Usually — but “covered” and “filled” are two different words, and nobody explains the gap.

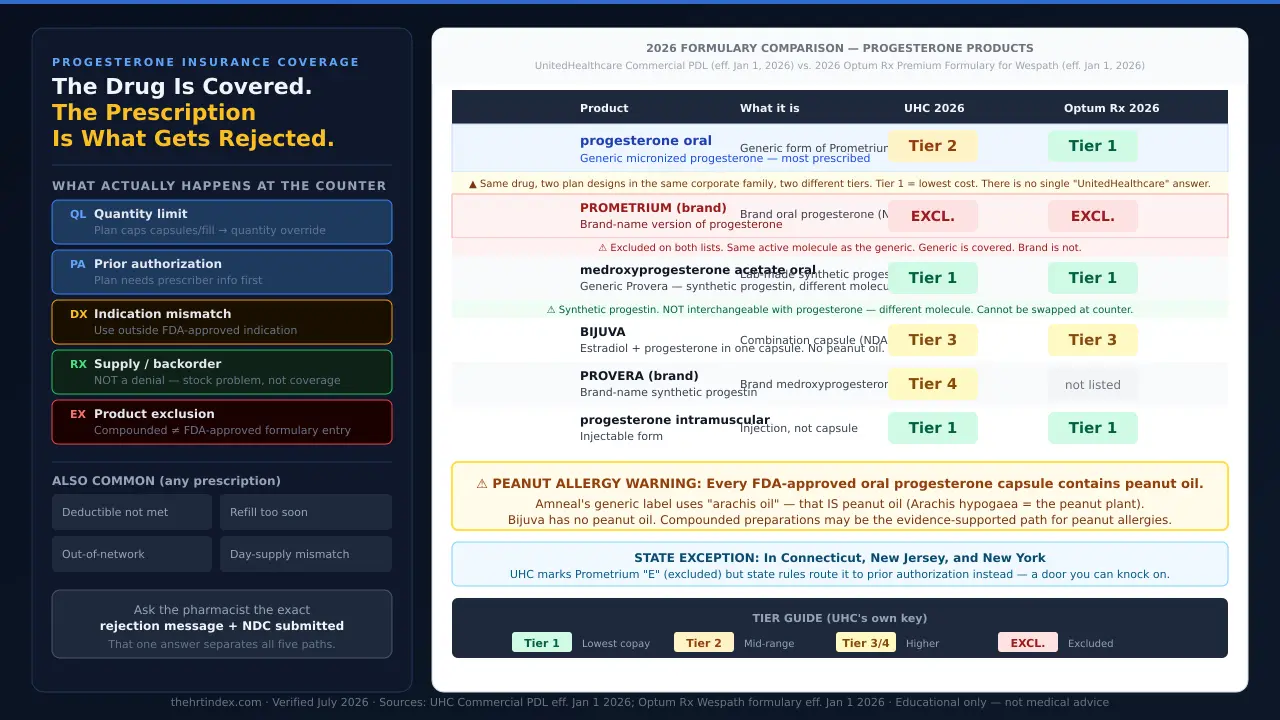

Generic oral progesterone is on the drug lists of major plans. We read two 2026 formularies line by line: it sits at Tier 1 on one and Tier 2 on the other. So if you’re asking whether insurance covers progesterone for menopause, the drug itself is rarely the problem.

Your specific prescription might be.

Insurance covers the drug. What gets rejected at the counter is the prescription— a particular brand, a particular number of capsules, a particular reason for taking it. And in 2026, sometimes nothing was rejected at all and the pharmacy simply doesn’t have it.

This page is for you if:you have a progesterone prescription that cost more than expected, got partly filled, or got rejected — or you’re about to fill one and want to know what’s coming.

This page is not for you if:you’re deciding whether to take progesterone at all, or comparing prices. Different questions, different pages.

Does insurance cover progesterone for menopause?

Usually, in some form. Generic oral micronized progesterone appeared on both 2026 US formularies reviewed for this page, at Tier 1 on one and Tier 2 on the other. Brand-name Prometrium was marked excluded on both. A formulary listing does not guarantee that a given prescription will be paid: tier, quantity limits, prior authorization, diagnosis rules, deductibles, and product availability all determine what actually happens at the counter.

The drug is covered. The prescription is what gets rejected.

Those are two different things, and almost nobody tells you that.

“Covered” means the drug is on the list. That’s it. A formulary — the list of drugs your plan agrees to pay for — isn’t a promise. It’s an entry. And that entry carries fine print: which tier, how many capsules, whether your prescriber needs permission first, which pharmacy, and whether your deductible is paid off yet.

What we found on two 2026 formularies

We didn’t call an insurance company. We opened two published 2026 drug lists and read the progesterone rows ourselves.

| Product | What it is | UnitedHealthcare 2026 Commercial PDL eff. Jan 1, 2026 | 2026 Optum Rx Premium Formulary (Wespath) eff. Jan 1, 2026 |

|---|---|---|---|

| progesterone oral | Generic micronized progesterone — the one most women are handed | Tier 2 | Tier 1 |

| PROMETRIUM | Brand-name version of the same hormone | E — Excluded | E — Excluded |

| medroxyprogesterone acetate oral | Generic Provera — a synthetic progestin, a different molecule | Tier 1 | Tier 1 |

| BIJUVA | Estradiol + progesterone in one capsule. No peanut oil. | Tier 3 | Tier 3 |

| PROVERA | Brand-name synthetic progestin | Tier 4 | not listed |

| progesterone intramuscular | The injection | Tier 1 | Tier 1 |

| Tier 1 = lowest-cost tier; Tier 2 = mid-range, per UnitedHealthcare’s own key. Sources: UHC 2026 Commercial PDL eff. Jan 1, 2026; Optum Rx Wespath Premium Formulary eff. Jan 1, 2026. Educational only — check your specific plan. | |||

Three things in that table are worth stopping on.

1. The synthetic sits below the body-identical one. On UnitedHealthcare’s 2026 commercial list, medroxyprogesterone acetate — generic Provera, a lab-made progestin — is Tier 1. Progesterone, the molecule your ovaries used to make, is Tier 2. One tier up. So when your doctor’s office mentions that your insurance “would rather” you take Provera, that isn’t a hunch. It’s printed.

2. Two formulary designs in the same corporate family don’t match. UnitedHealth Group owns both UnitedHealthcare and Optum Rx. Same effective date, same drug: Tier 2 on one design, Tier 1on the other. There is no such thing as “what UnitedHealthcare covers.” There’s only what your plan design covers.

3. Your state can change what “excluded” means. UnitedHealthcare marks Prometrium with an E. In small print: drugs listed as E are subject to prior authorization in Connecticut, New Jersey, and New York. Same insurer, same brand, same year — in most states that E means excluded; in those three, it points at a prior authorization instead.

What this proves

Two women who describe their insurance the same way can get two different answers for the same capsule — and it has nothing to do with them, their symptoms, or how bad their hot flashes are.

What this does not prove: Two formularies is two formularies. It is not a national coverage rate. Your employer buys a specific plan design. Yours may differ.

NOT SURE WHERE TO START?

The right answer depends on your situation.

The HRT Index’s Find My HRT Path tool matches your situation to the right provider — comparing telehealth options on clinical legitimacy, care quality, medication fit, and price transparency, so you can choose before your first consult.

Take the free matching quiz →Before we go further

Most women reading this page don’t need us. They need one phone call.

If your progesterone got rejected, there’s a real chance it’s a quantity limit or a supply gap — and both are things your pharmacist and prescriber can often sort out directly, using words we’re about to hand you. If that works, close this tab.

We do earn a commission if you later book with a provider through our links. That’s exactly why we’re telling you to try the free route first. If we only made money when you needed us, you couldn’t trust the rest of this page. See our affiliate disclosure.

What determines whether your plan pays?

Four variables drive most progesterone coverage outcomes: whether the prescription is for the brand or the generic, how many capsules are prescribed relative to the plan’s limits, whether the product is FDA-approved or compounded, and whether the patient can take the product at all. Symptom severity is not one of them — formulary tier is set by plan design, not by how a patient feels.

Brand or generic.Generic oral progesterone was covered on both 2026 lists we read. Brand-name Prometrium was marked excluded on both. If you’re staring at a rejection on Prometrium specifically, this is the first thing to check.

How many capsules. The FDA-approved dose for protecting the lining of the uterus is 200 mg for 12 days out of every 28-day cycle— twelve capsules per cycle. Many menopause clinicians now write one capsule daily, which is thirty a month. Those numbers don’t match, and some plans build limits from the label’s number. More on that below →

FDA-approved or compounded. Compounded progesterone is a separate category with separate rules and it is not automatically covered. More on that below →

Whether you can take it.Every FDA-approved oral progesterone capsule we read — brand and generic — contains peanut oiland is contraindicated in peanut allergy on its own label. If that’s you, the covered option isn’t an option, and your whole strategy changes. Jump to that →

Why was my progesterone rejected if it’s covered?

A progesterone rejection at the pharmacy is not a single event. Common causes include quantity limits, prior authorization requirements, a diagnosis outside the FDA-approved indication, a supply shortage, a product exclusion such as compounded preparations, an unmet deductible, a refill requested too soon, an out-of-network pharmacy, or a day-supply mismatch. Some of these are not coverage denials at all — a backorder is a stock problem, and an unmet deductible means the plan is paying, just not yet.

The five progesterone-specific paths

| Label | What the counter says | What’s happening | Where the fix lives |

|---|---|---|---|

| Quantity limit | “We can only fill 12.” / “Exceeds plan limit.” | The plan caps capsules per fill or per period. | Prescriber requests a quantity-limit exception— a different request from a prior authorization |

| Prior authorization | “It needs prior authorization.” | The plan wants information from your prescriber before it pays. Prometrium is excluded while generic progesterone isn’t — worth asking which product was submitted. | Prescriber submits the PA, or you discuss whether the generic fits you |

| Indication mismatch | “Not covered for this diagnosis.” | The prescribed use sits outside the narrow FDA-approved indication. | Medical-necessity documentation from your prescriber. A real conversation — not a coding trick |

| Supply / backorder | “Backordered.” / “Only have 15.” / “Try next week.” | Not a coverage decision. Progesterone capsules are on the shortage list. | Different manufacturer, different pharmacy, or mail order |

| Product exclusion | “Compounded isn’t covered.” | Compounded preparations are not FDA-approved products and are handled separately from the generic on the formulary. | Depends on your plan and your situation — see compounded section below |

The four that hit any prescription

Before you assume this is about progesterone, rule these out:

- Your deductible isn’t met. The plan iscovering the drug — you’re just paying the negotiated price until you hit your deductible. Especially likely in January.

- Refill too soon.You’re a few days early. That’s it.

- Out-of-network pharmacy. Your plan may only pay at certain pharmacies, or may price mail order differently.

- Day-supply mismatch.The prescription is written for a quantity your benefit doesn’t pay for in one fill.

The most useful question you can ask isn’t “is it covered.” It’s: “What’s the rejection message?”

The pharmacy sees the actual reason before anyone else does. That one answer separates all five paths above.

How do I check whether my exact prescription is covered — before I go to the pharmacy?

Coverage can be verified before a prescription is filled. The check requires four specifics: the product’s National Drug Code, the strength, the quantity, and the day supply. A general question about “progesterone” can return a different answer than a question about the exact product a prescriber sent to the pharmacy.

Ten minutes here saves a bad afternoon later.

What to have in front of you

- Your insurance card— the member services number is on the back.

- The NDC(National Drug Code) — the number that identifies the exact product. Your pharmacy can read it to you in seconds. Ask for it. “Progesterone” isn’t a question a formulary can answer. An NDC is.

- Strength— 100 mg or 200 mg.

- Quantity and day supply— how many capsules, over how many days.

The script — use these exact words

Say this to your plan’s member services line:

“I’m checking coverage for progesterone oral capsules, [strength], NDC [number], quantity [number], for a [number]-day supply.

Is that exact NDC on my current formulary, and what tier?

Is there a quantity limit, and what is it?

Does it require prior authorization or step therapy?

Have I met my deductible, and does it apply to this tier?

If it’s excluded, which progesterone products are covered — and what’s the exception process?

Please send me the coverage criteria in writing.”

That last line is the one nobody asks, and it’s the one that matters. A written criteria document is what your prescriber’s office needs to write a request that actually gets approved. Without it, they’re aiming at a target they can’t see.

Then write down the date, the representative’s name, and the call reference number. Every single time. If this goes sideways later, that log is your evidence.

And ask your prescriber’s office one question: “If this gets rejected, who in your office handles prior authorizations and exceptions?” Some practices have a dedicated person. Knowing which kind you have — before you need it — tells you a lot.

Why did they only give me 12 pills?

The FDA-approved dose of Prometrium and generic micronized progesterone for prevention of endometrial hyperplasia is 200 mg at bedtime for 12 days sequentially per 28-day cycle — twelve capsules per cycle. Many clinicians prescribe 100 mg daily on a continuous schedule, which is thirty capsules per month. Some plans build quantity limits from the label’s number. A short fill can also reflect a partial fill during a supply shortage or a day-supply mismatch.

Reason one: the label and modern practice disagree

We read the current Prometrium prescribing information — revision 02/2026, live on DailyMed today. Under Dosage and Administration, for prevention of endometrial hyperplasia, it says the capsules should be given as a single daily dose at bedtime, 200 mg orally for 12 days sequentially per 28-day cycle. Twelve capsules per cycle.

Now here’s how your prescription was probably written: 100 mg, one capsule, every night.Thirty a month, taken continuously — fewer withdrawal bleeds, steadier routine, the way menopause medicine is largely practiced now.

Twelve versus thirty. Nobody’s wrong. But the numbers don’t match, and a claims system only knows one of them.

The honest part: neither of the two 2026 lists we read flags a quantity limit on progesterone oral. No QL notation on either one. So a quantity limit is not universal — it’s specific to plan design. If you’re being told “we can only fill 12,” that may well be what’s happening — but we’re not going to tell you every plan does this when the two documents we opened say otherwise.

Reason two: it’s a partial fill

The pharmacy had fifteen and gave you fifteen. That’s a stock event, not a coverage event, and it looks identical from where you’re standing. More below →

Reason three: day supply

Your benefit pays for a certain number of days per fill, and the prescription was written for a different number.

How to tell which one you’re in

Ask the pharmacist: “Is this a plan quantity limit, or do you just not have the rest?”

That one question separates reason one from reason two, and they have completely different fixes. If it’s a quantity limit, ask your prescriber for a quantity-limit exception— that’s a different request from a prior authorization, with different criteria. Asking for the wrong one costs you time.

Why does my plan want me on Provera instead?

Progesterone and progestins are different molecules. Micronized progesterone is structurally identical to the hormone the ovaries produce. Medroxyprogesterone acetate — generic Provera — is a synthetic progestin with a different chemical structure. On UnitedHealthcare’s 2026 commercial drug list, medroxyprogesterone acetate is Tier 1 while oral progesterone is Tier 2. A pharmacist cannot substitute one for the other; that requires a new prescription.

Your plan isn’t making a medical argument. It’s making a purchasing decision — and that purchasing decision leaks into your appointment as a suggestion.

What can and can’t be swapped at the counter

- Generic progesterone for Prometrium? Generally yes. FDA rates them therapeutically equivalent, and pharmacists can typically substitute unless the prescriber specified brand only. Substitution rules are set by state law. If you’re facing a rejection on brand Prometrium, ask whether the generic was tried — on both lists we read, the generic is covered and the brand isn’t.

- Provera for progesterone? No. Different molecule, different drug. That requires your prescriber to write a new prescription.

That said — if progesterone is genuinely unavailable, medroxyprogesterone is a long-established option for endometrial protection during estrogen therapy. Worth raising with your prescriber rather than fearing. Bring it as a question, not a concession.

The peanut oil problem: when the covered option isn’t an option for you

Every FDA-approved oral micronized progesterone capsule reviewed for this page — brand Prometrium and the generics — contains peanut oil and is contraindicated in patients allergic to peanuts, per the products’ own FDA labeling. Some generic labels list the ingredient as “arachis oil,” which is peanut oil under its botanical name. Bijuva, the FDA-approved estradiol-plus-progesterone capsule, does not list peanut oil or arachis oil among its inactive ingredients.

| Product | Peanut oil? | Word the label uses | Contraindicated in peanut allergy? |

|---|---|---|---|

| Prometrium (brand, rev. 02/2026) | Yes | “peanut oil NF” | Yes. Label reads: DO NOT USE IF ALLERGIC TO PEANUTS |

| Generic progesterone — Amneal (rev. 02-2026-03) | Yes | “arachis oil”— same substance, different word | Yes, per label |

| Generic progesterone — other labels reviewed | Yes | “peanut oil NF” | Yes, per label |

| BIJUVA (estradiol + progesterone) | No | Gelatin, glycerin, lecithin, medium-chain triglycerides — no peanut oil, no arachis oil | No peanut-oil contraindication |

⚠ “Arachis oil” is peanut oil

Arachis hypogaea is the peanut plant. Arachis oil is peanut oil. Two labels for the same generic drug use two different words for it. A woman with a peanut allergy reads the ingredient list looking for the word peanut — and doesn’t find it. You need to look for both words.

There is no generic escape

Every FDA-approved oral progesterone capsule label we read contains peanut oil, whichever word it uses. We read the labels we could find. If a peanut-oil-free oral progesterone capsule exists in the US, we didn’t find it.

This is the strongest exception argument that exists

“The preferred alternative is contraindicated for this patient on its own FDA-approved label.”

That’s not a preference. That’s a labeled contraindication, printed by the manufacturer, approved by the FDA, and stamped on the bottle in capital letters. In a system built to say no, that’s about as clean and documentable as it gets.

And this is the one place where compounded is the evidence-supported answer

We spend this entire site saying FDA-approved first. Here’s where that doesn’t apply, and we’re going to say so plainly.

In July 2020, the National Academies of Sciences, Engineering, and Medicine published The Clinical Utility of Compounded Bioidentical Hormone Therapy — a report the FDA itself commissioned. It concluded there is insufficient evidence to support the clinical utility of compounded bioidentical hormone therapy, and recommended that prescribers restrict its use to two circumstances: when a patient is allergic to an ingredient in an FDA-approved hormone product, and when a patient requires a dosage form not available as an FDA-approved product.

Peanut allergy is the first one on that list.

Not because compounded is better. Not because it’s more natural. Not because it’s equivalent to an FDA-approved product; it isn’t. But because the National Academies, in a report the FDA paid for, named your exact situation as one of two where it belongs.

Also worth raising with your prescriber:Bijuva is an FDA-approved oral capsule with no peanut oil. But read this carefully — it is not a straight swap. It’s a different product with a different FDA-approved use (moderate to severe hot flashes in a woman with a uterus), and it contains the estrogen too, so it only makes sense if the estrogen fits your plan as well. It’s a conversation, not a substitution.

⚠ Take this language to your prescriber:

“The preferred oral progesterone contains peanut oil and is contraindicated in peanut allergy on its own FDA label. I need a formulary exception on those grounds.” Your prescriber can use the exact FDA label language and the National Academies report citation in the exception request.

My pharmacy says it’s backordered. Am I denied?

No. A backorder is not a coverage decision. Progesterone capsules appear on the American Society of Health-System Pharmacists drug shortage database. As of that entry’s June 30, 2026 update, Hikma reported 100 mg and 200 mg capsules on back order with an estimated release of early July 2026, and Amneal reported 100 mg capsules on back order with no estimated release date. A partial fill or a “come back next week” means the pharmacy has no stock — it says nothing about what your plan would pay.

⚠ A partial fill and a denial look identical from where you’re standing.

If you pay cash for a compounded preparation because a pharmacist said “we only have fifteen,” you may have just bought a solution to a problem you didn’t have. Whether your plan would have paid is a separate question — and it’s one you can get answered in one phone call.

What’s actually going on in 2026

- Last fall, the FDA moved to remove a 20-year-old boxed warning that had discouraged women from taking hormone therapy. Updated labeling was approved for the first group of products in February 2026— a rolling process, not a single switch.

- Estrogen patch prescriptions are up 162% over two years, more than doubling to roughly 1.6 million in May 2026. All estrogen prescriptions together are up 78% over two years.

- Three types of estradiol patch went into shortage. ASHP has since listed several estradiol creams and progesterone capsules in shortage too.

What we can say: demand rose sharply, and progesterone capsules are now on the shortage list. What we won’t say is that we’ve proven one caused the other. Nobody has published that.

Why your pharmacist says “shortage” and the FDA’s site doesn’t

ASHP’s shortage database is built from public reports — pharmacists, providers, people who can’t get the drug. The FDA’s list comes from manufacturers. Two different inputs. Two different answers. A shortage can be real on the ground and invisible on the spreadsheet. You’re not imagining it.

This matters practically: some legal permissions for compounding pharmacies key to the FDA’sshortage list, not ASHP’s. If someone tells you compounding is allowed “because of the shortage,” ask which list they mean.

What to actually do

- Ask for a different manufacturer.Availability differs by manufacturer and by week — the shortage entry names Amneal, Virtus, Hikma, and Xiromed at various statuses. Your pharmacist can check what’s in the system.

- Try an independent pharmacy. Different wholesaler, different allocation. Chain locations often draw from the same warehouse.

- Ask about 90-day mail order. Different supply channel entirely.

- Take the partial fill and ask them to hold the balance so you don’t lose the rest of the prescription.

- Don’t pay cash for a compounded preparation to solve a stock problem without first checking what your plan would cover next week.

Check the live ASHP entry before you act on any of this.Shortage status changes weekly, and the estimates in it are manufacturer estimates, not promises. The early-July date above is what the June 30 entry said — that window has now passed, which is exactly why you should look at today’s version rather than trust ours.

What does progesterone cost with and without insurance?

Cost depends on the product and the plan. Generic oral micronized progesterone is generally inexpensive relative to brand-name menopause medications, and on the two 2026 formularies reviewed here it carried the lowest or second-lowest cost-sharing tier. Brand-name Prometrium was marked excluded on both, which means a patient may be responsible for the full cost unless an exception is approved. Discount-card cash prices and insurance copays are set independently and either can be lower.

Your copay is sometimes higher than the cash price. This happens with cheap generics all the time. Ask the pharmacist for both numbers. Not one. Both.

But know the trade-off.Money you spend using a discount card usually isn’t automatically credited toward your deductible or your out-of-pocket maximum, because it isn’t going through your plan as a claim. Save the receipt and ask your plan whether it can be applied. Cheaper today can mean more expensive by December if you’re someone who hits your maximum.

📅 July 1 formulary changes — worth asking about by name

The Optum Rx 2026 formulary states that medications may move to a higher tier or be excluded from coverage on January 1 or July 1 of each year. If your progesterone was fine in June and rejected this month, you may not have done anything at all. Ask your plan directly: “Did my formulary change on July 1?”

For a full breakdown of progesterone prices across providers, see our HRT cost page. We keep this section short on purpose — we’d rather send you there than print a number we can’t stand behind.

Does Medicare cover progesterone for menopause?

Prescription drug coverage under Medicare comes through a Part D plan or a Medicare Advantage plan that includes drug coverage — not through Part A or Part B. Each Part D plan publishes its own formulary, so progesterone coverage and tier must be checked against that specific plan. In 2026, no Medicare drug plan may charge a deductible above $615, and once out-of-pocket spending on covered Part D drugs reaches $2,100, the plan pays 100% of covered drugs for the rest of the calendar year.

The 2026 numbers, from Medicare.gov:

| 2026 Medicare Part D Figures | Amount |

|---|---|

| Maximum deductible any Part D plan may charge | $615 |

| Out-of-pocket cap on covered Part D drugs | $2,100 |

| What you pay after you hit the cap | $0, rest of the calendar year |

| Coinsurance in the initial coverage stage | 25% |

Important: the tiers in our main table are from commercial drug lists, not Part D plans.

Part D plans build their own formularies. Don’t assume your Part D plan tiers progesterone the way a commercial plan does. Look it up on your plan’s own drug list, or call the number on your card.

Why your cheap generic cost full price in January

Because plans now carry more cost at the top end, many have responded by charging the maximum allowed deductible and applying it across all drug tiers. A low-tier generic that used to be a few dollars can cost you the negotiated price until you’ve worked through $615. Nothing changed about your drug. The plan design changed around it.

Two Medicare-specific traps

- Discount cards don’t count.Money you spend through a discount program doesn’t apply toward your $2,100 cap, because it isn’t a claim through your plan.

- Copay cards are off the table. Federal rules bar manufacturer copay cards for Part D patients. Manufacturer patient assistance programs are a different thing, and Medicare patients often can use those. Worth asking about.

The reason to actually appeal

If a drug isn’t covered by your plan, what you pay for it doesn’t count toward your $2,100 cap. No cap, no ceiling, no relief. That’s the difference between a bad year and a capped year — and it’s the strongest practical argument for using the exception process rather than quietly paying cash. The Part D process is below →

Also worth asking about: Part D plans commonly provide a one-time temporary supply of a drug in certain situations while you sort out a formulary problem. Ask your plan directly: “Am I eligible for a transition supply while we file this?”

⚠ Provider note — Midi Health and Medicare

Midi Health states it is not covered by Medicare or any Medicare-related plan. It can accept Medicare beneficiaries as self-paypatients, but no claims related to visits, medications, or associated services can be submitted. If you’re on Medicare and want to use your benefits, Midi is not the route.

Does Marketplace or ACA insurance cover progesterone?

Marketplace plans include prescription drugs as an essential health benefit, so each plan must have a formulary. The specific tier, quantity limits, and prior authorization rules vary by plan and by state. Marketplace plans follow the federal internal appeal and external review timelines, which differ from Medicare Part D deadlines. Every Marketplace plan publishes a formulary and a Summary of Benefits and Coverage, both of which can be reviewed before a prescription is filled.

Prescription drug coverage isn’t optional on Marketplace plans — it’s one of the essential health benefits every plan must include. But “included” doesn’t tell you the tier, the limits, or the deductible.

Two documents answer almost everything:

- The plan’s formulary— the drug list. Look up progesterone by name, then check the tier and any QL/PA notations.

- The Summary of Benefits and Coverage— the standardized document every plan must give you. This is where the deductible lives, and where you find out whether it applies to drugs at all.

Both should be linked from your plan’s page. If you can’t find them, that’s what member services is for.

One thing that catches Marketplace enrollees hard: many of these plans carry high deductibles that apply to prescriptions. Your generic can be “covered” at Tier 1 and still cost you the full negotiated price in March, because you haven’t hit your deductible. That’s not a denial. That’s the plan working as designed. Worth knowing before you start filing appeals against a problem that isn’t one.

Does Medicaid cover progesterone?

Medicaid prescription drug coverage is administered at the state level. States and their managed-care plans maintain preferred drug lists that determine which products are covered and under what conditions, so progesterone coverage depends on the state and, where applicable, the specific managed-care plan. Coverage should be checked against the applicable state preferred drug list rather than assumed from a national source.

The right question isn’t “does Medicaid cover HRT.” It’s “is progesterone on my state’s preferred drug list, and what does my managed-care plan require?” Those are lookups with real answers. Start with your state’s Medicaid preferred drug list. If you’re in a managed-care plan, check that plan’s formulary too — it may differ from the state’s.

⚠ Provider note — Midi Health and Medicaid

Midi Health states it is not enrolled with Medicaid or Medi-Cal and cannot treat Medicaid patients — even as self-pay.If you’re on Medicaid, don’t book. We’d rather lose the click than have you find out at checkout.

Employer plans, and no insurance at all

Employer-sponsored plans purchase specific formulary designs, so two people covered by the same insurance company can have different drug lists, tiers, and exclusions. Without insurance, progesterone is purchased at cash or discount-program prices, which vary by pharmacy and location.

Why your coworker pays less

Same card. Same logo. Different price. Employers buy different plan designs. Two people whose cards say “UnitedHealthcare” can have completely different drug lists — we showed you two designs in the same corporate family disagreeing on the same generic at the top of this page. Your friend’s copay tells you nothing about yours.

If your employer is self-funded, the plan design is your employer’s choice, not the insurer’s. That’s often who you’d actually be arguing with.

No insurance

If you’re uninsured, generic progesterone is one of the more affordable prescriptions in menopause care, and discount programs are the normal route. Prices vary by pharmacy and ZIP code enough that it’s worth checking two or three — including an independent pharmacy, which sometimes beats the chains.

A woman with no insurance can end up paying less for progesterone than a woman with a high-deductible plan. That’s not fair. It is, sometimes, true.

Is compounded progesterone covered by insurance?

Not automatically. Compounded preparations are not FDA-approved drug products and are handled separately from FDA-approved products on formularies. Many commercial plans exclude them. Under Medicare Part D rules, a compounded prescription may receive coverage when it contains at least one ingredient that qualifies as a Part D drug, so a blanket assumption of exclusion is not accurate for Part D. Coverage must be confirmed with the specific plan.

Why it’s treated differently — and it isn’t a conspiracy.FDA-approved products go through review for safety, effectiveness, and manufacturing quality, and they carry standardized labeling and dosing. Compounded preparations are prepared per prescription and haven’t been through that review. They’re a different regulatory category, so plans handle them under different rules.

What we will not say about compounded progesterone:

- Not an FDA-approved generic of anything

- Not therapeutically equivalent to an FDA-approved product

- Not clinically proven to the standard an FDA-approved product has met

- Not “safer than,” “more natural than,” or “the same as” FDA-approved

The two legitimate cases, per the National Academies report the FDA commissioned:

- Allergy to an ingredient in an FDA-approved product

- A dosage form that doesn’t exist as FDA-approved

⚠ One limitation we won’t soften

Absorption from transdermal progesterone cream varies between people, and the evidence for endometrial protection from creams is not equivalent to what exists for oral micronized progesterone. In Prometrium’s own pivotal trial, 358 postmenopausal women with an intact uterus were followed for up to 36 months. Among those taking conjugated estrogens 0.625 mg daily plus cyclical Prometrium 200 mg for 12 days per 28-day cycle, 6% developed endometrial hyperplasia. Among those taking the same estrogen alone, 64%did. If you have a uterus and you’re on systemic estrogen, the progestogen isn’t cosmetic. Whatever you and your prescriber decide, decide it together.

For a complete breakdown of FDA-approved vs. compounded hormone therapy, see our FDA-approved vs. compounded HRT explainer.

What do I do if my progesterone is denied?

Appeal rights and deadlines depend on the type of plan. Under Medicare Part D, a coverage determination or exception request must generally be decided within 72 hours, or 24 hours if expedited, with the clock starting when the plan receives the prescriber’s supporting statement; a first-level appeal must be filed within 65 calendar days of the denial notice. Under most employer and Marketplace plans, an internal appeal may generally be filed within 180 days of the denial notice, and an external review is generally decided within 45 days and is binding on the insurer.

Your deadlines depend on what kind of insurance you have. This is the single most common thing coverage articles get wrong, and getting it wrong can cost you your appeal.

If you have Medicare Part D or Medicare Advantage with drug coverage

| Step | The deadline | Who decides |

|---|---|---|

| Coverage determination / exception request | 72 hours standard; 24 hours expedited | Your plan |

| When does the clock start? | For an exception, when the plan receives your prescriber’s supporting statement — not when you call | — |

| File a redetermination (Level 1 appeal) | 65 calendar days from the date on the denial notice | Your plan |

| Redetermination decision | 7 calendar days standard; 72 hours expedited | Your plan |

| If the plan blows the deadline | Your case is automatically forwarded to Level 2 | — |

| Level 2 | Independent Review Entity | Outside reviewer |

⚠ 65 days, not 180

If you read somewhere that you have 180 days to appeal, that’s the commercial rule, and it does not apply to you. Miss the 65 and you need a good reason for filing late.

If you have an employer plan or a Marketplace plan

| Step | The deadline | Who decides |

|---|---|---|

| Coverage / exception request | Generally 72 hours; 24 hours expedited | Your plan |

| File an internal appeal | Generally 180 days from the denial notice | Your plan |

| Urgent internal appeal decision | Generally 72 hours | Your plan |

| External review — standard | Generally no later than 45 days | Independent reviewer |

| External review — expedited | Generally 72 hours or less | Independent reviewer |

| Is it binding? | Yes. Your insurer is required to accept it. | Independent reviewer |

Follow the instructions in your denial notice for the external review rather than any general route you read online. External review is administered differently depending on your state and your plan type, and the process has moved before. Your notice tells you the current path for your specific plan.

The four steps, in order

Get the rejection message

Not “is it covered.” “What’s the rejection message, and what’s the NDC you submitted?” The pharmacy sees the actual reason first. This one question sorts you faster than anything else on this page.

Call your plan with specifics

Use the script in the verification section above — NDC, strength, quantity, day supply. And ask for the coverage criteria in writing.

Match the request to the problem

These are different forms with different criteria. Picking the wrong one costs you the calendar:

- Quantity limit → quantity-limit exception

- Not on the formulary → formulary exception

- Covered but expensive tier → tiering exception

- Required to try something else first → step-therapy exception

- Exception denied → formal appeal, on the clock for your plan type

Ask about a peer-to-peer

Your prescriber speaks directly with the plan’s reviewing clinician. It’s two clinicians talking instead of a fax sitting in a queue. Ask your prescriber’s office whether they’ll request one.

For help with the prior authorization process specifically, see our HRT prior authorization guide.

Do telehealth menopause providers bill insurance for progesterone?

Practices differ. Midi Health states it is in-network with most PPO plans, operates in all 50 states, and lists self-pay pricing of $250 for an initial visit and $150 for follow-ups, excluding labs and medications. Winona states on its own help pages that it does not directly work with insurance companies and is not able to bill an insurance provider on a patient’s behalf. For a patient whose goal is to use insurance benefits, this distinction determines which providers are usable at all.

We fetched these pages on July 16, 2026 and recorded what each company says about itself.

| Provider | What the marketing says | What we verified on their own pages | The gap |

|---|---|---|---|

| Midi Health | “Insurance-Covered Hormone Replacement Therapy” | In-network with most PPO plans. Available in all 50 states. Self-pay: $250 initial / $150 follow-up, not including labs or medications. HSA/FSA accepted. Not covered by Medicare or any Medicare-related plan. Not enrolled with Medicaid/Medi-Cal — cannot treat Medicaid patients even as self-pay. | The headline says “insurance-covered,” full stop. The caveats are on the same page, to their credit. But “covered” is doing a lot of work if you’re on Medicare, Medicaid, or an HMO. |

| Winona | “Personalized bioidentical HRT” | From their own help center: Winona doesn’t directly work with insurance companies and is not able to bill your insurance provider on your behalf. HSA/FSA accepted at checkout; receipts and NDC forms available for possible reimbursement. Their help page notes that not every ingredient used in their HRT will have an NDC code. | Cash-pay-only isn’t in the marketing. It’s in the FAQ. And that NDC note matters: an HSA/FSA administrator asking for one may not get one. |

Midi Health — and what it can’t do

The flaw, stated plainly:Midi cannot bill Medicare or any Medicare-related plan, and it is not enrolled with Medicaid at all. If you’re on Medicaid, they can’t see you, period. If you’re on Medicare, they can see you — but only as a cash patient, with no claims submitted.

And here’s why that’s a limitation, not a dealbreaker:Midi built its model around commercial PPO billing. That focus is exactly why they’re the one provider on our approved list that’s in-network with most PPO plans and operates in all 50 states.

The routing is simple.On Medicaid? Don’t book. On Medicare and want to use your benefits? Midi isn’t your route. On a commercial PPO and stuck without a prescriber who’ll engage?That’s who Midi is built for.

ON A PPO AND NEED SOMEONE IN YOUR CORNER?

Check whether Midi is in-network with your plan

In-network with most PPO plans. All 50 states. Self-pay $250 initial / $150 follow-up if they’re not. HSA/FSA accepted. Not Medicaid. Not billable to Medicare.

Check Midi’s network coverage →Checking costs you nothing and commits you to nothing. We earn a commission if you book; see our disclosure.

If insurance is a dead end for you

Cash-pay is a legitimate path, and it’s the right one for some women. Winona is cash-pay. They state they can’t bill your plan. HSA/FSA at checkout, with receipts you can submit for possible reimbursement. Their offerings include compounded preparations, which are not FDA-approved products. Pricing varies by protocol — verify it at checkout, not from a review site, ours included.

The one question to ask any telehealth provider before you pay

Ask it before you hand over a card. If the answer is no, you’re paying cash — no matter what the homepage says.

When this page isn’t enough

Insurance coverage and medical appropriateness are separate questions. A coverage page can help resolve a pharmacy rejection or verify a benefit. It cannot determine whether progesterone is appropriate for an individual, which product or regimen fits her history, or whether online care is a suitable starting point.

Stop reading this page and call a clinician if:

- You have unexplained vaginal bleeding. This is not an insurance question.

- You’re deciding whether to start, stop, or change therapy at all.

- You don’t know why progesterone was prescribed to you.

- You have a history of breast cancer, blood clots, stroke, heart or liver disease, or a known allergy to an ingredient in the product.

- You’re pregnant, trying to conceive, or using progesterone for fertility care. Different rules entirely.

- The prescription doesn’t match what you and your doctor discussed.

- You’re considering switching to whatever your insurer prefers. That’s a conversation, not a self-serve decision.

And if what you need is a different page:

| If you’re here for… | Go here instead |

|---|---|

| Whether you medically need progesterone | Find My HRT Path, then a clinician |

| Prices and how to lower them | Our HRT cost page |

| Coverage for the rest of your HRT | Our HRT insurance hub |

| Online providers that prescribe progesterone | Best online progesterone providers |

| Estradiol patch coverage specifics | Does insurance cover estradiol patch? |

| Coverage outside the United States | This page is US-only and won’t help you. |

How we verified this

What we actually did, and what we didn’t.

On July 16, 2026 we read:the UnitedHealthcare 2026 Commercial Prescription Drug List (effective January 1, 2026) and the 2026 Premium Formulary booklet published by Optum Rx for Wespath (effective January 1, 2026), recording the exact progesterone, Prometrium, medroxyprogesterone, Provera, and Bijuva rows, tiers, symbols, and the documents’ own definitions of tiers, exclusions, and quantity limits; the current FDA prescribing information for Prometrium (rev. 02/2026) and Bijuva on DailyMed, including full inactive-ingredient lists; generic progesterone capsule labels on DailyMed, including Amneal’s (rev. 02-2026-03); the ASHP drug shortage entry for progesterone capsules; Medicare.gov and CMS pages for 2026 Part D cost figures and Part D appeal timelines; the National Academies’ 2020 report on compounded bioidentical hormone therapy; and the published insurance and pricing pages of Midi Health and Winona.

What we did not do:We did not call any insurer. We did not read every drug list in America — we read two, and we say so every time we cite them. We did not audit any Medicare Part D or Medicaid formulary. We did not read every progesterone application ever filed with the FDA. We did not verify Aetna’s 2026 exclusion list, because their site blocked our request, so we left it out rather than guess.

Every number on this page is a starting point for your phone call. None of it is a guarantee about your coverage.

Editorial research by The HRT Index. Not medically reviewed by a clinician.Educational only — not medical advice. Talk to your prescriber before changing anything. Last verified: . Found something wrong? Tell us and we’ll fix it and date the fix.

Frequently asked questions

- Why did my pharmacy only give me 12 progesterone pills?

- Three possibilities. A quantity limit: the FDA-approved dose for endometrial protection is 200 mg for 12 days per 28-day cycle — twelve capsules — and some plans build limits from that number, while modern prescribing is often one capsule daily (thirty per month). A partial fill: progesterone capsules are on the shortage list, and the pharmacy may only have had twelve. Or a day-supply mismatch. Ask the pharmacist: "Is this a plan quantity limit, or do you just not have the rest?" Worth noting: neither of the two 2026 formularies we read flags a quantity limit on oral progesterone, so this varies by plan.

- Is Prometrium the same as generic progesterone?

- Same active ingredient, same strengths, and the FDA rates them therapeutically equivalent — so a pharmacist can generally substitute the generic unless the prescriber specified brand only, subject to your state's substitution law. Insurance treats them very differently: on both 2026 formularies we reviewed, generic oral progesterone is covered at Tier 1 or Tier 2 while Prometrium is marked excluded. Both contain peanut oil.

- Does insurance cover progesterone if I'm not taking estrogen?

- It may, but you're more likely to hit an indication problem. Prometrium's FDA-approved uses are prevention of endometrial hyperplasia in postmenopausal women with a uterus who are receiving conjugated estrogens tablets, and treatment of secondary amenorrhea. Progesterone taken alone for sleep or perimenopause symptoms falls outside that. Off-label prescribing is legal and common, but it's a medical-necessity conversation with your prescriber — not a coding trick, and not something to misrepresent to your plan.

- Does insurance cover progesterone if I've had a hysterectomy?

- Worth a real conversation with your prescriber before you fight your insurer. The FDA-approved menopause indication for progesterone is preventing overgrowth of the lining of the uterus. Without a uterus, that specific reason doesn't apply, which puts the prescription outside the labeled use and can make coverage harder. Ask your clinician why it's being prescribed for you.

- Does Medicare cover Prometrium?

- Part D and Medicare Advantage drug plans each publish their own formulary, so this has to be checked against your specific plan's drug list — we audited commercial lists for this page, not Part D ones. What we can tell you: brand Prometrium was marked excluded on both 2026 commercial lists we read, while generic oral progesterone was covered on both. And remember the 2026 Part D figures: a $615 maximum deductible and a $2,100 out-of-pocket cap on covered drugs.

- Is compounded progesterone covered by insurance?

- Not automatically, and don't assume either direction. Compounded preparations are not FDA-approved products and many commercial plans exclude them. Under Medicare Part D rules, a compounded prescription may be covered when it contains at least one ingredient that qualifies as a Part D drug — so a blanket "Part D never covers compounds" is wrong. Confirm with your plan. The National Academies recommends restricting compounded bioidentical hormone therapy to two situations: allergy to an ingredient in an FDA-approved product, and a dosage form that doesn't exist as FDA-approved.

- Why is my copay higher than the cash price?

- Because your plan's price and the cash market's price are set by different systems that don't talk to each other. With inexpensive generics, the cash price often wins. Just know that discount-card spending usually isn't automatically credited toward your deductible or out-of-pocket maximum — save the receipt and ask your plan. On Medicare, it doesn't count toward your $2,100 cap.

- I'm allergic to peanuts. What are my options?

- This is the most important question on this page. Every FDA-approved oral progesterone capsule we read — brand and generic — contains peanut oil and is contraindicated in peanut allergy on its own label. Watch for "arachis oil," which is peanut oil under its botanical name; different manufacturers use different words for the same ingredient. Talk to your prescriber about routes and products that don't contain it. And know this: your plan's preferred alternative being contraindicated for you on its own FDA label is about as strong as an exception argument gets.

- How long does a progesterone exception take?

- It depends on your plan type. Under Medicare Part D, a coverage determination or exception is generally decided within 72 hours, or 24 hours expedited — but for an exception, that clock starts when the plan receives your prescriber's supporting statement, not when you call. Under most employer and Marketplace plans, expect similar decision windows, then 180 days to file an internal appeal and roughly 45 days for an external review that's binding on the insurer. Medicare's appeal deadline is 65 days, not 180. Follow the instructions in your denial notice.

- My progesterone is on backorder. Does that mean I'm not covered?

- No. A backorder is a stock problem, not a coverage decision — the two are separate questions. Progesterone capsules are on the ASHP shortage list in 2026. Ask for a different manufacturer, try an independent pharmacy, or ask about 90-day mail order. And check what your plan would cover before you pay cash for something else to solve a supply problem.

- Does insurance covering progesterone mean it's right for me?

- No. Coverage means a plan agreed to pay under its rules. It's a purchasing decision made by a committee that has never met you, and it says nothing about whether progesterone suits your body, your history, or your dose. Those are questions for your clinician.

STILL NOT SURE WHICH HRT PATH FITS YOU?

You came here with a rejection slip.

If you leave with a phone script and a prescription that fills, we did our job.

But if what you actually figured out today is that the problem was never your pharmacy — it’s that nobody is quarterbacking your menopause care — take our free matching quiz. It takes about 90 seconds and gives you a personalized starting-point plan, including a flag if your situation belongs with an in-person clinician first.

Start Find My HRT Path →See our full HRT insurance hub