Reader-supported. Affiliate disclosure. Some links on this page may earn a commission if you start care through them, at no cost to you. Affiliate relationships do not determine evidence, conclusions, or order of appearance.

Is this page for you?

| ✅ Yes, if | ❌ No — try this instead |

|---|---|

| Your pharmacy said “prior authorization” or “not covered” | You’re deciding whether to start HRT → What is HRT? |

| You got a denial letter you can’t decode | You’re choosing patch vs. pill vs. gel → Estradiol patch guide |

| Your patch got swapped to a different brand, then rejected | You want cash-pay HRT and are skipping insurance → Online HRT costs |

| Your patch stopped being covered on January 1 | You just need a pharmacy that has stock → Patch shortage guide |

| You’re on Medicare, Medicaid, commercial, Marketplace, FEHB, or TRICARE | You’re outside the United States |

One thing we won’t do: tell you to change your dose, your patch schedule, or your medication. That’s your prescriber’s call, not a website’s. What we will do is hand you the exact words that unstick a claim.

The four-second version

Here’s the whole page in one table. Find your row.

| What you were told | What may have fired | What to ask for |

|---|---|---|

| “Needs prior authorization” | A quantity limit — not always a medical review | A one-time quantity override |

| “Too soon to refill” | A refill timing edit | Reverse and rebill |

| “Not covered” | Non-formulary — often brand vs. generic | The generic, or a formulary exception |

| “Your copay is $180” | Tier placement | A tiering exception |

| “Try something else first” | Step therapy | The documented trial, or an exception |

| “Prior authorization required” | Clinical review | A medical necessity submission |

These are the likely causes, not a diagnosis. The rejection code on your claim is what actually decides. Getting that code is step one.

What does “prior authorization” actually mean at the pharmacy counter?

Prior authorization is a rule requiring a health plan to approve a medication before it will pay. At the pharmacy counter, the phrase is often used for any rejected claim, including quantity limits, refill timing edits, formulary exclusions, and tier problems, which are not prior authorizations and are resolved differently. Identifying the specific rejection code determines which fix applies.

Your pharmacist isn’t lying to you. She’s reading a code.

When a claim rejects, the pharmacy system spits back a short message. It might say “PA required.” It might say “plan limitations exceeded.” The tech reads it, translates it into the phrase most people recognize — “prior authorization” — and moves to the next person in line.

That translation costs you weeks.

Because if your problem is a quantity limit, and you go home and wait for a “prior authorization” that nobody filed, you will wait a long time for nothing. The fix was a phone call.

The eight rejections, decoded

| # | What you heard | What it may be | Why it happens | The exact ask | Who does it |

|---|---|---|---|---|---|

| 1 | “Needs prior authorization” | Quantity limit (some plans call it Drug Quantity Management) | You went over the patches-per-28-days cap — sometimes because a brand swap stacked two products in one month | “Request a one-time quantity override for a mid-month product change” | Prescriber’s office → your plan |

| 2 | “Too soon to refill” | Refill-too-soon edit | You filled early, or a dose change reset your timing | “Reverse and rebill” or “request an early refill override” | Pharmacy first, then plan |

| 3 | “Not covered” | Non-formulary — often a brand when a generic exists | Your prescriber wrote Climara or Vivelle-Dot; your plan covers the generic | Take the generic, or request a formulary exception | Prescriber |

| 4 | “Covered — copay is $180” | Tier placement | It’s covered. Just on a punishing tier. | Request a tiering exception | Prescriber |

| 5 | “Try something else first” | Step therapy | Plan wants a lower-cost option documented first | Do the documented trial, or request a step therapy exception | Prescriber |

| 6 | “Prior authorization required” | Clinical review | Off-label use, indication mismatch, or a coverage criterion | Full medical necessity submission | Prescriber |

| 7 | “NDC not covered” | Product-level exclusion | Your plan may cover Sandoz’s patch and not Zydus’s (NDC = National Drug Code, identifying exact product and manufacturer) | Ask which NDCs are covered, then have the prescription written to match | Pharmacy + prescriber |

| 8 | “Invalid day supply” | Data entry | Someone typed 30 days for a twice-weekly patch when the box holds 8 patches for 28 days | “Please correct the day supply and resubmit” | Pharmacy |

Why did estradiol patch problems get so much worse in 2026?

In November 2025 the FDA initiated removal of boxed warning statements about cardiovascular disease, breast cancer, and probable dementia from menopausal hormone therapy labeling, and approved the first six product label changes on February 12, 2026. Demand for estrogen patches has since outpaced supply, and pharmacies have substituted available brands. Under some plan policies, weekly and twice-weekly patches count against a single combined quantity limit, so a mid-month substitution can push a claim over that limit.

You did nothing wrong. The system moved, and you got the bill.

The chain, step by step

Step 1 — November 10, 2025.The FDA announced it was starting to remove the “black box” warnings from menopause hormone therapy — the most prominent safety warnings the FDA issues. They had been on estrogen since the early 2000s and scared a generation of women and doctors away from HRT.

Step 2 — February 12, 2026. The FDA approved labeling changes for six menopausal hormone therapy products, removing risk statements about cardiovascular disease, breast cancer, and probable dementia from the boxed warning. Those risks weren’t erased from the label — they were moved out of the most prominent warning box. The full prescribing information still discusses risks. The FDA said 29 drug companies have submitted proposed labeling changes at its request.

Step 3 — Demand went vertical. Estrogen patch prescriptions climbed 162% over two years, according to HealthVerity data reported by CNBC. Among women 45 to 54, estrogen-based prescriptions rose 184% since 2018, per Truveta data reported by NBC News.

Step 4 — Supply didn’t follow. Patches are complex dosage forms requiring specialized manufacturing, and industry capacity is finite. The American Society of Health-System Pharmacists has listed estradiol patches from Amneal, Noven, Sandoz, and Zydus in shortage — NBC News reported ASHP listing 14 brands or dosages.

Step 5 — Pharmacies started substituting.Climara this month. Vivelle-Dot next month. Whatever’s on the shelf.

Step 6 — The trap sprang.

The accumulator problem

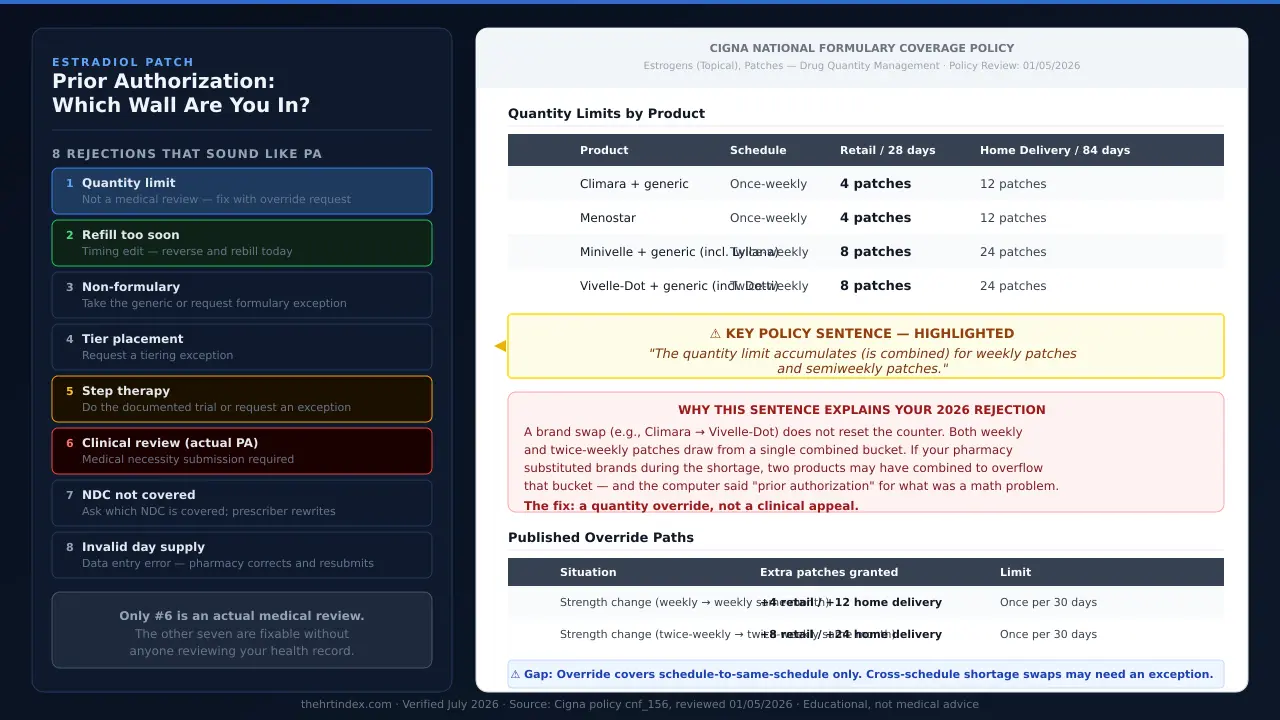

We pulled Cigna’s national coverage policy for estrogen patches — a public document, reviewed January 5, 2026. Buried in the quantity table is one sentence that explains a lot of 2026:

Under that published policy, “Climara patches” and “Vivelle-Dot patches” don’t get counted separately. They get counted as patches. One bucket.

Caveat from Cigna’s own document: your individual benefit plan can override their national policy. Confirm with yours.

The published override — and the gap in it

| Your patch type | What triggers the override | What you get | Limit |

|---|---|---|---|

| Weekly (Climara, Menostar) | Changing strengths to another once-weekly patch in the same month | +4 patches retail · +12 home delivery | One override per 30 days |

| Twice-weekly (Vivelle-Dot, Minivelle, Dotti, Lyllana) | Changing strengths to another twice-weekly patch in the same month | +8 patches retail · +24 home delivery | One override per 30 days |

What it means for you:if your swap crossed schedules, the routine override may not fit. The stronger path is a quantity or formulary exception based on medical necessity, citing documented supply problems — not a routine override request.

This is The HRT Index’s reading of a published policy. It is not a position Cigna has stated, and it is not a prediction of what your plan will do.

Cigna’s standing quantity limits

| Product | Strengths (mg/24hr) | Box | Schedule | Retail max / 28 days |

|---|---|---|---|---|

| Climara (+ generic) | 0.025 / 0.0375 / 0.05 / 0.06 / 0.075 / 0.1 | 4 | Weekly | 4 patches |

| Menostar | 0.014 only | 4 | Weekly | 4 patches |

| Minivelle (+ generic, incl. Lyllana) | 0.025 / 0.0375 / 0.05 / 0.075 / 0.1 | 8 | Twice weekly | 8 patches |

| Vivelle-Dot (+ generic, incl. Dotti) | 0.025 / 0.0375 / 0.05 / 0.075 / 0.1 | 8 | Twice weekly | 8 patches |

- Climara Pro (estradiol/levonorgestrel) is subject to quantity limits but is not included in the override criteria in that policy. If you’re on Climara Pro and hit a quantity wall, the routine override door isn’t there. You go to exception or appeal.

- Menostar’s only override in that policy is a strength change. Nothing else.

Does every plan handle estradiol patches the same way?

No. Published 2026 plan documents show estradiol patches treated three different ways: listed as preferred with no criteria on Oregon’s Medicaid preferred drug list, subject to step therapy requiring a documented generic patch trial under one Federal Employee Health Benefit plan, and subject to combined quantity limits under Cigna’s national formulary policy. The insurer’s name alone does not determine the rule.

Same patch. Three plans. Three different walls.

| Plan | What it covers | The gate | The exact rule they published | Effective / reviewed |

|---|---|---|---|---|

| Oregon Health Plan (Medicaid) | Vivelle-Dot, Minivelle, Lyllana, Dotti, Climara, generic weekly, generic twice-weekly | None listed. All shown as preferred (“Y”) with no drug use criteria attached | On that list, preferred means no prior authorization for that product | Current, checked July 2026 |

| Western Health Advantage (FEHB plan) | Minivelle, Menostar, Alora, Vivelle-Dot | Step therapy | FDA-approved indication AND “Trial and failure of a minimum 28-day supply or intolerance to generic estradiol patch.” Approval lasts 12 months | Effective Jan 1, 2026 · P&T approved Nov 20, 2025 |

| Cigna | Climara, Menostar, Minivelle, Vivelle-Dot (+ generics) | Quantity limit, combined across weekly and twice-weekly | 4 patches / 28 days (weekly) · 8 patches / 28 days (twice-weekly), retail | Policy reviewed Jan 5, 2026 |

A woman on Oregon Medicaid walks into a pharmacy and her Vivelle-Dot pays. No questions. A woman on that FEHB plan needs her chart to show she tried a generic patch for 28 days first. A woman on Cigna gets it, until a brand swap pushes her over a combined patch count.

That’s why the internet’s generic “how to appeal a prior authorization” advice fails you. There is no one wall.

One pattern showed up more than once

| Product | Oregon Medicaid | Cigna | Cigna indication |

|---|---|---|---|

| Vivelle-Dot, Minivelle, Dotti, Lyllana, Climara | Preferred, no criteria | Standard quantity limit, with overrides | Multiple indications |

| Menostar | Non-preferred (age restriction criteria) | Narrowest override — strength change only | Osteoporosis prevention only |

| Climara Pro | Non-preferred (age restriction criteria) | Not in the override criteria | Combo product |

If you’re on Menostar or Climara Pro, expect more friction than a woman on Vivelle-Dot.Not because there’s anything wrong with your prescription — because in the documents we read, payers put these two in a different bucket.

The Menostar trap specifically

Cigna’s policy says Menostar is the only estrogen patch with a single indication: prevention of postmenopausal osteoporosis.That’s it. Bone protection. So if Menostar was prescribed for your hot flashes, that’s off-label — a legitimate reason for a plan to deny. If you’re on Menostar and got denied, ask your prescriber whether Menostar is the right product for what you’re actually treating.

The right online HRT provider isn’t the same for every woman.

It depends on your symptoms, your age and whether you have a uterus, your medication route preference, your risk history, your insurance or cash-pay situation, and your state. Some situations belong with an in-person clinician first.

Use The HRT Index’s Find My HRT Path tool to match your situation to the right provider — and to flag when online care isn’t the right starting point.

Free · No email required · Takes about 90 seconds

How do I know which type of plan I have?

Coverage rules and appeal deadlines for prescription drugs depend on plan type. Medicare Part D and Medicare Advantage drug coverage follow Part D rules. Employer coverage generally follows ERISA claims rules, and self-funded employer plans are not regulated by state insurance departments. Marketplace and individual policies follow Affordable Care Act rules. Plan documents and member ID cards identify which applies.

Everything below — your deadline, your appeal path, whether external review is even available — depends on this answer.

| Look for | You’re probably on |

|---|---|

| A red-white-and-blue Medicare card, or a Medicare Advantage card, and a separate drug plan | Medicare Part D or MA-PD |

| Coverage through your job or your spouse’s job | Employer / ERISA — ask HR the next question |

| You bought it yourself on HealthCare.gov or a state exchange | Marketplace / individual |

| A state Medicaid card (Medi-Cal, OHP, etc.) | Medicaid |

| A federal employee plan | FEHB |

| A military card | TRICARE |

“Is our health plan self-funded or fully insured?”

Self-funded means your employer pays the claims and the insurer just administers them — and those plans generally aren’t regulated by your state insurance department, so state appeal help may not apply to you. Fully insured means the insurance company carries the risk, and state rules generally do apply.

Ask now. It’s a lot easier than finding out mid-appeal.

Which estradiol patch am I actually on?

Climara and Menostar are once-weekly patches. Vivelle-Dot and Minivelle are twice-weekly. Dotti and Lyllana are FDA-approved generic estradiol transdermal systems from Amneal, approved through the abbreviated new drug application (ANDA) pathway. Available strengths differ between weekly and twice-weekly products, which affects whether a same-strength substitution exists.

| Product | Maker | Regulatory status | Schedule | Strengths (mg/24hr) |

|---|---|---|---|---|

| Climara | Bayer | Brand (generic available) | Weekly | 0.025 / 0.0375 / 0.05 / 0.06 / 0.075 / 0.1 |

| Menostar | Bayer | Brand | Weekly | 0.014 only |

| Vivelle-Dot | Noven / Sandoz | Brand (NDA) | Twice weekly | 0.025 / 0.0375 / 0.05 / 0.075 / 0.1 |

| Dotti | Amneal | FDA-approved generic (ANDA) | Twice weekly | 0.025 / 0.0375 / 0.05 / 0.075 / 0.1 |

| Minivelle | Noven | Brand | Twice weekly | 0.025 / 0.0375 / 0.05 / 0.075 / 0.1 |

| Lyllana | Amneal | FDA-approved generic (ANDA) | Twice weekly | 0.0375 / 0.05 / 0.075 / 0.1 |

| Climara Pro | Bayer | Brand (estradiol + levonorgestrel) | Weekly | Combination product |

| Alora | — | See note | — | — |

About Alora:Cigna’s policy removed Alora and marked it obsolete. Western Health Advantage’s FEHB criteria — effective January 1, 2026 — still lists Alora as a target for step therapy. We could not confirm its current U.S. marketing status from a primary source, so we’re reporting the discrepancy. Payer paperwork lags the market.

If you’re on Climara 0.06, read this

Climara has a 0.06 mg/24hr patch. Scan the twice-weekly rows. There isn’t one. No twice-weekly patch is made in 0.06.

So if you’re on Climara 0.06 and your pharmacy runs out of weekly patches, there is no same-strength twice-weekly counterpart. Any switch involves a clinical decision your prescriber has to make.

What should I say at the pharmacy counter right now?

Before leaving the pharmacy, ask for the exact rejection code and message, the product and National Drug Code submitted, and the quantity and day supply on the claim. Pharmacy staff can typically see this information on the claim screen. These details determine which fix applies and whether the problem is administrative or clinical.

Don’t leave without these answers. You will not get them as easily over the phone.

“Can you read me the full rejection message and the code? What product, manufacturer, and NDC did you submit? What quantity and day supply? And does the claim show a prior authorization, a quantity limit, refill-too-soon, or something else?”

Four questions. Thirty seconds.

“Can you reverse and rebill it? And can you run it as cash so I can see that price?”

- Reverse and rebill can fix typos and timing problems on the spot. If someone entered 30 days for a twice-weekly patch, this catches it.

- Run it as cash tells you your exit price in ten seconds. You might find your patch costs less than you feared and this entire fight is optional.

If they say “NDC not covered,” ask one more: “Which estradiol patch NDCs does my plan cover?”Pharmacy staff can often look this up. Then your prescriber can write to match — which is a lot faster than an appeal.

Seriously. Refill-too-soon usually means you filled early — very common right now, because women are grabbing patches whenever a pharmacy actually has them. It’s a timing edit. The pharmacy or plan can often override it directly. Ask, fix it, go home.

What does my prescriber actually need to send?

A prior authorization or exception request must identify the exact product, strength, frequency, quantity, day supply, and the specific plan criterion at issue. Under 42 CFR 423.568, the decision timeframe for a Medicare Part D exception request begins when the plan receives the prescriber’s supporting statement. If no supporting statement arrives within 14 calendar days of the request, the plan must still issue a decision no later than 72 hours after that period ends.

The starting gun nobody tells you about

For a Medicare Part D exception request, the plan’s clock doesn’t start when your doctor faxes the form. It starts when the plan receives the prescriber’s supporting statement.

So the real math is roughly 3 days versus roughly 17 days. Not 3 days versus infinity.

Call your plan and ask: “Have you received my prescriber’s supporting statement, and what date did you receive it?”

Use the right words

If you tell your prescriber’s office “the insurance needs a prior auth,” they’ll file a prior auth. If your problem is a quantity limit, that prior auth goes nowhere.

| Your gate | What to ask your prescriber for |

|---|---|

| Quantity limit | “A one-time quantity override for a mid-month product change” |

| Non-formulary brand | “A formulary exception” — or just take the generic |

| Bad tier | “A tiering exception” |

| Step therapy | “A step therapy exception” — or do the documented trial |

| NDC not covered | “Rewrite to a covered NDC” |

| Clinical PA | “A medical necessity submission with the plan’s criterion answered” |

Get the criterion before they write

Here is a real one — published and current. Western Health Advantage’s FEHB criteria for brand estradiol patches says approval requires:

- Use for an FDA-approved indication, AND

- Trial and failure of a minimum 28-day supply, or intolerance to, a generic estradiol patch

Approval then lasts 12 months. That’s their published guideline (GL-448214), effective January 1, 2026, approved by their pharmacy committee November 20, 2025.

If that were your plan, you’d now know the exact sentence your chart needs. Not “medically necessary” — that’s vague and it loses. Something like: tried generic estradiol transdermal for 28 days beginning [date], with [documented outcome].

“Please send me the coverage criteria and the prior authorization form for estradiol transdermal patches, and tell me where my prescriber submits it.”

If your prescriber’s office won’t file this

Some offices are drowning. Some don’t have staff for pharmacy benefit paperwork. Some specialists are booked past the point where you’d run out.

Midi Healthstates it is in-network with most PPO plans, operates in all 50 states, and prescribes FDA-approved HRT. The relevant part: Midi bills commercial insurance. That’s the business model — which means formularies, tiers, and prior authorizations are a routine operating problem for them rather than someone else’s department.

If you’re on Medicare or Medicaid, skip this and see the Medicare section below. → HRT insurance coverage guide

You don’t have to decide anything right now. But it takes about a minute to find out if they’re in-network with your plan, and knowing that before you need it is worth the minute.

Commercial PPO coverage, and a prescriber who won’t file this?

Midi is built around billing commercial insurance — formularies, tiers, and prior authorizations are the core of what they do. Check whether they’re in-network with your plan before you need it.

Check whether Midi is in-network with your plan →Affiliate link. We may earn a commission. The Medicare/Medicaid limits above don’t change because of it.

How long does my plan legally have to decide?

Decision deadlines for prescription coverage are set by federal regulation and vary by plan type. Medicare Part D plans must decide standard requests within 72 hours and expedited requests within 24 hours. Group health and Marketplace plans must decide urgent pre-service claims within 72 hours and non-urgent pre-service claims within 15 days, with one possible 15-day extension. Missing a deadline can create additional appeal rights.

Your deadline isn’t a favor. It’s regulation. Find your row.

| Your plan | Standard | Expedited | What starts the clock | If they blow it | Time to appeal |

|---|---|---|---|---|---|

| Medicare Part D / MA-PD | 72 hours | 24 hours | ⚠ For exceptions: when the plan gets your prescriber’s supporting statement (with a 14-day backstop) | Counts as a denial; must forward to the independent review entity within 24 hrs | 65 days from the date on the notice |

| Part D — first appeal (redetermination) | 7 days | 72 hours | Receipt of request | Forwards to review contractor | — |

| Part D — second appeal (IRE) | — | — | — | — | 60 days from Level 1 decision |

| Employer / ERISA | 15 days (pre-service), extendable once by 15 days | 72 hours (urgent) | Receipt of claim | May be deemed exhausted | At least 180 days |

| Marketplace / individual | Same — but one internal appeal | 72 hours | Receipt of claim | May be deemed exhausted | At least 180 days |

| External review | 45 days | 72 hours | Reviewer gets request | Reviewer may reverse | 4 months from denial |

Your denial letter has to contain specific things

Federal rules require a denial notice to include the denial code and what it means, plus a description of the standard the plan used. If your letter doesn’t have those, that’s a procedural problem you can name in writing.

You can also request the diagnosis code and treatment code attached to your claim — and asking for them doesn’t count as filing an appeal.That’s written into 45 CFR 147.136. Ask freely.

A missed deadline can be a lever

Group health and Marketplace plans: if the plan fails to strictly follow the requirements, your internal appeals may be deemed exhausted— meaning you can go straight to an outside reviewer who doesn’t work for them. There’s a limited exception for minor violations during a good-faith process, but if it’s a pattern, that exception doesn’t apply.

Medicare Part D: a missed deadline counts as a denial and the plan must forward your case to an independent review entity within 24 hours.

Can I make them decide faster?

Under 45 CFR 147.136, whether a claim involves urgent care is determined by the attending provider, and the plan or issuer must defer to that determination. A prescriber’s urgency designation can move a group health pre-service claim from a 15-day decision to a 72-hour decision. Federal rules also allow an expedited internal appeal and an expedited external review to be requested at the same time.

Yes. And almost nobody knows how.

Your prescriber decides if it’s urgent. Not your insurance company.

“a claim involving urgent care has the meaning given in 29 CFR 2560.503-1(m)(1), as determined by the attending provider, and the plan or issuer shall defer to such determination of the attending provider.”

Not the insurer’s reviewer. Not a nurse in a call center. Your prescriber. And the plan shall defer. That’s not a suggestion — it’s in the Code of Federal Regulations. It can turn 15 days into 72 hours.

Run both clocks at once

Most people appeal, wait, get denied, then file for external review. Sequential. Slow. You may not have to. Federal rules say exhaustion of internal appeals isn’t required where you applied for expedited external review at the same time as your expedited internal appeal. 45 CFR 147.136(c)(2)(iii). Two clocks. Running together.

How do I check the status without losing my mind?

Prior authorization and exception requests can stall between the prescriber’s office, the pharmacy, and the plan without any party notifying the patient. Confirming receipt dates directly with the plan identifies where a request is stuck. Under Medicare Part D rules, an enrollee, the prescriber, or an appointed representative may request a coverage determination.

Nobody calls you. Your request can sit in a fax queue for nine days and no system on earth will tell you. So call. Once a week. Same three questions, every time.

- “Has a request been received for estradiol transdermal patches? What date?”

- “Has my prescriber’s supporting statement been received? What date?”

- “What’s the decision deadline, and what’s the reference number for this request?”

Write down: date, time, who you spoke to, reference number. That log isn’t busywork. If this ends up in an appeal, the log is your evidence.

“Was the supporting statement sent, and to which fax or portal?”

Between those two calls, you’ll find the gap in about ten minutes. It’s almost always a gap. You’re allowed to do this. On Part D, you, your prescriber, or someone you appoint can request a coverage determination. You are not going over anyone’s head. You’re a party to your own case.

What if I’m on Medicare Part D?

Under 42 CFR 423.120(b)(3), Medicare Part D plans must maintain a transition process providing a temporary supply of drugs that are not on the plan’s formulary, including formulary drugs subject to prior authorization or step therapy, within the first 90 days of coverage under a new plan. Many plan transition policies also extend this to plan-imposed quantity limits and to current enrollees affected by formulary changes across contract years.

If your patch was covered in December and stopped being covered in January, this section is for you.

The transition fill

Federal regulation requires your Part D plan to have a transition process that gives you a temporary supply while you sort out a drug that’s off-formulary — or that’s on the formulary but blocked by prior authorization or step therapy. 42 CFR 423.120(b)(3). Many plans go further in their published transition policies and apply it to plan-imposed quantity limits too — and to current enrollees hit by a formulary change across plan years.

“Is this eligible for a transition fill?”

Your plan also has to notify you in writing within 3 business days of that temporary fill, and that notice must explain your right to request an exception. If you never got a letter, say so. A month is enough time to fight properly instead of panicking.

If you’re on Medicare or Medicaid — the honest routing

Midi cannot treat Medicaid or Medi-Cal patients at all — not even as a self-pay patient. That’s Midi’s own published policy.

What if it’s actually denied?

A denial begins a defined appeals process with deadlines set by federal regulation. External review is conducted by an independent organization, is reviewed without being bound by the plan’s earlier decision, and is binding on the insurer. Federal standards prohibit a minimum dollar threshold for external review eligibility.

First: figure out whether you were actually denied, or whether something was just wrong.

| What happened | What you do |

|---|---|

| Wrong NDC, quantity, or day supply | Fix the claim. Not an appeal. |

| A document didn’t get sent | Resubmit. Not an appeal. |

| Form went to the wrong fax | Resend. Not an appeal. |

| Plan says a criterion wasn’t met | Now you appeal. |

| Brand denied, generic covered | Take the generic or request a formulary exception |

| Denied after clinical review | Internal appeal → external review |

Plenty of “denials” are the top three rows. Check before you fight.

What goes in the appeal

Keep it boring and complete. Boring wins.

- The denial letter, and the denial code

- The plan’s own criterion, quoted, with your facts answered against it point by point

- Your prescriber’s supporting statement

- Chart documentation of anything the criterion asks about — trials, dates, outcomes

- Your call log

- If it’s urgent: your prescriber’s urgency determination, stated plainly

Don’t write an essay about how you feel. Write the criterion, then write how you meet it. That’s it.

Five things about external review nobody tells you

You have 4 months from your denial notice to file. Standard decisions come within 45 days; expedited within 72 hours. And you can appoint a representative — like your doctor — to file it for you.

If you live in Alabama, Florida, Georgia, Texas, Wisconsin, or a U.S. territory other than Puerto Rico— and your plan uses the HHS-Administered Federal External Review Process (FERP) — that process is temporarily unavailable as of July 1, 2026.

HHS says its team is working on a solution and will provide information about extending deadlines for people who were eligible. If that’s you: don’t assume you have no path. Many plans in those states don’t use FERP — they contract with an independent review organization or use a state process instead. Follow the instructions in the notice from your plan.

We’re flagging this because generic “just file for external review” advice is currently wrong for a lot of people.

What if I’m going to run out before this is resolved?

Interruptions in hormone therapy are a clinical issue that should be directed to the prescriber, who can assess options including alternative formulations. Federal regulation requires Medicare Part D plans to maintain a transition process for a temporary supply in defined circumstances. Discount-card cash prices and manufacturer copay programs may also be available depending on plan type.

Tell your prescriber you’re running out. Today. Not when you’re on your last patch. That’s not an insurance question — it’s a clinical one, and she has options you don’t.

While you’re waiting, three things are actually available:

- The cash price. Ask the pharmacy to run it as cash. For a lot of women this ends the emergency in about ninety seconds. See the numbers below.

- A transition fill, if you’re on Part D and the circumstances fit. Say the words at the counter.

- A manufacturer copay program, if you have commercial insurance and you’re on a brand. Not if you’re on Medicare, Medicaid, TRICARE, or VA — federal anti-kickback rules constrain manufacturer cost-sharing support for federal healthcare program beneficiaries, and the card terms will say so.

Call her today.

What does it cost to just pay cash instead?

Published pharmacy pricing lists generic estradiol transdermal patches starting at approximately $36 to $56 per 30-day supply depending on strength and dosing schedule. Discount card prices cannot be combined with insurance benefits, and cash payments are not automatically credited toward a plan deductible or out-of-pocket maximum.

| What | Published cash price | Source |

|---|---|---|

| Generic patch, twice-weekly (8 patches, 0.025mg) | from ~$35.83 | Drugs.com price guide |

| Generic patch, twice-weekly (8 patches, 0.05mg) | from ~$44.15 | Drugs.com price guide |

| Generic patch, weekly (4 patches, 0.05mg) | from ~$56.38 | Drugs.com price guide |

| Generic estradiol, twice-weekly 0.05mg (8 patches) with discount coupon | ~$36.23 (vs. avg retail ~$104.43) | GoodRx |

Read that first row again. About $36. You can very likely walk into a pharmacy today, pay less than a nice dinner, and go home with patches. Then fight the claim on your schedule instead of theirs. You are not trapped.

Four catches — all of them real

- 1. You can’t stack a discount card with insurance. Cash-pay programs and insurance are one or the other on any given fill.

- 2. Cash isn’t automatically credited toward your deductible or out-of-pocket maximum. If you’re on a high-deductible plan working toward that number, ask before you make cash your default all year.

- 3. Manufacturer copay cards generally exclude Medicare, Medicaid, TRICARE, and VA. Read the terms. If you’re on Part D, the “just use the savings card!” advice on every other page isn’t for you.

- 4. A different formulation isn’t a pricing decision. Oral estradiol is cheaper. It’s also metabolized differently. That’s a conversation with your prescriber, not a budgeting move.

Do the new 2026 prior authorization rules help me?

No. The CMS Interoperability and Prior Authorization final rule (CMS-0057-F), whose operational provisions took effect January 1, 2026, excludes drugs. Its 72-hour expedited and 7-day standard decision timeframes do not apply to pharmacy benefit prescription claims. A separate proposed rule would extend similar requirements to drugs but has not been finalized.

You may have read that new rules in 2026 force insurers to decide prior authorizations in 72 hours or 7 days. They do. Just not for your patch.

CMS’s own fact sheet is explicit: the rule requires impacted payers to send decisions within 72 hours for expedited and seven calendar days for standard requests — and then states plainly that the provision does not apply to prior authorization decisions for drugs.

Your patch is governed by:

- Medicare Part D → 42 CFR Part 423

- Employer coverage → ERISA claims rules (29 CFR 2560.503-1)

- Marketplace / individual → ACA rules (45 CFR 147.136)

What if I need a prescriber who’ll actually fight this?

Telehealth providers differ in whether they bill insurance and whether they assist with medication prior authorization. Providers operating on a cash-pay model generally do not interact with a patient’s pharmacy benefit. Whether a provider is in-network with a specific plan and whether it assists with prior authorization are two separate questions to confirm before booking.

Sometimes the honest answer is that your current prescriber isn’t going to do this. Not out of malice — out of capacity. If you’ve called three times and gotten nowhere, here’s the landscape. Including the parts that don’t flatter anyone.

Midi Health is not covered by Medicare or any Medicare-related insurance plan. And Midi cannot treat Medicaid or Medi-Cal patients at all — not even self-pay. Both statements are from Midi’s own website, not our interpretation.

So if you’re on Medicare, Medicare Advantage, Part D, or Medicaid and your goal is coverage, Midi is not your answer, and we’re not going to pretend otherwise to earn a commission. → Go to our HRT insurance coverage guide

Midi states it’s in-network with most PPO plans. If you have an HMO or EPO, verify before you book, not after.

Midi is built around billing commercial insurance. That’s the whole business model. A company that bills insurance has to live inside formularies, tiers, quantity edits, and prior authorizations — because that’s how it gets paid. Compare that to a cash-pay telehealth brand: it never touches your pharmacy benefit. It never sees a formulary. It has no structural reason to build a team that handles pharmacy benefit paperwork, and generally hasn’t.

What we verified about Midi

| Claim | Status |

|---|---|

| In-network with most PPO plans | Stated by Midi ✅ Provider-stated |

| All 50 states | Stated by Midi ✅ Provider-stated |

| Prescribes FDA-approved HRT (patches, pills, rings, gels, creams) | Stated by Midi ✅ Provider-stated |

| Prior authorization function referenced | On Midi’s own reviews page — provider-published ⚠ Testimonial, not independent |

| Not covered by Medicare; beneficiaries self-pay only, no claims | Stated by Midi ✅ Provider-stated |

| Cannot treat Medicaid / Medi-Cal | Stated by Midi ✅ Provider-stated |

| Reported communication slowdowns during the patch shortage | Acknowledged by Midi on its own reviews page ⚠ Provider-acknowledged |

| Visit cost | ⚠ Confirm at booking — we don’t publish numbers we can’t trace to a dated source |

- “Are you in-network with my specific plan?”

- “Do you assist with medication prior authorizations, or only write the prescription?”

Those are different questions. A yes to the first is not a yes to the second. Get both in writing.

Commercial PPO, prescriber who won’t file, and you’ve been waiting long enough.

Midi is built around billing commercial insurance. Formularies, tiers, and prior authorizations are their operating environment, not someone else’s department.

Takes about a minute to find out if they’re in-network with your plan.

Affiliate link. We may earn a commission, at no cost to you. The Medicare/Medicaid limits above didn’t change because of it.

About the other options — honestly

Sesame is a cash-pay marketplace with visits starting around $34. A prescription written there still runs through your own pharmacy benefit. But Sesame’s own site says its clinicians assist with insurance prior authorization specifically for patients who book a weight management service.So we can’t tell you Sesame will handle your estradiol patch prior authorization. If you need a prescriber quickly and will drive the paperwork yourself, it’s a real option. For prior authorization help specifically, it isn’t the tool.

Winona, Hers, and Inner Balanceare cash-pay. Winona’s materials describe providing documentation you may use to seek reimbursement rather than billing your plan directly. None of them solve an insurance problem, because none of them are in your insurance.

What we actually verified

This page is editorial research produced by The HRT Index Editorial Team. Payer rules, regulatory deadlines, and prices cited are traced to dated primary sources. It has not been reviewed by a clinician. Items that could not be confirmed from a primary source are identified below.

| What | Source | Checked | Status |

|---|---|---|---|

| Quantity limits, accumulator, overrides | Cigna national formulary coverage policy (reviewed 01/05/2026) | Jul 2026 | ✅ Verified |

| Step therapy criterion, 28-day generic trial, 12-month approval | Western Health Advantage GL-448214 (effective 01/01/2026) | Jul 2026 | ✅ Verified |

| Preferred status for patches; Menostar and Climara Pro non-preferred | Oregon Health Plan PDL | Jul 2026 | ✅ Verified |

| Part D deadlines, supporting statement clock, 14-day backstop | 42 CFR 423.568 | Jul 2026 | ✅ Verified |

| Part D 65-day appeal window | Medicare.gov | Jul 2026 | ✅ Verified |

| Transition process requirement | 42 CFR 423.120(b)(3) | Jul 2026 | ✅ Verified |

| Group health / ACA deadlines, urgency deferral, deemed exhaustion | 29 CFR 2560.503-1; 45 CFR 147.136 | Jul 2026 | ✅ Verified |

| External review cost, timing, 4-month window, FERP outage | HealthCare.gov | Jul 2026 | ✅ Verified |

| Boxed warning removal initiated | FDA press release, 11/10/2025 | Jul 2026 | ✅ Verified |

| Six product labels approved; 29 companies submitted | FDA press release, 02/12/2026 | Jul 2026 | ✅ Verified |

| CMS-0057-F excludes drugs | CMS fact sheet | Jul 2026 | ✅ Verified |

| Patch shortage listings (FDA has not listed) | ASHP | Jul 2026 | ✅ Verified |

| Dotti and Lyllana are ANDA-approved generics | FDA product data | Jul 2026 | ✅ Verified |

| Cash prices | Drugs.com, GoodRx | Jul 2026 | ⚠ Volatile — re-checked monthly |

| Midi insurance / Medicare / Medicaid policy | Midi’s own site | Jul 2026 | ✅ Provider-stated |

| Sesame PA scope limited to weight management | Sesame’s own site | Jul 2026 | ✅ Provider-stated |

What we could not verify:

Alora’s current U.S. marketing status. Cigna’s policy calls it obsolete; Western Health Advantage still targets it. We report the conflict, not a conclusion.

Whether Midi will file a prior authorization for your specific plan and drug. We have Midi’s insurance statements and a testimonial Midi published itself. That’s not the same as a documented workflow. Ask them directly before you book.

Estradiol-patch-specific criteria for several other major national insurers. We couldn’t find current public product-level criteria for all of them. We’re not going to guess and dress it up as data. Call and ask for it in writing.

Found an error? Email corrections@thehrtindex.com— we’ll fix it and log it.

Frequently asked questions

Does generic estradiol patch require prior authorization?

It depends on the plan. Oregon’s Medicaid preferred drug list shows generic once-weekly and twice-weekly estradiol patches as preferred with no criteria attached. Cigna’s national policy applies quantity limits rather than clinical prior authorization. Some plans require approval for all patches. Check your formulary for a “PA,” “ST,” or “QL” flag next to estradiol transdermal.

Why would my insurance cover a pill but not a patch?

Usually cost. Oral estradiol is generally less expensive than patches, and some plans use step therapy to require the lower-cost option first. Oral and transdermal estrogen aren’t clinically interchangeable — they’re metabolized differently, which affects the risk profile. That’s a conversation for your prescriber, not a swap to make on your own to save money.

Can I submit the prior authorization myself?

Usually not the clinical part — plans require the prescriber’s submission and supporting statement. But you can do a lot: get the rejection code, get the criterion in writing, confirm the supporting statement arrived, track the deadline, and file appeals. Under Medicare Part D rules, you, your prescriber, or an appointed representative can request a coverage determination.

Does prior authorization mean my patch is unsafe?

No. Prior authorization is a payment rule, not a medical opinion about you. Many estradiol patch rejections are quantity limits or refill timing edits where nobody reviewed your health at all. On February 12, 2026, the FDA approved labeling changes removing cardiovascular disease, breast cancer, and probable dementia risk statements from the boxed warning on six menopausal hormone therapy products.

How long does an approval last?

It varies. Western Health Advantage’s FEHB criteria specify 12 months for brand estradiol patches. Cigna’s policy states approvals run one year unless otherwise noted, with “one-time” overrides lasting 30 days. Ask for your approval end date in writing so you’re not ambushed at renewal.

My pharmacy gave me a different brand and now it’s rejected. Why?

One likely cause is a combined quantity limit. Cigna’s published policy states the quantity limit accumulates across weekly and semiweekly patches, so a mid-month brand swap can stack two products against one cap. Get the rejection code to confirm, then ask your prescriber to request a one-time quantity override.

Does Medicare Part D cover estradiol patches?

Coverage varies by plan formulary. If yours applies prior authorization or step therapy, federal regulation requires your plan to maintain a transition process providing a temporary supply within the first 90 days of coverage under a new plan. Many plan transition policies extend this to quantity limits and to formulary changes across plan years. Ask at the counter: “Is this eligible for a transition fill?”

Does TRICARE require prior authorization for estradiol patches?

A TRICARE contractor prior authorization form for estradiol we reviewed directs that if the patient’s sex is female, prior authorization is not required. That form is undated in its body text and reflects one contractor’s process, so confirm with your TRICARE pharmacy contractor before relying on it. If you’re on TRICARE and were told you need a PA, it’s worth asking directly.

What’s the difference between a formulary exception and a tiering exception?

A formulary exception asks your plan to cover a drug that isn’t on its approved list. A tiering exception asks your plan to charge you a lower tier’s price for a drug that is covered. Different requests, different forms. Using the wrong term can route your request to the wrong queue.

Can my doctor request an expedited review?

Yes — and it’s the most underused right you have. Under 45 CFR 147.136, whether a claim involves urgent care is determined by the attending provider, and the plan must defer to that determination. That can move a group health pre-service claim from 15 days to 72 hours. Your prescriber makes that call based on your actual situation.

How long do I have to appeal a Medicare Part D denial?

You, your representative, or your prescriber must request an appeal within 65 days from the date on the initial denial notice, per Medicare.gov. Medicare extended this from 60 days. If you miss it, you can still file if you give a reason. Note it runs from the date on the notice, not the day you received it.

What if it’s denied?

First determine whether it’s a substantive denial or a fixable error — wrong NDC, wrong day supply, missing document. Fix errors; appeal denials. You generally have 65 days on Part D and at least 180 days on group health plans, plus 4 months to request external review from your denial notice.

How much does an estradiol patch cost without insurance?

Published pricing lists generic patches starting around $35.83 for eight twice-weekly 0.025mg patches and about $56.38 for four weekly 0.05mg patches, per Drugs.com. GoodRx lists the twice-weekly 0.05mg 8-patch supply around $36.23 with a coupon against an average retail of about $104.43. Prices vary by pharmacy and change frequently. Checked July 2026.

Do the new 2026 prior authorization rules apply to my patch?

No. CMS-0057-F’s 72-hour and 7-day timelines took effect January 1, 2026 but exclude drugs. Your patch runs on Part D rules or ERISA/ACA rules instead. A proposed rule (CMS-0062-P) would extend the requirements to drugs, but it hasn’t been finalized.

Can I use a GoodRx coupon and my insurance together?

No. It’s one or the other on any given fill. Sometimes the coupon beats your copay — especially on a high-deductible plan or a high tier. Ask the pharmacist to run it both ways. But cash isn’t automatically credited toward your deductible.

One last thing

If you got here from a pharmacy counter, we’re sorry. That’s a genuinely awful way to spend an afternoon, and being told no in front of a line of strangers — about a medication you already have a prescription for — is a special kind of insult.

But now you know what most women never find out: it’s often not a doctor saying no. It’s a running total hitting a ceiling. And running totals have overrides.

You know which of eight things might have happened, and how to find out which. You know the words. You know your deadline and the regulation behind it. You know your prescriber — not your insurer — decides if it’s urgent. And you know that if all of it falls apart, published cash prices for the generic patch start around thirty-six dollars.

You’re allowed to want this. You’re allowed to be annoyed. And you’re allowed to make the call and be specific about what you need. Go make the call.

Still not sure your current care setup is right?

Fighting your insurer for a patch is one problem. Whether you’re in the right care model — for your symptoms, your insurance, your state, and whether online care is even the right starting point for you — is a different one. A pharmacy counter can’t answer that.

Get your personalized HRT action plan

Free · No account needed · It’ll also tell you when online care isn’t where you should start.

Find My HRT Path →Takes about 90 seconds

Related: Estradiol patch shortage 2026 · Estradiol patch guide · HRT insurance coverage · HRT costs 2026 · FDA-approved vs. compounded HRT · Does insurance cover estradiol patch?

Sources

- 42 CFR 423.568 — Medicare Part D exception timeframes and supporting-statement clock

- 42 CFR 423.120(b)(3) — Medicare Part D transition process requirement

- 45 CFR 147.136 — Group health and Marketplace plan deadlines, urgency deferral, deemed exhaustion, external review

- 29 CFR 2560.503-1 — ERISA claims and appeals procedures

- Medicare.gov — appeals in a drug plan — 65-day appeal window

- HealthCare.gov — external review — cost, timing, 4-month window, FERP outage notice

- Cigna National Formulary Coverage Policy — Estrogens (Topical), Patches — quantity limits, accumulator, overrides. Reviewed 01/05/2026.

- Western Health Advantage GL-448214 — step therapy criterion, effective 01/01/2026

- Oregon Health Plan PDL — Estrogen Replacement, Topical — preferred status, checked July 2026

- FDA — boxed warning removal announcement, Nov 10, 2025

- FDA — six product label changes approved, Feb 12, 2026

- CMS — CMS-0057-F fact sheet — drugs excluded from 72-hour / 7-day timelines

- Drugs.com price guide and GoodRx — cash prices, checked July 2026

- ASHP drug shortage bulletin — estradiol transdermal patches listed (Amneal, Noven, Sandoz, Zydus)

The HRT Index is the independent decision resource for online menopause and HRT care. Educational content only — not medical advice, not insurance advice, not legal advice. FDA-approved and compounded options are labeled distinctly throughout; compounded medications are not FDA-approved. Your member plan documents, your pharmacy claim, and your written denial control your actual coverage. Last verified July 2026.