Check your specific strength, quantity, and pharmacy before you count on any of them.

For a lot of women reading this, the cash price of the generic is lower than the copay they were preparing to fight for. That’s not a consolation prize. Check it before you assume otherwise.

“But isn’t the generic worse?”

FDA-approved generic drugs must contain the same active ingredient, at the same strength, in the same dosage form, by the same route as the reference product, and must meet FDA’s bioequivalence requirements. They’re expected to produce the same clinical effect and safety profile under the labeled conditions of use.

One real caveat we won’t paper over:inactive ingredients can differ by manufacturer. For most people that’s irrelevant. If you have an allergy or an ingredient sensitivity, it isn’t — and that’s covered in its own section below.

And a line we won’t blur: everything above applies to FDA-approved generic micronized progesterone. It does not apply to compounded progesterone, which is not FDA-approved and is not a generic of anything.

When paying cash is the wrong move

- You’re close to your deductible or out-of-pocket maximum. A discount-card transaction generally bypasses the insurance claim, so it may not be credited toward either. Ask your plan whether it accepts a member-submitted claim before you assume.

- Your plan’s copay is actually lower. Check. Sometimes it is.

- You may need this documented later. If a future exception could depend on showing you tried something, ask the plan what evidence it accepts and whether a cash fill shows up in the records its reviewer looks at.

- Your prescription is marked dispense as written. Then this route isn’t open until your prescriber changes it.

Not sure if cash or coverage is right for you?

If you’re not sure whether cash or coverage is the better path — or whether the care you’re getting can actually handle this — our Find My HRT Path tool gives you a personalized action plan in about 90 seconds, before you spend anything.

Find My HRT Path →What real appeal decisions show about documentation

New York State publishes its external appeal decisions, including the reviewers’ full clinical reasoning. Across six selected menopause-related decisions, outcomes turned on case-specific factors: the plan’s listed alternatives, chart documentation, the diagnosis and indication, therapeutic equivalence, and prior reactions. These are individual cases and do not establish approval odds or a universal rule.

When you exhaust a plan’s required internal process, some denials are eligible for external review— an independent medical reviewer, outside the insurance company. In New York’s eligible external appeal process, the reviewer’s decision binds the plan. That’s New York’s program — it doesn’t create a national standard.

But New York publishes the decisions. With the reasoning. And you can read them.

Two things before you read them. First, this is a selected set, not a survey. Second, we’re deliberately not turning six cases into a percentage. Six cases is not an approval rate, and anyone who gives you one is inventing it.

| Case # | Year | Therapy | Drug | Outcome | The reviewer’s reasoning |

|---|---|---|---|---|---|

| 202302-158900 | 2023 | Systemic MHT | Prometrium (brand) | Upheld | She was on Divigel and started generic Prometrium for endometrial protection. The generic gave her hot flashes she couldn’t tolerate. She asked for the brand. The reviewer concluded the generic is FDA-approved with the same indication and warnings, and that brand Prometrium “is not medically necessary as she could use the generic form.” |

| 202207-151963 | 2022 | Systemic MHT | Prempro | Upheld | She’d tried and failed multiple options and was doing well on Prempro. Denied because Premarin plus medroxyprogesterone are the same two medications as Prempro and are on the formulary — and she hadn’t failed that combination. |

| 202009-131454 | 2020 | Systemic MHT | Vivelle-Dot | Upheld | ⚠️ Read this one twice. She had tried a generic patch. She hadside effects. The reviewer’s words: side effects “per the letter; however, the office notes do not document this.” Also no documentation she’d tried estradiol tablet, Menest, Premarin, or Yuvafem. And the claim that the Dot has fewer side effects was “not supported by the medical literature.” |

| 202103-136077 | 2021 | GSM (local) | Intrarosa | Upheld | The plan required failure or serious side effects with allformulary alternatives in the class. She’d failed Estring, estradiol cream, and Premarin cream — but not Vagifem. The reviewer found she hadn’t met the formulary requirement. |

| 202104-137028 | 2021 | GSM (local) | Osphena | Upheld | Multiple factors. She’d tried Vagifem but was “worried about the continuous effect of estrogen” — which the reviewer treated as neither a failure nor a contraindication. The decision also noted the submitted records described introital stenosis, a different condition from vaginal atrophy. |

| 202108-140606 | 2021 | GSM (local) | Estring | Overturned | She’d failed estradiol cream and brand Estrace cream (adverse reaction) and Femring (ineffective) — three named alternatives, three named outcomes — and had used Estring successfully for years with documented efficacy and no adverse effects. Denial reversed. |

Source: New York State Department of Financial Services public external appeal database, read July 2026. NYS DFS notes that its database may not be complete, accurate, or up to date, that every case involves many individual variables, and that nothing in it promises a particular outcome in any other case. GSM = genitourinary syndrome of menopause.

What keeps showing up

Six decisions. Different drugs, different plans, different years. The same factors keep appearing.

Recurring in the decisions that went against the patient:

- “The brand works better than the generic.” These reviewers treat FDA-approved generics as therapeutically equivalent and say so directly.

- A failure that lives in the appeal letter but not the chart. The Vivelle-Dot decision turned on exactly this.

- Most of the alternatives, not all.Where a plan’s criteria required failure of every formulary option in the class, three of four wasn’t enough.

- “I’m worried about” or “I’d prefer.” Reviewers separated concern from documented failure and contraindication.

- A mismatch between the diagnosis in the record and the treatment requested.

In the one that was overturned:named alternatives, named failures, named reactions — all documented — plus a record of sustained success on the requested product.

You’re not writing to someone who will be moved by how you feel. You’re writing to a reviewer reading a record against a set of criteria.

If your bad reaction to a medication isn’t in your chart, a reviewer has no way to know it happened. That’s case 202009-131454, in the reviewer’s own words.

What your prescriber actually has to write

Medicare Part D defines what a prescriber’s supporting statement must address for a Part D tiering or formulary exception. Commercial, employer, Medicaid, and Marketplace plans may ask for similar evidence, but their criteria, forms, and appeal rights are separate and must be checked individually.

Fact 1: A Part D exception can ask them to waive the requirement itself

Most people don’t know this exists.

CMS defines a formulary exceptionunder Medicare Part D as a request to get a drug that isn’t on the plan’s formulary — or to have a utilization management requirement waived. CMS names them specifically: step therapy, prior authorization, quantity limit.

You don’t only get to satisfy the prior authorization. Under Part D, your prescriber can ask the plan to drop it.

Fact 2: On Part D, the clock starts when the supporting statement lands

For a Medicare Part D exception, the normal decision clock begins when the plan receives the prescriber’s supporting statement — not when you first called, and not when the request was opened.

There’s a backstop:under current federal rules, if the supporting statement still hasn’t arrived 14 calendar days after the exception request, the plan must make its determination within 72 hours after that 14-day period ends. So a request doesn’t float outside a clock forever. But it can absolutely sit for two weeks while everyone assumes someone else is waiting.

“Has the plan received the supporting statement yet?”

“What date did the plan record as the original exception-request date?”

Not “any update?” Not “did the prior auth go through?” Those two, exactly.

Medicare Part D exception standards

| Route | Use it when | What the prescriber’s statement must address |

|---|---|---|

| Tiering exception | You want a non-preferred drug at preferred cost-sharing | The preferred drug(s) would not be as effective, would have adverse effects, or both |

| Formulary exception— non-formulary drug | The drug isn’t on the formulary | All covered Part D drugs on any tier would not be as effective or would have adverse effects |

| Formulary exception— waive step therapy | They want you to fail something first | The required alternative has been or is likely to be less effective or have adverse effects |

| Formulary exception— waive quantity limit | The dose cap is too low | The number of doses under the restriction has been or is likely to be less effective |

Source: CMS, Medicare Part D exceptions guidance. Checked July 16, 2026. These are Part D standards. If you have commercial, employer, Medicaid, or Marketplace coverage, ask your plan for its own criteria and forms.

How it can be submitted (Part D):the prescriber’s supporting statement may be given orally or in writing, though the plan may require written follow-up. It can go on CMS’s Model Coverage Determination Request Form, the plan’s own form, or — straight from CMS — any other written document, including a plain letter.

The grid that does the work

Before your prescriber sends anything, get this into the chart:

| Drug tried | Dates | What happened | Specific reaction | Documented in the notes? |

|---|---|---|---|---|

| ☐ | ||||

| ☐ | ||||

| ☐ |

Chart documentation can be decisive. It isn’t the only thing — the indication, the plan’s criteria, the required alternatives, and therapeutic equivalence all weigh in. But it’s the one you can do something about this week.

What to say to the office

That last question is the one nobody asks. Ask it.

One line we won’t cross, and neither should you: never put a diagnosis, a code, a prior treatment, or a reaction into a request that isn’t true and supported by your record. It’s the line between advocating for yourself and misrepresenting your history to an insurer.

How long does a progesterone prior authorization take?

For Medicare Part D coverage determinations, plans generally have 72 hours for a standard request and 24 hours for an expedited request. For Part D exception requests, that period begins when the plan receives the prescriber’s supporting statement, subject to a 14-day backstop. Timelines under Medicaid, Marketplace, Medicare Advantage drug benefits, and commercial plans are program-specific and plan-specific.

| Your coverage | Standard | Expedited | When the clock starts |

|---|---|---|---|

| Medicare Part D— coverage determination | 72 hours | 24 hours | When the plan receives the request |

| Medicare Part D— exception request | 72 hours | 24 hours | When the plan receives the prescriber’s supporting statement; if it hasn’t arrived within 14 calendar days of the request, the plan must decide within 72 hours after that period ends |

| Medicare Part D— payment request (you already paid) | 14 calendar days | — | When the request is received |

| Commercial, employer, Medicaid, Marketplace | Plan- and program-specific | Plan- and program-specific | Ask your plan— and write down the answer |

Source: CMS Part D coverage determination and exception guidance; 42 CFR 423.568. Checked July 16, 2026.

That last row is not us dodging. Prescription drug timelines outside Part D genuinely vary by program, plan, PBM, and state law. Any page that gives you one number for all of them is making it up. Ask your plan what starts its clock and what its deadline is — then write it down.

If a Part D deadline passes

On Medicare Part D, when a plan doesn’t decide within the required timeframe, that’s treated as an adverse determination, and the case must be forwarded to the Independent Review Entity within 24 hours of the deadline expiring. The clock running out doesn’t mean you wait longer. It means you move up a level.

Expedited review: use it honestly

Expedited review exists for situations where waiting could seriously jeopardize your life, health, or ability to regain maximum function. Your prescriber applies that standard. Don’t ask for it just to jump the line.

What to write down on every call

Call log — one index card

- Exact product, strength, quantity, day supply

- Exact rejection wording

- Plan name, formulary name, plan year

- Who you spoke to, and when

- Reference number — always ask for it

- Date submitted, and by whom

- The decision deadline the plan gave you

- Denial reason, if there is one

- The next filing deadline

The reference number is the one people skip. It’s the one that makes the second call take four minutes instead of forty.

What can you do while you wait?

Ask your pharmacist, prescriber, and plan what continuity options exist before you go without. Depending on the plan, options may include a claim correction, a transition or temporary supply, expedited review, or paying cash for the exact prescribed product. Do not stop, split, double, or substitute medication on your own.

Ask about a temporary supply

The UnitedHealthcare Community Plan of Maryland PDL describes a specific one: for a newly prescribed non-formulary drug, when there’s an immediate need and the prescriber can’t be reached, the claim system will accept a one-time 3-day supply.

That’s one Medicaid plan, one narrow situation. It is not a general override for every rejection, every plan, or every refill.

Other real options

- A transition fill. Some plans provide a one-time refill after you enroll, especially early in a plan year. Ask.

- Ask whether the claim just needs re-running.For “diagnosis required” or “refill too soon,” that’s sometimes the entire fix.

- Pay cash for the exact prescribed product— with all the caveats in the section above.

Before you pay cash while a request is pending

- Can I submit a paid claim for reimbursement later?

- Does paying cash affect my pending request?

- Is the pharmacy filling exactly what was prescribed?

- Is this price for the right strength and quantity?

Call your clinician before you change anything. Not the pharmacy. Not us.

What does a peanut allergy mean for Prometrium and generic progesterone?

Prometrium capsules contain peanut oil, and the label lists peanut allergy as a contraindication — meaning Prometrium itself should not be used by someone with that allergy. This is a safety question first and an insurance question second. FDA-approved generics may use different inactive ingredients, so the specific manufacturer being dispensed has to be checked.

Prometrium’s FDA-approved label states that the capsules contain peanut oil and are contraindicated in patients allergic to peanuts.It ’s in the contraindications section, and it’s been there since the original approval.

That is a reason not to take Prometrium. It is not an argument for getting Prometrium covered.

If you have a peanut allergy and you’ve been handed a progesterone capsule, tell your prescriber and your pharmacist today. Before you take it. Not because of insurance — because of the allergy.

Then check the specific product.FDA-approved generics must match the reference product on active ingredient, strength, dosage form, and route — but inactive ingredients can differ by manufacturer. Whether the exact capsule in your bottle contains peanut oil depends on who made it. Your pharmacist can read the label for the product they’re dispensing. Don’t assume in either direction.

Where insurance re-enters:if the plan’s preferred product contains an ingredient you can’t safely take, that’s the kind of documented clinical fact a prescriber may use to request a different appropriate product. The allergy drives the medical decision. The documentation follows it — not the other way around.

Other contraindications on the label

The label also lists, among its contraindications: hypersensitivity to its ingredients; undiagnosed abnormal genital bleeding; known, suspected, or a history of breast cancer; active deep vein thrombosis or pulmonary embolism, or a history of these; active arterial thromboembolic disease such as stroke or heart attack, or a history of these; and known liver dysfunction or disease.

We list these as label facts, not advice. If any describe you, that ’s a conversation with your clinician.

How does Medicare Part D handle progesterone coverage and appeals?

A Medicare Part D formulary may cover generic progesterone, brand Prometrium, or another product, each subject to its own tier and utilization rules. Coverage cannot be inferred from Part D enrollment alone. Part D runs on its own decision timelines and a defined five-level appeal process.

If you’re on Part D, three things are different:

- Coverage is per formulary, not per program. “I have Part D” doesn’t tell you whether your progesterone is covered.

- The clock is defined— 72 hours standard, 24 hours expedited, and for exceptions it starts when the supporting statement lands (with that 14-day backstop).

- The ladder is fixed.Before the appeal levels, there’s the initial coverage determination or exception request — that’s the decision, not an appeal. Then:

| Level | What it is |

|---|---|

| Level 1 | Redetermination by your Part D plan |

| Level 2 | Reconsideration by the Independent Review Entity |

| Level 3 | Hearing before an Administrative Law Judge or attorney adjudicator at the Office of Medicare Hearings and Appeals — requires the amount in controversy to meet a threshold ($200 for 2026) |

| Level 4 | Medicare Appeals Council review |

| Level 5 | Federal district court review — requires a higher amount in controversy ($1,960 for 2026) |

Source: CMS Part D appeals guidance and 2026 amount-in-controversy thresholds. Checked July 16, 2026.

Your denial notice controls everything.It names the specific reason, the filing instructions, and your deadline. File based on what your notice says — not what a website told you, including this one.

The honest warning we owe you

Midi Health — the telehealth provider we mention later on this page — does not work with Medicare or Medicaid. Per Midi’s own published statements: it is not covered by Medicare or any Medicare-related insurance plan, and it is not an enrolled participating provider with state programs like Medicaid or Medi-Cal. It cannot treat Medicaid patients even as self-pay. Medicare beneficiaries can be seen as self-pay patients, but no claims may be submitted for those visits, medications, or associated services.

If you’re on Medicare or Medicaid, Midi is not your route. Don ’t book a visit hoping it works out.

On Medicare? → Medicare and online HRT: what’s covered and how to appeal

On Medicaid? → Medicaid and HRT: state-by-state coverage

What if your prescriber won’t submit the prior authorization?

Prior authorizations impose substantial administrative work that is generally not separately reimbursed, and some practices decline to do it. In the American Medical Association’s survey of 1,000 practicing physicians conducted in late 2024, 93% said prior authorization sometimes, often, or always resulted in care delays.

Let’s be fair to your doctor for a second. This is unpaid administrative work that pulls staff away from patients, and the AMA ’s own data says physicians hate what it does to care. The system is the problem here, not usually the person.

Try these first — they’re all free

- Ask whether the practice has a prior-authorization or medication-access coordinator. Some do. The front desk may not know to route you there.

- Ask whether they can submit it orally.For Medicare Part D exception requests, CMS permits an oral supporting statement, though the plan may want written follow-up. Some offices will make a two-minute call when they won’t touch a fax.

- Ask whether the pharmacy can start an electronic prior authorization that lands in the prescriber’s workflow.

- Ask for the reference number.If they’ve already submitted, you may just need to follow up rather than escalate.

If the practice genuinely won’t do it

Then changing prescribers becomes an option worth weighing — after you’ve confirmed the current practice won’t submit the plan-required documentation, and after you’ve thought about continuity of care. That’s a real cost, not a footnote.

Midi Health — what we verified

This is The HRT Index Verification Standard applied: we read every published claim, separate FDA-approved from compounded, verify state availability and insurance, and re-check on a fixed schedule.

| Claim | Source status |

|---|---|

| In-network with most PPO plans; coverage varies by plan | Provider-stated — Midi pricing & insurance page; checked July 16, 2026 |

| Available in all 50 states | Provider-stated; checked July 16, 2026 |

| Prescribes FDA-approved hormones by default | Provider-stated — Midi HRT page; checked July 16, 2026 |

| Self-pay: $250 initial consultation, $150 follow-up | Provider-stated; checked July 16, 2026 |

| Not covered by Medicare or any Medicare-related plan | Provider-stated; checked July 16, 2026 |

| Not enrolled with Medicaid / Medi-Cal; cannot treat even self-pay | Provider-stated; checked July 16, 2026 |

| Submits pharmacy prior authorizations | ⚠ Not claimed by Midi. Not verified by us. Ask at intake. |

Read that last row, because we’re not going to pretend around it. We are not telling you Midi will handle your prior authorization. Midi doesn’t publicly claim that, and we haven’t confirmed it. Anyone who tells you otherwise is selling you something.

Here’s the honest trade.Midi doesn’t take Medicare or Medicaid — if that’s your coverage, this isn’t your path. But Midi is in-network with most PPO plans in all 50 states and prescribes FDA-approved hormones by default. Those two facts happen to be exactly what determines whether a prescription can be covered at all: a clinician your plan recognizes, writing products your formulary can actually list. A cash-pay clinic writing compounded preparations gives you neither — and compounded products are the ones most likely to be excluded from your benefit outright.

The four questions to ask any provider before you pay

- Do you bill my plan, and are you in network?

- Does your office submit pharmacy prior authorizations, and do you handle appeals and renewals?

- Is that work included in the visit fee?

- Will the prescription go to my local pharmacy — and are the medications FDA-approved or compounded?

Write the answers down. A provider who answers all four clearly is telling you something. So is one who doesn’t.

Affiliate disclosure: The HRT Index may earn a commission if you use the link below, at no additional cost to you. It did not affect what we wrote — on most of this page we’re telling you to check a $12 generic and never click a provider link at all.

Have a PPO plan? Check whether Midi accepts it.

If you have a PPO plan and you need a prescriber who takes it — check whether Midi accepts your insurance. It’s a coverage lookup, not a purchase. Then ask them question 2 above before you book.

Check Midi insurance coverage →What we actually verified

This page is built from primary documents: FDA labels, CMS regulations, published payer policies, published state appeal decisions, and providers’ own published statements. Where we could not verify something, we say so rather than estimating.

What we read ourselves

- CMS's Medicare Part D coverage determination and formulary exception standards, and 42 CFR 423.568

- The FDA-approved Prometrium label, including the indication and contraindications

- The FDA's February 12, 2026 announcement approving labeling changes to six menopausal hormone therapy products

- Mass General Brigham Health Plan's commercial/exchange Bijuva prior authorization policy, effective 09/01/2025

- UnitedHealthcare Community Plan of Maryland's Medicaid Preferred Drug List, effective 07/01/2026 — markers, the diagnosis-required mechanism, generic substitution policy, temporary supply provision, and the oral progesterone row

- Six published New York external appeal decisions, located through the stated search and individually classified by diagnosis, product, coverage type, and outcome

- Cash pricing at two independent sources, on a dated snapshot

- Midi Health's own insurance and pricing pages

What we could NOT verify — and won’t pretend otherwise

- Your plan's rule. We didn't access any member portal or run a live claim. No public document can tell you your coverage.

- A complete picture of how plans treat progesterone. We have real rows from real documents. We do not have a measured sample across the market, which is why you won't find the words "most plans" on this page.

- Employer-specific formulary variations. These are the least public and often the most restrictive.

- Whether every manufacturer's generic progesterone contains peanut oil. Inactive ingredients vary. Ask your pharmacist about the specific product being dispensed.

- Whether Midi Health submits pharmacy prior authorizations. Not claimed by them, not confirmed by us.

- Whether any plan has changed a progesterone rule because of the February 2026 labeling action. None of the policies we reviewed said so.

- Actual approval odds. Nobody can honestly give you a number, and anyone who does is guessing.

- A complete New York appeal dataset. We read six decisions. There are more, and we're working through them.

Update log

| Date | What changed | Sources checked |

|---|---|---|

| July 16, 2026 | Initial publication | CMS Part D standards + 42 CFR 423.568; FDA Prometrium label; FDA Feb 12, 2026 labeling action; Mass General Brigham Bijuva PA policy (eff. 09/01/2025); UHC Community Plan of Maryland Medicaid PDL (eff. 07/01/2026); six NYS DFS external appeal decisions; Drugs.com and GoodRx price snapshots; Midi Health published insurance and pricing pages |

Progesterone prior authorization FAQ

Does progesterone always require prior authorization for menopause?

No. Plans use several distinct restrictions — prior authorization, diagnosis required, quantity limits, step therapy, age and gender limits — and they aren't interchangeable. On the UnitedHealthcare Community Plan of Maryland Medicaid drug list effective July 1, 2026, generic oral progesterone carries a diagnosis requirement and a quantity limit, not a prior authorization. Your rule depends on your exact plan and product.

Why is my progesterone not covered all of a sudden?

Common causes: your plan year changed, your employer changed plans, the pharmacy billed brand instead of generic, your dose changed and tripped a quantity limit, or a prior authorization expired. Ask the pharmacy for the exact rejection wording — that tells you which one it is.

Is generic progesterone the same as Prometrium?

FDA-approved generic progesterone must meet FDA requirements for the same active ingredient, strength, dosage form, route, quality, and bioequivalence to the reference product, and is expected to provide the same clinical effect and safety under labeled conditions. Inactive ingredients can differ by manufacturer, which matters if you have an allergy or intolerance. Compounded progesterone is not an FDA-approved generic and is a separate category.

How much is progesterone without insurance?

On July 16, 2026, Drugs.com listed generic progesterone 30 × 100 mg from $11.77 and 30 × 200 mg at $17.54–$24.50, and GoodRx displayed a lowest price of $14.10 against an average retail price of $60.73. These are price-guide and savings-program figures, not guaranteed local prices. Check your strength, quantity, and pharmacy.

How long does a progesterone prior authorization take?

For Medicare Part D, plans generally have 72 hours for a standard coverage determination and 24 hours for an expedited one. For Part D exception requests, that period starts when the plan receives the prescriber's supporting statement — with a rule that if the statement hasn't arrived within 14 calendar days of the request, the plan must decide within 72 hours after that period ends. Commercial, employer, Medicaid, and Marketplace drug timelines are plan-specific: ask your plan and write down the answer.

Who submits the prior authorization — me, the pharmacy, or my doctor?

When the plan wants clinical support, that generally has to come from your prescriber. The pharmacy can identify the rejection and often start an electronic request. Under Medicare Part D, you, your prescriber, or your representative can request a coverage determination — but the prescriber's supporting statement is what the plan decides on.

What is a formulary exception?

Under Medicare Part D, it's a request for the plan to cover a drug that isn't on its formulary — or to waive a requirement such as step therapy, prior authorization, or a quantity limit. The prescriber must submit a supporting statement addressing why covered alternatives wouldn't be as effective or would cause adverse effects. Other plan types may use similar concepts under their own rules.

Can my doctor ask them to waive the prior authorization entirely?

Under Medicare Part D, yes — CMS defines a formulary exception to include requests to waive a utilization management requirement, and names prior authorization specifically. Most people never ask, because almost nobody knows it's an option. For other plan types, ask your plan whether it offers an equivalent.

What does "diagnosis required" mean?

The plan's claim system checks whether a matching diagnosis is on file. If it isn't found in your medical or pharmacy claim, the prescription rejects at the counter. Sometimes the pharmacy or prescriber can simply transmit the documented diagnosis. If the diagnosis doesn't meet the plan's rule, a prior authorization review may still be needed — ask which situation you're in.

Can the pharmacy just give me the generic instead of Prometrium?

Only if your prescription allows substitution. If it's marked "dispense as written" or "brand medically necessary," the pharmacy cannot substitute regardless of cost — your prescriber would need to authorize a change or write a new prescription. Ask the pharmacy which applies to yours.

Can insurance make me try a different progestogen first?

A plan can apply step therapy or generic-first rules. That's a payment rule, not a treatment instruction. Whether a preferred alternative is right for you is a decision for you and your prescriber. Ask the plan exactly which drug, at what dose, for how long, and what counts as completing the step.

What happens if my progesterone prior authorization is denied?

Read the denial notice first — it names the specific reason, the filing instructions, and your deadline. Answer that reason directly, with your prescriber's factual support and the records that back it up. Commercial, Medicare, Medicaid, employer, and self-funded plans run different processes with different rights.

Can I appeal a denial and win?

Sometimes. Some denials are eligible for external review by an independent reviewer after the required internal process, though eligibility, deadlines, and effect depend on your plan, state, and denial type. In the New York decisions we read, the one that was overturned documented every alternative tried, with specific named reactions, in the medical record.

Does Medicare cover Prometrium?

A Part D formulary may cover generic progesterone, brand Prometrium, or another product, each with its own tier and utilization rules. Coverage can't be inferred from Part D enrollment alone — check your exact plan, product, strength, and current formulary.

Is compounded progesterone covered by insurance?

Some plans exclude compounded products from the pharmacy benefit; others cover them only under narrow rules. Ask whether your rejection is a benefit exclusion, a non-formulary decision, or a documentation issue. Separately: compounded drugs are not FDA-approved, and we don't present them as interchangeable with FDA-approved progesterone.

Can I pay cash while my request is pending?

Often, yes. First ask whether you can submit for reimbursement later, whether it affects the pending request, and whether the pharmacy is filling exactly what was prescribed. Note that a discount-card transaction generally bypasses the insurance claim, so it may not be credited toward your deductible or out-of-pocket maximum — ask your plan whether it accepts a member-submitted claim.

Should I stop my estrogen if my progesterone is denied?

Call your prescriber today. That's a clinical decision and it isn't one to make from a pharmacy parking lot. Tell the office your fill was blocked and ask what they want you to do while it's sorted out. If you're having emergency symptoms, get emergency care instead of waiting on any of this.

My prior authorization expired. Now what?

Ask the plan for the previous approval's start and end dates, the renewal criteria, and the submission route. Continuation criteria are sometimes different from initial approval criteria, so a renewal isn't always a formality.

Does a peanut allergy matter?

Yes. Prometrium contains peanut oil and its label lists peanut allergy as a contraindication — meaning it shouldn't be used by someone with that allergy. Tell your prescriber and pharmacist before taking it, and ask about the specific generic product being dispensed, since inactive ingredients vary by manufacturer.

Does a hysterectomy change whether I need progesterone?

It can change the clinical picture significantly. That decision belongs to you and your clinician — this is a coverage page and we're not going to answer it for you.

Three things to do next

- Call the pharmacy. Ask what exactly rejected, and exactly what product they billed. Then ask whether your prescription allows a generic. Two questions, one call.

- Match the answer to the table at the top of this page. Confirm your exact plan, its formulary effective date, and the product before you switch, pay cash, or appeal. The wrong process costs more time than the right one.

- If a request is already in, ask the plan two things: has it received the prescriber’s supporting statement, and what date did it record as the original request date? On Part D that’s what starts the clock. On other plans, ask what does.

You didn’t do anything wrong. This is a payment rule, not a judgment about you or your treatment. It’s a system that’s frustrating by design, and the women who get through it fastest are just the ones who found out which door they were actually standing in front of.

Now you know how to find out.

Still not sure which HRT program is right for you?

Take our free 90-second matching quiz to find the provider that fits your situation, your plan, and your state.

Find My HRT Path →Sources

Federal regulation

- CMS — Coverage Determinations, Medicare Part D

- CMS — Exceptions, Medicare Part D

- 42 CFR § 423.568 — Part D coverage determination timeframes

- CMS — Medicare Part D appeals process and 2026 amount-in-controversy thresholds

FDA

- FDA — FDA Approves Labeling Changes to Menopausal Hormone Therapy Products, February 12, 2026

- FDA — PROMETRIUM (progesterone) capsules label, NDA 019781

- FDA — Compounding and the FDA: Questions and Answers

- FDA — Orange Book Preface (therapeutic equivalence and generic standards)

Published appeal decisions — New York State Department of Financial Services public external appeal database

- Case 202302-158900 — Prometrium, menopause, upheld, 2023

- Case 202207-151963 — Prempro, menopause, upheld, 2022

- Case 202009-131454 — Vivelle-Dot, premature menopause, upheld, 2020

- Case 202103-136077 — Intrarosa, menopausal atrophic vaginitis, upheld, 2021

- Case 202104-137028 — Osphena, postmenopausal atrophic vaginitis, upheld, 2021

- Case 202108-140606 — Estring, genitourinary syndrome of menopause, overturned, 2021

Payer documents

- Mass General Brigham Health Plan — Bijuva (estradiol and progesterone) commercial/exchange prior authorization policy, effective 09/01/2025

- UnitedHealthcare Community Plan of Maryland — Medicaid Preferred Drug List, effective 07/01/2026

Pricing (snapshot July 16, 2026)

- Drugs.com Price Guide — progesterone

- GoodRx — progesterone

Provider

- Midi Health — published pricing, insurance, and HRT pages (checked July 16, 2026)

Other

- American Medical Association — 2024 prior authorization physician survey (n=1,000)