Does insurance cover compounded hormones? Usually not.

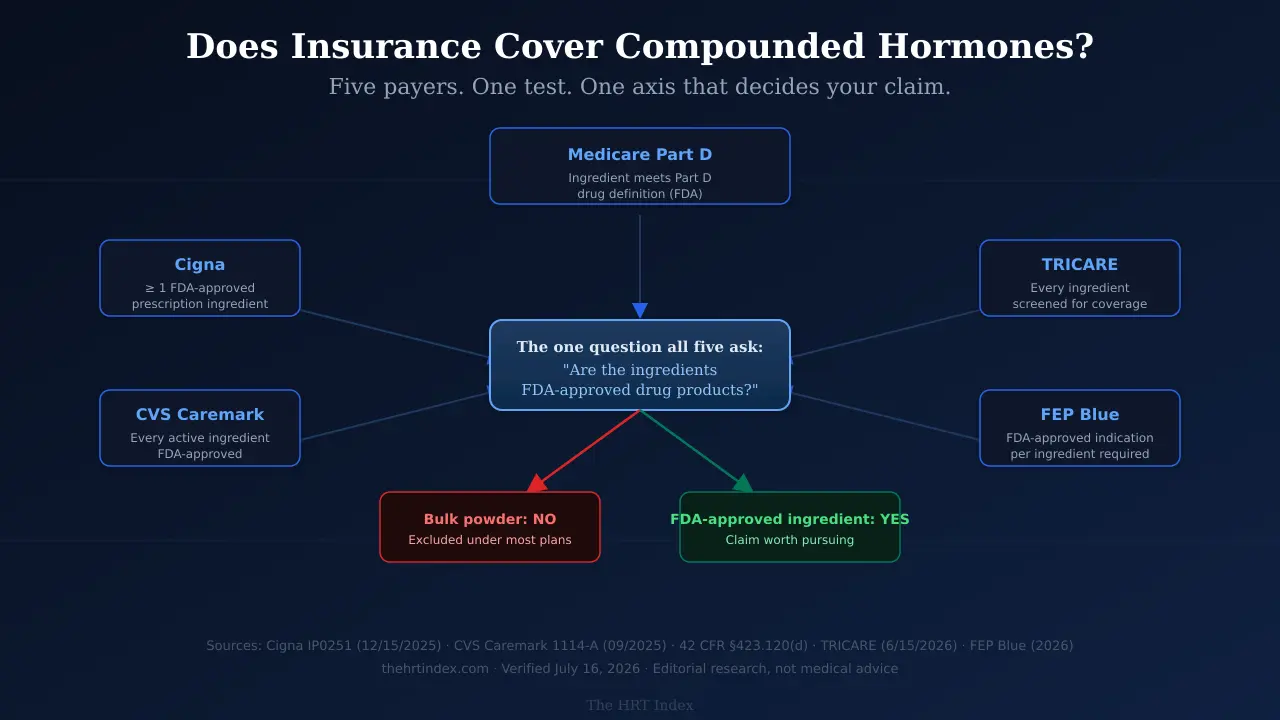

Compounded hormones are typically made from bulk drug substances. The compound policies we read all test the same thing — the ingredients. Cigna requires at least one FDA-approved prescription ingredient. CVS Caremark’s criteria require every active ingredient to be FDA-approved. Medicare Part D requires an ingredient that independently meets the federal definition of a Part D drug. Bulk powder meets none of those tests.

That’s the answer. Here’s the part nobody told you.

You called your insurer and got “it depends on your plan.” That’s true — your plan document really does control. But it’s also the least useful sentence in American healthcare, because it sends you into a phone tree to ask the wrong question.

So we did something different. We opened the actual coverage documents and read them. They’re not identical. They have different criteria, different exceptions, different lawyers. But they all turn on the same axis: are the ingredients FDA-approved drug products? Once you know that’s the question, you can answer it about your own prescription in about ten minutes. We’ll show you how.

And if your estradiol patch is on backorder right now and someone offered you a compounded cream instead — read section 6 before you say yes. There’s a specific trap in that swap, it’s written into one PBM’s criteria, and we’ll show you exactly where it sits.

What each payer’s own document establishes

How we built this: we read current published regulations, payer policies, and program pages, recorded what each one expressly establishes, and normalized them into one format. These are published examples, not a survey of every U.S. plan. Your plan document controls, and it can differ from anything below.

| Benefit system (source + date) | What the source establishes | Main gate | Best next action |

|---|---|---|---|

| Cigna — Coverage Policy IP0251, eff. 12/15/2025 | Bulk chemicals used in compounds don't meet the definition of a Prescription Drug in Cigna standard benefit plans. Six criteria, all required, for compounds that are reviewed. Listed compounded hormone pellets are classified experimental, investigational, or unproven. | Criterion 2: the compound must contain at least one FDA-approved prescription ingredient. | Ask whether your specific plan uses this standard policy, and confirm with your pharmacy whether the formula contains any FDA-approved prescription ingredient. |

| CVS Caremark — PA criteria 1114-A, dated 09/2025 | Approval requires every active ingredient to be an FDA-approved drug, plus a stack of conditions — including that the request is not a topical for skin, not containing bulk powder, and not a hormone therapy compound for menopause or androgen decline due to aging. | Three independent gates a menopause cream fails. | Get the criteria document that governs your actual employer group. Caremark administers many client plans and clients can customize. |

| Medicare Part D — 42 CFR §423.120(d) | A multi-ingredient compound may be covered under Part D only if at least one ingredient independently meets the definition of a Part D drug and it isn't a Part B compound. Formulary status and an approved exception affect payment for eligible ingredients. | Ingredient eligibility, then formulary. | Ask your plan for a coverage determination on the exact formula, not on "compounded hormones." |

| TRICARE — Compound Drugs, updated 6/15/2026 | Express Scripts screens every ingredient for coverage, safety and effectiveness, and medical necessity. A pharmacist may remove or replace a non-covered ingredient. A prescriber may request prior authorization. Denials are appealable. | The ingredient screen. | Let the pharmacy run it, then ask which ingredient failed and whether substitution is possible. |

| FEP Blue — 2026 compound pharmacy policy | Compounds may be considered medically necessary only when all stated criteria are met, including an FDA-approved indication for each ingredient and an unavailable commercial dosage form or strength. Prior approval required. | An all-elements test. | Confirm you're actually governed by the FEP policy, and whether your prescriber can document every element. |

| Aetna — commercial prescription drug claim form | An ingredient-level manual claim route exists. The form asks for a valid 11-digit NDC, ingredient name, metric quantity, and cost for each ingredient — and expressly warns that submitting it does not guarantee reimbursement. | Complete ingredient data, then actual plan coverage. | Get an itemized pharmacy statement before you pay, and confirm the current form and filing deadline. |

| Medi-Cal Rx (California) — provider manual | Multi-ingredient compounds are processed. At least one ingredient must be covered for processing to continue; only eligible ingredients are reimbursed; ingredients requiring authorization aren't paid until approved. | Ingredient, labeler, NDC, and authorization rules. | Use as a California example only. Check your own state's Medicaid pharmacy benefit. |

Read that table again and notice two things. First, these organizations compete. Different lawyers, different formularies, different politics. Second, look at the middle column. Every one of them is asking about the ingredients.That convergence is the whole story, and it’s why “it depends on your plan” is technically true and practically useless.

Not sure which route fits your situation?

The right online HRT provider depends on your symptoms, your age, your medication route preference, your risk history, your insurance, and your state. Some situations belong with an in-person clinician first.

Use the Find My HRT Path Tool →Free. About 90 seconds. No account required. Flags when online care isn’t the right starting point.

1. Does insurance cover compounded hormones?

Usually not. Insurance rarely covers compounded hormones because the finished product is not an FDA-approved drug and is typically built from bulk drug substances, which published compound-coverage criteria commonly exclude or refuse to count as qualifying ingredients. Coverage still depends on the governing plan document, the exact formula, the dispensing pharmacy, and any prior-authorization or exception rules.

Let’s define the word, because it’s doing a lot of work.

Compoundingmeans combining, mixing, or altering ingredients to create a medication tailored to a patient. It can be done by a licensed pharmacist, a licensed physician, or a registered outsourcing facility. It can start from bulk drug substances — raw powders — or, in some cases, from finished drug products. (FDA on human drug compounding)

Most compounded menopause hormones start from powder. Real medicine, made by a licensed pharmacist, from a real prescription.

And the finished product is not FDA-approved. That’s not an insult. It’s a category. FDA didn’t approve the thing in your hand and didn’t review that finished product for safety, effectiveness, or quality before it was sold.

There are seven ways this ends — not two

Most pages give you “covered” or “not covered.” Your claim actually has seven possible exits:

- It pays under the plan’s compound rules.

- Only some ingredients pay. The eligible ones go through; the rest don’t.

- It processes, but you still pay — deductible, copay, or coinsurance.

- It rejects on data, gets corrected, and gets resubmitted. Fixable.

- Prior authorization or an exception is requested.

- You pay cash and file a manual claim. A route exists. Payment isn’t promised.

- It’s excluded outright and stays cash-pay.

Knowing which of the seven you’re in is the entire game. Exit 4 is a phone call. Exit 7 is a wall. Most women can’t tell them apart, so they either give up too early or fight for six weeks over something that was never winnable. Section 3 shows you how to tell.

What this is not about

You’ve probably run through these theories already. Cross them off:

- Not “insurers think menopause is elective.” FDA-approved hormone products go through the ordinary formulary process like any other prescription. A compound denial doesn’t mean your plan is anti-menopause.

- Not “your doctor coded it wrong.” J7999 means compounded drug, not otherwise classified. It’s a real, correct code for a real thing.

- Not you. Some compound rejections are automatic and happen before anyone opens your chart. That’s not a comment on your symptoms or your history.

2. Why doesn’t insurance cover compounded hormones?

There is no single national exclusion. Common barriers include an explicit plan exclusion for compounds, ingredients that are not FDA-approved or not on formulary, missing NDC or claim data, an out-of-network dispensing pharmacy, prior-authorization requirements, and the availability of a commercially manufactured product. Published criteria commonly require a compound’s ingredients to be FDA-approved drug products, which bulk drug substances are not.

Here’s the sentence that reframes everything: a raw powder is an ingredient, not a drug.

Your compounding pharmacy buys estradiol powder, maybe estriol powder, progesterone powder, and a base cream. Those powders are bulk drug substances. They’re real, they’re pharmaceutical grade, they’re legally purchased. And they have never been through FDA’s drug approval process as finished products, because they aren’t finished products.

Now look at what each policy asks for. Cigna: at least one FDA-approved prescription ingredient. Caremark 1114-A: every active ingredient FDA-approved. Part D: an ingredient that independently meets the Part D drug definition. Cigna adds that bulk chemicals don’t meet its plans’ definition of a Prescription Drug at all.

Same question, four documents, one axis.That’s not a conspiracy. It’s what happens when everyone builds a rule on the same regulatory fact.

Three things people mix up — and payers don’t

This trips up prescribers, not just patients. Keep them separate:

| The claim | What’s actually true |

|---|---|

| “The ingredient is used in an FDA-approved product.” | Often true, and irrelevant to the finished compound. Estradiol appears in many approved products. That doesn’t make a compounded estradiol cream approved. |

| “It has an NDC, so it’s FDA-approved.” | No. An NDC is a drug-listing and claim identifier. FDA states plainly that inclusion in the NDC Directory does not mean FDA approval — and representing otherwise can be misbranding. Compounded products can appear there. |

| “FDA-approved ingredients means the medicine is FDA-approved.” | No. Approval attaches to a finished drug product, not to a shopping list. |

Read that middle row twice. It’s the one that costs money — because “we’ll give you the NDC for reimbursement” sounds like a promise and isn’t one.

Medicare is the cleanest example

Under 42 CFR §423.120(d), a compound may be covered under Part D only if at least one ingredient independently meets the federal definition of a Part D drug — a definition that runs on FDA approval — and the compound isn’t classified as a Part B compound.

So ask your pharmacy one question: “Is every active ingredient in this supplied as a bulk substance?”

If the answer is yes, that formula has no ingredient that independently qualifies. There’s nothing there for Part D to pay for. Not a bad tier. Not disfavored. Nothing to price.

If the answer is no — if something in there is a finished, approved product — you’re in a different conversation, and it’s worth having.

3. How can I tell whether my compounded hormone claim will be denied?

Under CVS Caremark prior-authorization criteria 1114-A, three features can each independently block approval: a topical compound for use on skin, a compound containing bulk powder, and a hormone therapy compound for menopause. This predicts the outcome only for members whose plan actually uses that criteria document; other plans apply different rules.

Go get the bag from the compounding pharmacy. We’ll wait. This is the five minutes that turns an abstract rule into your own paperwork.

Caremark’s compound criteria (1114-A, dated September 2025) run a gate. To be considered, a compound has to clear all of it. Ask your own label:

The criteria require that the request is not for a topical compound or topical compound kit for use on skin.

The criteria require that the compound not contain a bulk powder. Ask the pharmacy directly: “Was this compounded from bulk active pharmaceutical ingredients?”Don’t guess — ask.

This one isn’t inferred. It’s written out. The criteria require that the request is notfor a hormone therapy compound for menopause or for androgen decline due to aging — and they name testosterone, estrogen, progestin, and bioidentical hormone as examples.

Now pull up your EOB or superbill

If you got pellets, look for these codes. They’re in Cigna’s policy by number:

- CPT 11980 — subcutaneous hormone pellet implantation. Under Cigna’s policy, specified uses of compounded hormone pellets are classified experimental, investigational, or unproven.

- J3490 (unclassified drugs), J3590 (unclassified biologics), J7999 (compounded drug, not otherwise classified). These identify what was billed. They don’t by themselves prove exclusion.

One hard fact behind all of it, stated flatly in Cigna’s policy: there are no FDA-approved implantable estrogen or progesterone hormone pellets.None exist. That isn’t your insurer being difficult.

The 10-minute phone call that actually gets an answer

Most people call and ask “is my compounded estradiol cream covered?” The rep searches a formulary that doesn’t contain compounds, says “I don’t see it,” and you hang up knowing nothing.

Ask these instead:

• “Does my plan have a blanket compound exclusion, or an ingredient-level bulk chemical exclusion?”

• “Who is my pharmacy benefit manager, and what exact criteria document governs my group?”

• “Is this dispensing pharmacy in network?”

• “Is prior authorization, an exception, a corrected resubmission, or a manual claim available to me?”

• “What’s the case number and call reference number for this conversation?”

Then ask your pharmacy to run a test claim before you pay:

“Please submit this exact prescription to my pharmacy benefit before I hand you a card. If it rejects, tell me the reject code and which ingredient or field caused it.”

4. What insurance CAN still cover: the five separate bills

Hormone therapy can generate up to five separate charges — the clinician visit, lab work, an FDA-approved prescription, a compounded prescription, and any membership or shipping fee — and each can receive a different coverage decision. A denied compound does not mean the visit or the lab work is also denied.

Here’s where real money gets lost.

“Is HRT covered?” is the wrong question, because HRT isn’t one bill. It’s five, and they run through different systems that don’t talk to each other.

| The charge | Which benefit handles it | The exact question to ask |

|---|---|---|

| Clinician visit | Medical benefit — or cash-pay, if the provider doesn't bill insurance | "Is this clinician in-network for my plan, and do I need a referral?" |

| Lab work | Medical or lab benefit, often billed by an outside lab | "Which lab is in-network, and is the order billed separately from the visit?" |

| FDA-approved prescription | Pharmacy benefit | "Is this exact product, dose, and route on my formulary? Does it need prior auth?" |

| Compounded prescription | Usually the pharmacy benefit — though office-administered products can run through the medical benefit | "Does my plan process this exact formula, from this pharmacy?" |

| Membership or shipping | Usually neither. Provider terms. | "Is this billable at all, or is it always cash?" |

What “covered” actually means (seven words that don’t mean the same thing)

| What you were told | What it actually means |

|---|---|

| "Covered" | The plan recognizes it as a benefit. You still owe copay, coinsurance, and deductible. |

| "In network" | The pharmacy or clinician participates. The drug can still be excluded or non-formulary. Different question. |

| "On formulary" | The drug is on the plan's list. Compounds usually aren't on the list at all. |

| "Reimbursable" | You can submit paperwork after paying. Nobody promised to pay you. |

| "Applied to deductible" | Your plan paid nothing, but the spend counts toward the day it starts paying. |

| "HSA/FSA eligible" | You can spend tax-free dollars on it. This is not insurance coverage. |

| "Exception available" | Your prescriber can ask the plan to bend a rule. Asking isn't getting. |

The cost nobody mentions

When a plan treats an expense as an excluded, non-covered drug, that money generally doesn’t count toward your out-of-pocket maximum. HealthCare.gov says it in its own glossary: anything you spend on services your plan doesn’t cover doesn’t count toward the out-of-pocket limit. Whether it earns any deductible credit depends on your plan.

For 2026, Marketplace out-of-pocket limits can’t exceed $10,600 for an individual or $21,200 for a family. Medicare Part D’s cap is $2,100— for covered Part D drugs only.

The gap between compounded and covered can be wider than the sticker price.Ask your plan which side of that line your prescription falls on — in writing.

Comparing total cost across routes? See what HRT actually costs in 2026 for the full first-90-day picture.

5. Can you get insurance to cover compounded hormones with an exception?

Rarely, and it depends on the criteria that govern the plan. Published pathways generally require documented intolerance or contraindication to FDA-approved alternatives, or a needed dosage form or strength that isn’t commercially available. Several major policies also require the compound to contain FDA-approved prescription ingredients, which a compound made only from bulk substances would not.

Sometimes. And we’re going to be specific about when, because “just ask for an exception!” is advice that costs women weeks.

The two-circumstance rule — and where it actually lives

In 2020, the National Academies of Sciences, Engineering, and Medicine reviewed compounded bioidentical hormone therapy and recommended prescribers restrict it to two situations:

- Allergy to an ingredient in an FDA-approved hormone product.

- A dosage form no FDA-approved product offers.

That’s clinical guidance. Now the part that reframes it. Those two circumstances show up in payment policy. Cigna’s compounded medications policy cites the National Academies by name and reproduces that framework in its own reasoning. The Menopause Society’s 2022 position statement lands in the same place. They aren’t the same rule — clinical guidance isn’t a contract, and your plan document controls payment. But they say nearly the same thing, and that’s not an accident. Which is why “but it’s working for me” doesn’t appear on any criteria list we read.

The criterion nobody talks about

Cigna’s policy requires all six criteria. Everyone focuses on criterion 1: documented inadequate efficacy, significant intolerance, or contraindication to all FDA-approved alternatives by the same route, with documentation required.

Read criterion 2:

The compound must contain at least one FDA-approved prescription ingredientnot otherwise excluded by the plan’s benefit language.

A formula made only from bulk powders doesn’t clear that. So you can win criterion 1 outright — airtight documentation, five failed alternatives, all by the same route, prescriber did everything right — and still fail on the composition of the product itself.

Caremark 1114-A is stricter: each active ingredient FDA-approved, for the indication prescribed, by the approved route, at or below the approved dose.

When an exception is genuinely worth your time

Worth trying when:

- You have a documented reaction to a specific inactive ingredient — a dye, a preservative, a patch adhesive. Where criteria recognize intolerance or the need to omit an ingredient, this is the case the pathway was built for.

- A needed strength or dosage form isn’t commercially available. Several published criteria, including 1114-A, recognize this.

- Your compound contains an FDA-approved prescription ingredient rather than only bulk powder. This changes which criteria you’re even arguing under.

Worth much less when:

- You prefer the compound

- You feel better on it

- Someone told you it’s more “natural”

Those may all be true. None of them appears as a criterion.

6. Your patch is backordered and they offered you a cream. Read this first.

The American Society of Health-System Pharmacists has listed estradiol transdermal systems in shortage since January 30, 2026. FDA has not announced a shortage during this period. Under CVS Caremark criteria 1114-A, a supply-shortage circumstance does not override the document’s separate requirements excluding topical skin compounds, bulk powder, and menopause hormone compounds.

This is a costly coverage mistake happening right now, and almost nobody has written it down. Here it is.

What’s actually happening

On November 10, 2025, FDA initiated the removal of boxed warnings from menopausal hormone therapy products. On February 12, 2026, it announced the first approved labeling changes.

Prescribing has climbed sharply. Truveta’s analysis of real-world data found estrogen-based HRT prescribing more than doubled from 2018 to 2026 (a 104.8% increase). Among women aged 45–54, rates rose 184.2% across that period — by February 2026, 1 in 20 women in that age group had an estrogen-based HRT prescription. Between July 2025 and February 2026 alone, prescribing rose 25.7% in that group. Patch use more than tripled and became the most common route.

Now the two-lists problem. ASHP has listed estradiol transdermal systems in shortage since January 30, 2026 — its bulletin was last revised July 1, 2026.

FDA has not announced one. Truveta’s researchers noted it directly in April 2026: there was no shortage announcement from FDA during the period, and their data showed no corresponding decline in patch dispensing. FDA Commissioner Dr. Marty Makary told NBC News the industry has been able to keep up “but barely.”

Both things are true at once, because the two lists are built differently. ASHP’s is populated from practitioner and patient reports; FDA works from manufacturer data. So the country is in a shortage that isn’t an official shortage. Which brings us to the trap.

The trap

Your doctor says: “Patches are backordered. Let’s do a compounded cream.”

It sounds like the shortage is your reason. It sounds appealable. It sounds like exactly what an exception is for.

Look closely at Caremark 1114-A. A current supply shortage of the commercially manufactured product ison its list of qualifying patient circumstances. It’s right there. You can check that box honestly.

Because the shortage circumstance sits inside a gate. Before anyone reaches the supply question, the compound has to be built only from FDA-approved active ingredients, at or below approved doses, by the approved route, and it must not be a topical for skin, must not contain bulk powder, and must not be a hormone therapy compound for menopause.

A compounded estradiol skin cream fails those first.

The box exists. You qualify for it. Under 1114-A, you don’t get to it.

What FDA-approved alternatives can you ask about during a shortage?

“Is there an FDA-approved product — a different patch brand, a gel, a spray, an oral tablet, a systemic vaginal ring — that’s clinically appropriate for me and covered under my plan?”

The shortage isn’t universal. ASHP’s own bulletin lists specific products as available while others are back-ordered — it’s manufacturer-specific, and your pharmacy can check which.

But “might need prior authorization” and “excluded because the ingredients don’t qualify” are different problems. One is a form. The other is a wall.

Ask the question before you accept the compound. Asked this month, it may be worth more than everything else on this page.

If your compound isn’t covered, the question becomes: what does your plan already pay for?

Midi Health says it is in-network with most PPO plans and prescribes FDA-approved hormone therapy — which means your prescription enters the ordinary formulary process instead of compound-review criteria. Midi’s own FAQ says insurance is more likely to cover FDA-approved bioidentical hormones than compounded preparations. Self-pay is $250 for a first visit and $150 for follow-ups. With insurance, your plan determines your deductible, copay, coinsurance, and any prior authorization.

If that’s your coverage, don’t click this. Scroll to section 10— we have a route built for you.

If you have a PPO: because Midi only contracts with plans it’s actually in-network with, you can find out what your visit costs before you book instead of six weeks after.

Check whether Midi is in-network with your plan →Affiliate link. We earn a commission if you book. It doesn’t change your price, and it didn’t decide the order of this page.

7. What FDA-approved hormones does insurance cover instead?

FDA-approved estradiol and micronized progesterone products run through ordinary formulary and pharmacy-claim pathways rather than compound-review criteria. Exact coverage, tier, prior-authorization requirements, pharmacy network, and member cost remain specific to the product and the plan.

| What you’re taking now (compounded) | FDA-approved product(s) containing that hormone | Claim route | The honest note |

|---|---|---|---|

| Estradiol cream, gel, or troche | Estradiol patch, gel (EstroGel, Divigel), spray, oral tablet (Estrace/generic), systemic vaginal ring (Femring) | Ordinary formulary — check tier, network, and PA for the exact product | Route changes the risk profile. Oral estrogen undergoes first-pass metabolism in the liver; transdermal largely avoids that first pass. Clinician decision. |

| Micronized progesterone capsule | Prometrium / generic oral micronized progesterone | Ordinary formulary — plan-specific | The row where an FDA-approved product matches the compounded form most directly: same hormone, same oral route. |

| Estradiol + progesterone combo | Bijuva (estradiol/progesterone, one capsule) | Ordinary formulary; brand may need PA or step therapy | The FDA-approved bioidentical E+P combination in a single oral capsule. |

| Bi-est or tri-est (estradiol + estriol ± estrone) | ⚠️ None. | Compound criteria | FDA states no FDA-approved drug contains estriol. There's no approved bi-est to switch to, and a formula containing estriol can't satisfy criteria requiring FDA-approved ingredients. Estradiol alone is a different medication, not a substitution. |

| Testosterone cream or troche | ⚠️ No product approved for women — but see below. | Off-label; plan-specific | Read the testosterone section below. This is the row most often gotten wrong. |

| Vaginal DHEA | Intrarosa (prasterone) | Ordinary formulary — plan-specific | An FDA-approved vaginal DHEA product exists. Worth asking about. |

| Pellets (any hormone) | None for estrogen or progesterone | Often classified experimental/investigational | No FDA-approved implantable estrogen or progesterone pellets exist for menopause. FDA-approved testosterone pellets exist for male indications. |

“Bioidentical” isn’t what you were told it was

“Bioidentical” describes molecular structure — the hormone has the same chemical structure as the one your body makes. It is not a regulatory category and it is not a safety claim.

Cigna’s own coverage policy calls bioidentical hormone replacement therapy a marketing term not recognized by the FDA. The Endocrine Society says no published peer-reviewed studies show compounded bioidentical products are safer or more effective than FDA-approved ones, and recommends FDA-approved products.

Testosterone: the row everyone gets wrong

We had this wrong in an earlier draft, and it matters enough to say plainly.

There is no FDA-approved testosterone formulation for women in the United States. ACOG’s clinical consensus states it, and Cigna’s policy says testosterone products aren’t FDA-approved for use in women.

But compounding is not the only route. ACOG notes that FDA-approved preparations dosed for men can be titrated for use in women, and The Menopause Society’s practice guidance goes further: when no approved formulation for women is available, it’s reasonable to prescribe an approved male formulation off-label at roughly one-tenth the male dose — and compounded products cannot be recommended, because of the lack of efficacy and safety data.

Where compounding may genuinely be required

A formulation containing estriol currently requires compounding, because no FDA-approved U.S. drug contains estriol. FDA states no FDA-approved drug contains estriol. If bi-est is what you’re on, there is no approved product to switch to — and a compound containing estriol won’t satisfy criteria that require FDA-approved ingredients. That’s the corner with no good exit, and you deserve to know you’re in it.

What the 2026 label change did — and didn’t — change

FDA initiated the boxed-warning removal in November 2025 and announced the first approved labeling changes in February 2026, removing cardiovascular disease, breast cancer, and probable dementia statements from the boxed warning. The endometrial-cancer boxed warning remains for systemic estrogen-alone products.

Those changes apply to FDA-approved products only.

Compounded hormones have no FDA-approved label. They never carried that warning — and they didn’t get the update either.

8. Does Medicare Part D cover compounded hormones?

Medicare Part D applies an exact-formula, ingredient-eligibility test. A multi-ingredient compound may be covered only if at least one ingredient independently meets the federal definition of a Part D drug and the compound is not classified as a Part B compound. Formulary status and an approved exception can affect whether eligible ingredients are payable.

Rarely — and for a reason you can check in one phone call to your pharmacy.

Ask: “Is every active ingredient here supplied only as a bulk substance?”If yes, that formula has nothing that independently meets the Part D drug definition, and there’s nothing for Part D to price. If something in it is a finished, approved product, the compound rule may apply and a coverage determination is worth requesting.

Request the determination on the exact formula— not on “compounded hormones” in general. That distinction is the difference between a real answer and a shrug.

Part D’s $2,100 out-of-pocket cap for 2026 counts covereddrugs only. Cash spend on an excluded compound doesn’t move it.

And watch a very common mix-up: a telehealth company accepting Medicare patients tells you nothing about whether your medication is covered. Two different decisions, two different organizations.

9. Does Medicaid cover compounded hormones?

Medicaid pharmacy coverage is state-specific, so no reliable national answer exists. California’s Medi-Cal Rx processes multi-ingredient compound claims and reimburses only eligible ingredients, subject to ingredient, labeler, NDC, and prior-authorization rules. Other state programs apply different rules.

State by state. That’s not a dodge — it’s the actual answer, and any page giving you a national yes or no is guessing.

We verified one state.California’s Medi-Cal Rx processes multi-ingredient compounds through electronic and paper routes. At least one ingredient must be covered for processing to continue. Only eligible ingredients are reimbursed. Ingredients requiring prior authorization aren’t paid until authorization is approved.

That tells you nothing about the other 49. State programs differ on preferred drug lists, compound claim fields, ingredient rules, prior authorization, pharmacy networks, and appeals.

10. Does TRICARE cover compounded hormones?

TRICARE screens every ingredient in a compound through Express Scripts for coverage, safety and effectiveness, and medical necessity. A pharmacist may remove or replace a non-covered ingredient, a prescriber may request prior authorization, and a denial may be appealed within 90 days under current guidance.

TRICARE is the most transparent process we reviewed. Its published steps (updated June 15, 2026):

- Electronic screen. Every ingredient checked for coverage, safety and effectiveness, and medical necessity. Under five seconds.

- Substitute or replace. If an ingredient fails, your pharmacist may be able to remove it, swap in a covered one, or call your prescriber. Happens while you wait — about 15 to 20 minutes.

- Prior authorization. If nothing can be substituted, your prescriber can request individual review. About five days once Express Scripts has the paperwork.

Denied? You have 90 days to request a formal appeal.

Here’s the route that still works.

Most menopause telehealth platforms — including Midi — can’t help you. Stop looking for a platform that bills your insurance.

You don’t need a platform that bills your insurance. You need a prescriber. Your own coverage handles the pharmacy.

Sesameis a cash-pay marketplace where you pick your own clinician from named providers with published credentials. Sesame states plainly that it doesn’t bill health insurance, specifically to keep prices predictable and available to everyone regardless of insurance status.

Here’s the mechanism, in Sesame’s own words: if you do have health insurance, the cost of any prescribed medication or lab work may be covered depending on your plan. Your clinician sends a prescription for an FDA-approved product — estradiol, micronized progesterone, Bijuva, Intrarosa — to your local pharmacy. The visit is cash. The prescription runs through your own Part D or Medicaid benefit like any other prescription— subject to your formulary, your tier, and any prior authorization. FDA approval doesn’t guarantee payment. It just means you’re in the ordinary process instead of compound-review criteria.

Sesame publishes its subscription price at signup. Confirm the current figure at checkout— we don’t publish provider prices we haven’t verified on the day.

Affiliate link. We earn a commission if you book. It doesn’t change your price.

11. Can you file a claim after you’ve already paid cash?

A manual claim route generally exists, but it is an administrative path rather than a promise of payment. Plans typically require a claim form, an itemized pharmacy receipt, ingredient-level data including available 11-digit NDCs, prescriber information, and submission within a plan-specific deadline. Aetna’s commercial claim form expressly states that submission does not guarantee reimbursement.

Yes — and go in clear-eyed. A manual claim asks the same plan the same question the pharmacy already asked. If the answer was “these ingredients don’t qualify,” paper won’t change it. If the rejection was about data — a missing field, a wrong pharmacy identifier — this is exactly how you fix it.

Build the packet

- Member, plan, and group number

- Prescription number and fill date

- Prescriber name and NPI where requested

- Pharmacy name, address, and identifier

- Each ingredient name, with available 11-digit NDC, metric quantity, and cost

- Total quantity, days’ supply, total amount paid

- Itemized pharmacy receipt — not a cash-register slip

- The current plan claim form and its filing deadline

- Proof of submission

One more time, because it’s the trap: an NDC on your receipt is not proof of coverage or FDA approval.It’s an identifier. The plan still decides whether it’s payable.

12. Can you use HSA or FSA money for compounded hormones?

HSA and FSA eligibility follows tax and account-plan rules for qualified medical expenses, which are different from insurance coverage rules. A prescribed compounded hormone may qualify as a medical expense, but the account administrator’s documentation requirements control, and eligibility is not a guarantee of reimbursement.

Often yes. And it surprises people, because insurance just said no.

- Your insurer asks: is this an FDA-approved drug product the plan covers? For most compounds, no.

- Your HSA/FSA asks: is this a qualified medical expense under the tax rules and your account plan? A prescribed medicine for medical care generally can be.

Same product. Different answers. Because they’re not asking the same question.

Practically: pre-tax dollars against a $150/month compound is a real discount depending on your bracket.

Three things to know. Some administrators scrutinize compounds harder and may want a letter of medical necessity — keep itemized receipts. Eligibility isn’t reimbursement; the administrator’s rules decide. And once you’re enrolled in Medicare, you can’t make new HSA contributions — existing balances still spend on qualified expenses.

That’s a compounded provider telling you, in writing, on their own site, that some components won’t carry a usable claim identifier. We respect them for saying it out loud — and it’s the clearest illustration on this page of why “we’ll give you the paperwork” isn’t the same as “you’ll get paid.”

13. Should you appeal a compounded hormone denial?

Whether an appeal is worth pursuing depends on the denial reason. Denials involving medical judgment or an experimental/investigational determination may qualify for external review under the governing federal, state, or plan process. Denials based on an explicit benefit exclusion are contract terms, which an appeal is unlikely to override. The denial notice identifies the applicable route and deadline.

Usually not — and we’d rather say that plainly than let you find out in six weeks.

First: identify what kind of “no” you got

Don’t file anything until you know which row you’re in.

| The denial says | What it actually is | Your move |

|---|---|---|

| Missing or incorrect claim data (invalid NDC, missing quantity or days' supply, wrong pharmacy ID) | A paperwork error | Pharmacy corrects and resubmits. Often fixed same day. |

| Out-of-network pharmacy | A network problem | Ask whether an in-network compounding pharmacy can fill it, or whether a network exception exists. |

| Non-formulary drug | A formulary miss (usually means no compound rule applies) | Ask for a non-formulary or medical exception if criteria allow. |

| Not medically necessary | A medical judgment | A clinical exception with prescriber documentation. May qualify for internal and then external review. |

| Prior authorization required | A process gate, not a final answer | Start the PA. Get your prescriber's office to file it. |

| Experimental, investigational, or unproven | A medical-judgment determination — not a contract term | This is the denial most likely to qualify for independent external review under federal or state rules. Follow the appeal notice. |

| Benefit exclusion / not a covered benefit | A contract term | Hard to overturn. The plan doesn't cover this category. An appeal may be procedurally available but is unlikely to change the contract. |

Appeal deadlines: the ones that matter

| System | Standard internal deadline |

|---|---|

| Commercial plan (ERISA) | 180 days from denial notice to file internal appeal; external review after exhausting internal. |

| ACA Marketplace plan | Follow the denial notice; external review available after internal appeal. |

| Medicare Part D | 65 days for Level 1 redetermination. Standard: 7 days (benefit) / 14 days (payment). Expedited: 72 hours. |

| TRICARE compound appeal | 90 days after the compound isn't approved. |

When to stop

Stop when your plan document has an explicit compound exclusion with no exception pathway. Stop when the pharmacy confirms the formula is bulk-only and the criteria require FDA-approved ingredients. Stop when the recovery is smaller than what the fight costs you.

Redirecting that energy toward a route your plan already processes usually pays back faster than winning would have.

A denial isn’t always the end — but it isn’t always worth fighting.

See which route fits your plan, your state, and your situation before you spend weeks on paperwork.

Compare my next-step options →Free. About 90 seconds. No account required.

14. If you want to stay on compounded hormones anyway

Choosing compounded hormone therapy as a cash-pay expense is a legitimate decision, and a formulation containing estriol currently requires compounding because no FDA-approved U.S. drug contains estriol. Compounded preparations are not FDA-approved, meaning FDA has not evaluated the finished product for safety, effectiveness, or manufacturing quality before marketing.

That can be the right call. We’re not going to talk you out of it — telling you to leave would be the same paternalism the rest of the internet practices in reverse.

Go in with your eyes open on three things.

What you’re accepting. Compounded drugs aren’t FDA-approved. FDA doesn’t verify their safety or effectiveness, and there’s no FDA finding of manufacturing quality before they’re sold. Poor-quality compounding can produce sub- or super-potent product. ACOG’s clinical consensus reports that levels in compounded preparations could be as much as 26% below label for estradiol and 31% above label for progesterone, and that conventional therapy is preferred when FDA-approved formulations exist.

What it costs beyond the sticker.When a plan treats a compound as an excluded expense, it generally gives you no out-of-pocket-maximum credit. Deductible treatment is plan-specific — ask.

Sometimes there is. Sometimes there genuinely isn’t. Both answers are worth having, and you can only get one by asking.

If you’ve read this far, you know what your plan asks about a bulk compound.

Winona publishes its prices, which is rarer than it should be — and it publishes its ingredient lists, which is rarer still. As of July 16, 2026: Estrogen Body Cream with Progesterone from $89/month, Progesterone Capsules from $39/month, Estrogen Tablets from $54/month, Vaginal Estrogen Cream from $89/month.

| Winona product | Regulatory status | What we verified |

|---|---|---|

| Estrogen Body Cream (and with Progesterone) | Compounded. Not an FDA-approved drug product. | Winona lists the actives as estradiol USP and estriol USP, and calls bi-est “a compounded blend.” Prepared by a state-licensed compounding pharmacy. |

| Vaginal Estrogen Cream | Compounded. Not an FDA-approved drug product. | Active ingredient listed as estradiol USP; Winona states it’s compounded by a state-licensed pharmacy. |

| Progesterone Capsules, Estrogen Tablets, Estrogen Patch | Winona describes these as FDA-approved products. | Provider-stated. Confirm at intake — it changes your coverage answer completely. |

The damaging admission — and we mean it as a compliment: Winona does NOT bill your insurance. At all. No claims, no prior authorization. Their help center says it directly. It provides receipts and NDC documentation for member-submitted reimbursement attempts — and tells you honestly that not every ingredient has an NDC. If getting your plan to pay is your priority, go back to Midi or Sesame.They’re the better call and we’d rather you go there.

Because Winona skips the insurance machine entirely, they put one number on the screen before you order. No EOB six weeks later. No reject code at the counter. You know what it costs before you decide. Winona accepts HSA/FSA at checkout. Check state availability— coverage is limited and we don’t publish a state count we haven’t confirmed with Winona directly.

See Winona’s published pricing and check your state →Affiliate link. We earn a commission if you subscribe.

15. When online HRT isn’t the right starting point

A coverage decision is an administrative determination, not a clinical one. Insurance approval does not establish that a treatment is appropriate for an individual, and a denial does not establish that it is inappropriate. Some histories, symptoms, and unresolved diagnoses require in-person assessment before online care is a suitable starting point.

A paid claim doesn’t mean a treatment is right for you. A denied claim doesn’t mean it’s wrong for you.

Your insurer answers one question: does our contract cover this? Your clinician answers a different one: is this the right medicine for this woman?This whole page lives in the first world. Don’t mistake it for the second.

Some histories, symptoms, examination needs, and unresolved diagnoses require in-person assessment first. Our HRT safety and eligibility guide carries the specific routing criteria. If something feels urgent, seek urgent or emergency care — don’t wait on a form.

Find My HRT Pathis built to flag that routing question. It doesn’t diagnose and it doesn’t determine treatment eligibility.

16. What we actually verified

We’re showing our work, because on a question like this you shouldn’t take our word for anything.

| Source | Document | Date on the source | We checked |

|---|---|---|---|

| Cigna | Coverage Policy IP0251, Compounded Medications | Effective 12/15/2025 | 7/16/2026 |

| CVS Caremark | PA criteria 1114-A, Compounded Drug Products | Dated 09/2025 | 7/16/2026 |

| Medicare | 42 CFR §423.120(d) | Title 42 amended 6/16/2026 | 7/16/2026 |

| TRICARE | Compound Drugs | Updated 6/15/2026 | 7/16/2026 |

| HealthCare.gov | Internal appeals; external review; out-of-pocket glossary | Current | 7/16/2026 |

| ASHP | Estradiol Transdermal System shortage bulletin | Created 1/30/2026; revised 7/1/2026 | 7/16/2026 |

| Truveta | Estrogen-based HRT prescribing trends | Published 4/9/2026 | 7/16/2026 |

| FDA | Menopause consumer page; NDC Directory; compounding; Nov 2025 and Feb 2026 labeling actions | Current | 7/16/2026 |

| ACOG | Compounded Bioidentical Menopausal Hormone Therapy | 11/2023 | 7/16/2026 |

| Midi, Sesame, Winona | Published pricing, insurance terms, product pages | Provider-stated | 7/16/2026 |

What we did not do.We did not submit an insurance claim. We did not predict any individual’s approval. We did not identify a credible current national coverage rate for compounded hormones, and we won’t publish one. We did not build a 50-state Medicaid table. We did not publish a provider price we couldn’t see on the day.

What we can’t tell you. Employer groups customize PBM criteria — your plan document supersedes every policy we cited. A published claim form proves a route exists, not that your claim will pay. Provider terms change. This is editorial research, not medical review. The final decisions belong to your plan and your clinician.

This page was produced under The HRT Index Verification Standard: read every published price and policy, separate FDA-approved from compounded, verify state availability and insurance language, record effective and checked dates, and re-check on a fixed schedule. We evaluate providers on five pillars, always in this order: clinical legitimacy, care quality, medication fit, price transparency, and access.

17. Common questions

Questions answered from our source documents. Not medical advice. Not legal advice.

Does insurance cover compounded hormones?

Usually not. Compounded hormones are typically made from bulk drug substances, and published compound criteria commonly require a compound's ingredients to be FDA-approved drugs — Cigna requires at least one, CVS Caremark's criteria require every active ingredient, and Medicare Part D requires an ingredient that independently meets the Part D drug definition. Your plan document, the exact formula, the pharmacy, and any exception rules still control the outcome.

Why was my compounded hormone cream denied?

The reason depends on the plan and the claim. Common ones: an explicit compound exclusion, a non-payable or non-formulary ingredient, missing NDC or claim data, an out-of-network pharmacy, or an available commercial product. Under CVS Caremark criteria 1114-A specifically, topical skin compounds, bulk powder, and menopause hormone compounds are three separate approval barriers — a compounded estradiol cream can fail all three.

Does Medicare cover compounded bioidentical hormones?

Rarely. Under 42 CFR §423.120(d), a multi-ingredient compound may be covered under Part D only if at least one ingredient independently meets the federal definition of a Part D drug and it isn't a Part B compound. Bulk substances don't meet that definition. Ask your pharmacy whether every active ingredient is bulk-supplied, then request a coverage determination on the exact formula rather than on "compounded hormones."

Does insurance cover hormone pellets?

The outlook is poor. Cigna's standard policy classifies listed compounded hormone pellets as experimental, investigational, or unproven; other plans use different terms. No FDA-approved implantable estrogen or progesterone pellets exist for menopause. One useful wrinkle: an experimental/investigational determination is a judgment, not a contract term — which may make it eligible for independent external review in a way a benefit exclusion isn't.

Can I appeal an insurance denial for compounded hormones?

Identify the denial reason first. Missing claim data, network errors, prior authorization, and non-formulary decisions all have different fixes — some are same-day. A clear benefit exclusion is a contract term and is hard to overturn. An experimental/investigational determination may qualify for external review. Follow the deadline on your denial notice; Medicare Part D uses its own coverage-determination and redetermination track.

Are compounded hormones cheaper than FDA-approved hormones?

There's no reliable universal answer, but compare correctly before you assume. Put the compound's cash price next to your member cost for the exact FDA-approved product, then add visits, labs, shipping, membership fees, and the fact that excluded spend generally earns no out-of-pocket-maximum credit while covered spend does. Compounded platforms publish cash prices from roughly $39 to $89 a month per product before any clinic bundling.

Is there an FDA-approved version of bi-est?

No. FDA states that no FDA-approved drug contains estriol, so there's no approved bi-est to switch to and compounding is currently the only route. A compound containing estriol also can't satisfy criteria requiring FDA-approved ingredients. Switching to estradiol alone is a different medication, not a substitution — that's a clinician conversation, not a swap.

Does insurance cover compounded testosterone for women?

There's no FDA-approved testosterone formulation for women in the U.S., and coverage of a compounded one is plan-specific and unlikely. But compounding isn't the only route: ACOG notes FDA-approved preparations dosed for men can be titrated for use in women, and The Menopause Society's guidance says it's reasonable to prescribe an approved male formulation off-label at roughly one-tenth the male dose, while compounded products cannot be recommended. Testosterone is a Schedule III controlled substance requiring a valid prescription from a licensed prescriber. Off-label coverage is a separate, plan-specific question.

Can I use my HSA or FSA for compounded hormones?

Often yes, and it surprises people. HSA/FSA eligibility follows qualified-medical-expense rules under the tax code and your account plan — not FDA approval. A prescribed compounded hormone generally can qualify, but eligibility isn't reimbursement: your administrator's rules and documentation requirements control, and some ask for a letter of medical necessity. Keep itemized receipts. Once you enroll in Medicare you can't make new HSA contributions, though existing funds still spend.

My estradiol patch is backordered. Will insurance cover a compounded cream instead?

Almost certainly not, and this is the most expensive misunderstanding happening in menopause care right now. ASHP has listed estradiol transdermal systems in shortage since January 30, 2026; FDA has not announced one. CVS Caremark's criteria 1114-A do list a supply shortage as a qualifying circumstance — but it sits inside a gate that separately excludes topical skin compounds, bulk powder, and menopause hormone compounds, so a cream fails before the shortage question is reached. Ask your prescriber and your plan about an available FDA-approved alternative instead — a different patch brand, a gel, a spray, an oral tablet.

Can my visit and labs be covered if the medication isn't?

Yes, and many women miss this. The visit, labs, prescription, and any membership fee are separate charges running through different benefits, and each gets its own decision. A denied compound doesn't deny your appointment or your bloodwork. Ask about each one separately rather than accepting "HRT isn't covered" as one answer.

My plan said "it depends." What do I actually ask?

Don't ask "is my compounded cream covered?" — the rep searches a formulary that doesn't contain compounds and tells you they don't see it. Ask: "Does my plan have a blanket compound exclusion or an ingredient-level bulk chemical exclusion? Who's my PBM, and what criteria document governs my group?" Then ask your pharmacy to run a test claim before you pay, and get the reject code.

Still not sure which route is yours?

You now know how to identify why your claim was rejected, whether that reason is correctable, and which route to check next.

The last question is which provider fits your situation — your symptoms, your route preference, your insurance, and your state.

Find My HRT Path

Matches your situation to the right provider, and flags when online care isn’t the right starting point. Free. About 90 seconds. No account required.

Start Find My HRT Path →